How Deep a First Rate Cut Is Fed’s Key Debate as July 31 Nears

How Deep a First Rate Cut Is Fed’s Key Debate as July 31 Nears

(Bloomberg) --

It’s the question that looks likely to dominate the run-up to the Federal Reserve’s next meeting: Will it cut interest rates by a quarter-percentage point or twice that?

Fresh from their June gathering, when they indicated a potential willingness to reduce rates for the first time in a decade, some Fed officials have in recent days publicly discussed how far they may go. For now, though, investors are no wiser about just what policy makers will do when they meet again in the final days of July.

Minneapolis Fed President Neel Kashkari got things started June 21 by announcing he had argued already for a 50-basis-point move, to prevent inflation from slipping further. Expectations were bounded by his counterpart from St. Louis, James Bullard, who said June 25 that a half-point cut would be “overdone.” Those comments caught the market’s attention because he voted in June for an immediate reduction.

“The fact that Bullard, one of the leading doves who dissented in favor of a 25-basis-point cut in June, is not ready to back a 50-basis-point cut in July must cool speculation of a double-sized reduction at that meeting,” said Krishna Guha, head of central bank strategy at Evercore ISI.

At the heart of the discussion is whether officials believe the economy needs an “insurance cut” against the possibility of a slowdown, or a more aggressive move to counteract a serious deterioration that may already be underway.

Historically, policy makers have kicked off rate-cutting cycles with reductions of both sizes -- 25 basis points in 1995 and 1998 and double that in 2001, 2002 and 2007.

Trade Thaw

A June 29 meeting between President Donald Trump and his Chinese counterpart Xi Jinping at the G-20 summit in Osaka had the potential to swing the argument one way or another, but ended up being neutral, at least on a longer-term basis. The leaders declared a truce in their trade war, opening the door to renewed negotiations but leaving existing tariffs in place.

Another guidepost comes Friday, when the Labor Department releases payrolls data for June after a weak May report.

A half-point cut has several arguments in its favor.

The Fed is likely to alter borrowing costs in financial markets in a meaningful way only if it surprises. A quarter-point move is arguably already fully priced in and doing more early on would prevent attention from turning immediately to a discussion about the next cut.

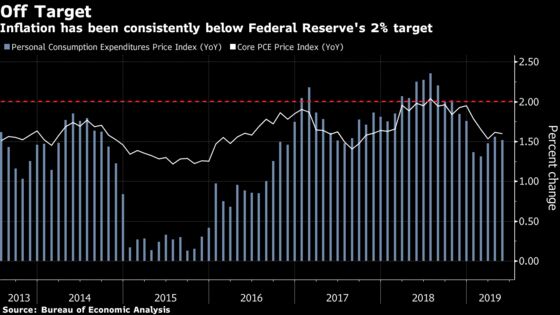

Additionally, the Fed may have moved rates a notch too high in 2018, and the risk of unleashing excess price pressures appears to be very low given that inflation has repeatedly fallen short of the central bank’s 2 percent target.

If more negative economic data surface before month’s end, another technical argument will build momentum. The lower end of the federal funds target range is only 2.25%, limiting how much the Fed can cut if a recession emerges. When a central bank has so little room to maneuver, many economists, including New York Fed President John Williams, have long argued it should act aggressively when the economy begins to sour.

Fed Chairman Jerome Powell acknowledged the wisdom of that very argument at his June 19 press conference.

“That is a valid way to think about policy in this era,” he said. “It’s in the minds of policy makers during this era because it’s well understood to be correct.”

Yet Powell also cautioned against assuming this approach will necessarily influence officials at the Fed’s July meeting.

“Nothing I can say about that is specific to the near-term question that we face,” he said. A 50 basis-point cut, he added, was “something we haven’t really engaged with yet and it will depend very heavily on incoming data and the evolving risk picture.”

Arguments Against

Meanwhile, there are good arguments against a half-point move. If entirely unexpected, it could spook markets as investors might fret the Fed is more worried about the outlook than it’s been letting on. The economic situation also may not be dire enough to justify going large, especially given signs of tightness in the labor market.

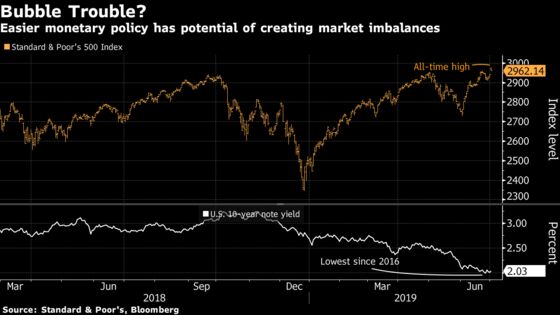

It’s also a concern that the lower rates go, the higher the risk of spurring financial bubbles, a case made June 24 in an essay by Dallas Fed President Robert Kaplan.

“I am concerned that adding monetary stimulus, at this juncture, would contribute to a build-up of excesses and imbalances in the economy which may ultimately prove to be difficult and painful to manage,” Kaplan wrote.

Kaplan isn’t alone in doubting the wisdom of fresh stimulus. Eight of the FOMC’s 17 members submitted projections in June that include no rate cuts this year, and one foresaw a rate hike. Investors would be wise to bear in mind that resistance could fade or grow by the end of July.

Despite that, pricing in federal funds futures contracts late on Monday implied investors in that market see a 100% probability of a cut, with about a 15% chance of a half-point move.

Economists surveyed June 20-24 by Bloomberg came down heavily predicting a quarter-point move. Only three of 36 respondents predicted 50 basis points, though none believed the Fed will stand pat.

UBS Securities LLC economists, led by former Fed staffer Seth Carpenter, expect a 50-basis-point cut this month. Still, they argued in a report that even a quarter-point reduction was “not a foregone conclusion.” Progress on trade talks or a positive tilt for global growth, business investment and inflation could alter the Fed’s calculus.

“Strong increases across a number of these normally first-tier economic indicators could give the committee pause and delay the Fed cut at this meeting,” they said.

To contact the reporter on this story: Christopher Condon in Washington at ccondon4@bloomberg.net

To contact the editors responsible for this story: Alister Bull at abull7@bloomberg.net, ;Margaret Collins at mcollins45@bloomberg.net, Vince Golle

©2019 Bloomberg L.P.