Why Main Street Should Worry About Wall Street’s Bond Sell-Off

(Bloomberg Opinion) -- The recent leg lower in the bond market has pushed mortgage rates to the highest since the start of the decade. The glass half full people might say that's not a problem since rates are less than half the levels seen during the bad old days of the 1980s when borrowing costs exceeded 10 percent. But that's not the way to think about the potential fallout from higher rates. The real issue is what current mortgage rates represent to the current generation of home buyers. And by that measure, the outlook is rather dire.

According to the Mortgage Bankers Association, the average loan rate for a conforming 30-year mortgage was 5.10 percent in the week ended Oct. 12, the highest since early 2011. Back then, that level didn't hold for long, as rates crashed to 3.5 percent by late 2012 and held at those low levels for years. As recently as July 2016, the 30-year rate was at 3.6 percent. Starting points matter, especially now with home prices at nosebleed levels. According to Black Knight’s August Mortgage Monitor, the monthly payment on the average home has jumped by 16 percent since the start of the year. That's up from a 3 percent increase in 2017, illustrating the effect of rising rates on affordability.

The potential for rising rates to inflict damage on household finances has grown in the era of extraordinarily easy monetary policy. Yes, mortgage lending standards were tightened after the housing bubble burst in the financial crisis, but record low rates have nevertheless allowed buyers to afford pricier homes and homeowners to refinance to improve their cash flow via lower payments in order to augment stagnant income growth. But that was then. Refinancing activity is off by a third compared with last year, an effective drag on households.

Twice a month, the University of Michigan reports its Consumer Sentiment Index. In the preliminary October report, reported buying conditions for autos and homes fell. The last time both of these gauges were as low as they are today was the early 1980s as the economy was emerging from a grueling recession. If history is any guide, a sustained level of higher rates is the second nail in the coffin for housing followed by an upward turn in the unemployment rate and recession. We’re well on our way to the second stage.

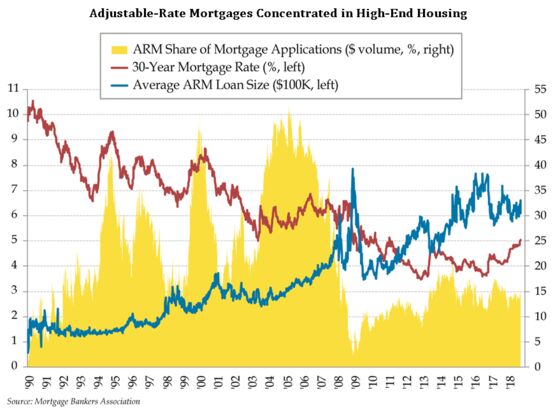

Determined homebuyers are increasingly turning to adjustable-rate mortgages, or ARMs, which have low initial rates that adjust either higher or lower after some period depending on prevailing rates at the time. Currently, the average 5-year ARM charges a rate of 4.34 percent. As per the Mortgage Bankers Association, ARMs comprised 7.1 percent of new applications in the latest week, the most in a year.

To be clear, demand for ARMs is a shadow of what it was during the last boom when underqualified buyers did whatever it took to get into overpriced homes and lenders were happy to accommodate. At the apex of the housing bubble, ARMs were over half of mortgage activity. The drivers of ARM usage, however, have not changed. It’s still all about price. The average ARM today is $661,000, which are clearly being used to finance high-end homes. And just like when the last housing bubble burst, the risk is that ARMs taken out in recent years will reset at higher rates, leading to defaults and weighing on housing prices.

And don't forget that well-heeled home buyers are also likely to have a high concentration of stock market holdings. And given that eight of the top 10 markets with the largest monthly declines in home prices in July as measured by Black Knight were on the tech-heavy West coast, a month when technology stocks were headed to record highs, it's not hard to imagine how fast home prices will fall once the air comes out of the tech bubble.

Black Knight highlighted San Jose in its latest report. The average home price in San Jose fell 1.4 percent in July, a sharper decline than any other market and the steepest drop for any month in any of the top 100 markets since the housing recovery began. Prices are down by 2 percent since May following a cumulative rise of 35 percent over the prior 20 months. Black Knight notes that "71 of the largest markets nationwide have seen the rate of home price appreciation slow in recent months.”

How bad things get may depend on supply. The housing market has been marked by low inventories placing ever greater upward pressure on home prices. There are two root causes. The first is that both small and institutional investors have scooped excess supply to flip or rent homes. And the second is the millions of owners who were able to hold onto their homes by modifying their mortgages through a government program through 2016. But after five years, their 2 percent interest-only payment period ends. At that point their loans will fully amortize and the mortgage rate will rise by one percentage point per year for five years. The payment shock will be enormous and could lead to an exorbitant number of homes being dumped on the market.

Two announcements in recent weeks suggest lenders have grown wise to the building risks. Home builder Lennar Corp. put Rialto Capital, its real estate lending group, up for sale. And Goldman Sachs Group Inc. said it will rein in the expansion of Marcus, its direct lending to consumers arm.

The outlook for households, and by extension the economy, is on shaky ground. Many households simply cannot weather a rising rate environment.

To contact the editor responsible for this story: Robert Burgess at bburgess@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Danielle DiMartino Booth, a former adviser to the president of the Dallas Fed, is the author of "Fed Up: An Insider's Take on Why the Federal Reserve Is Bad for America," and founder of Quill Intelligence.

©2018 Bloomberg L.P.