How Hong Kong’s Intervention Battle Will Chill Carry Trade

How Hong Kong’s Intervention Battle Will Chill The Carry Trade

(Bloomberg) -- Hong Kong’s defense of its currency peg will likely boost the interbank liquidity pool to a level unseen in two years, lowering local borrowing costs and weakening its dollars.

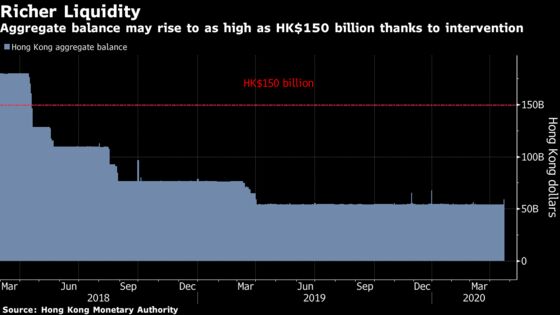

As authorities sell the city’s currency to protect its peg to the greenback, they inject Hong Kong dollar liquidity into the banking system and boost the city’s aggregate balance. The gauge of interbank cash supply will rise to HK$66.8 billion ($8.6 billion) following this week’s operations. It could climb to as high as HK$150 billion this quarter, according Scotiabank and OCBC Wing Hang Bank Ltd. That compares to HK$426 billion in 2015.

That would narrow the gap between local borrowing costs and the U.S. rates from near the widest in two decades -- and make less appealing a carry trade that sent the exchange rate to the strong end of its band for the first time since 2016 this week.

A lowering of borrowing costs would be timely for Hong Kong’s economy as the coronavirus pandemic delivers another major blow after protests rocked the city. Lower interest rates typically translate to stronger motivation for corporates and households to borrow, which would facilitate the recovery of growth in the former British colony.

“I expect the intervention to continue in the coming weeks, and the authorities may spend another HK$50 billion to HK$100 billion to defend the peg,” said Gao Qi, a currency strategist at Scotiabank. “The lower interest rates could help the economy, though potentially higher demand from China and other countries remains the most important driver for the recovery.”

To defend the peg, which allows the city’s currency to move in a narrow range of 7.75 to 7.85 against the greenback, the Hong Kong Monetary Authority has sold the equivalent of about $1 billion of its currency so far this week. That’s the first case of intervention on the strong side of the band since 2015.

A gauge of the Hong Kong dollar’s one-month borrowing costs -- known as Hibor -- was little changed at 1.55% Thursday. Its premium over U.S. interest rates remains elevated at around 100 basis points, suggesting buying the city’s dollars in exchange for the greenback remains profitable. This means the long carry trade will continue and more intervention will be needed, according to Mizuho Bank Ltd.

| Analysts | Aggregate Balance Forecast |

|---|---|

| Carie Li, OCBC Wing Hang | HK$120 billion to HK$150 billion by end-2Q |

| Stephen Chiu, Bloomberg Intelligence | About HK$150 billion in 2Q |

| Ken Cheung, Mizuho Bank | Toward HK$100 billion in 2Q |

Liquidity in the former British colony was tightened by a series of currency interventions in the past two years when lower borrowing costs relative to the U.S. helped drive the currency to the weak end of its trading band. That helped shrink the aggregate balance by 70% to HK$54 billion before Tuesday, which was the lowest level since the global financial crisis.

The Hong Kong dollar weakened to as low as 7.7515 on Thursday, before rebounding to trade at 7.7509 as of 4:14 p.m.

“Carry trade activities will reduce gradually as Hibor drops,” said Carie Li, an economist at OCBC Wing Hang Bank, adding the HKMA will inject liquidity by selling local dollars and reducing issuance of exchange fund bills.

“Then, another round of Hong Kong dollar strength will be driven by strong capital inflows after the pandemic is over in the medium term.”

©2020 Bloomberg L.P.