Hong Kong Stonewalls China's Trillion-Dollar Easing

(Bloomberg Opinion) -- The longer Hong Kong protests drag on, the less likely China will be to unleash the trillion-dollar stimulus markets seem to want. Beijing has become painfully aware that its easy-money policies of the past inflated asset bubbles and widened the wealth gap. Any repeat endeavors could risk stoking social unrest on the mainland.

Over the past decade, China flooded its economy with big-ticket outlays. There was the 4 trillion yuan ($561 billion) package after the collapse of Lehman Brothers Holdings Inc., followed by interest-rate cuts in 2014 and 2015, and 3.5 trillion yuan of shantytown redevelopment projects from 2015 to 2018, to name a few.

Lately, however, China has been conspicuously timid with its monetary tools, even as deflation hangs over the country’s producers and the trade-war standoff deepens. Sure, Beijing lowered banks’ required reserve ratio on Friday; but an outright cut to its benchmark lending rate is nowhere in sight. In fact, one could argue that the central bank bought itself some time to delay any weighty monetary-policy decisions, after last month’s tweak to the rate lenders offer their best clients.

On the fiscal side, Beijing has found a new way to finance construction projects: Issuance of special-purpose municipal bonds has hit record highs this year. Yet infrastructure spending hasn’t picked up. That’s because the Ministry of Finance has been diligently auditing local governments, sometimes bi-weekly, to ensure money is spent in the right places.

What explains this change of tune?

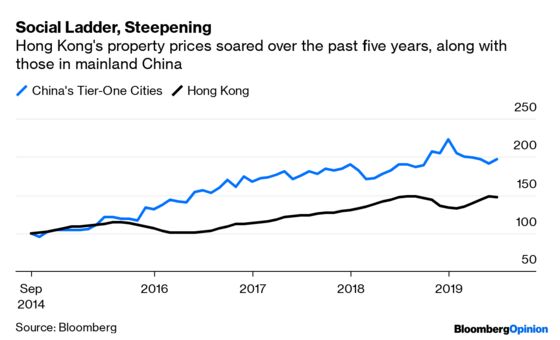

China increasingly sees Hong Kong’s sky-high home prices as the root cause of city’s turmoil, which has continued for 14 consecutive weeks. Even the country’s liaison office in the former British colony cited minsheng, or people’s livelihood, as a valid concern.

Beijing wants to prevent Hong Kong’s discontent from spreading to the mainland, aware that China is now a society of extreme income inequality, too, as measured by the Gini coefficient. Home prices in the first-tier cities of Beijing, Shanghai, Shenzhen and Guangzhou have more than doubled since 2013; as a result, young Chinese, just like their counterparts in Hong Kong, may find that climbing the middle-class ladder is getting harder.

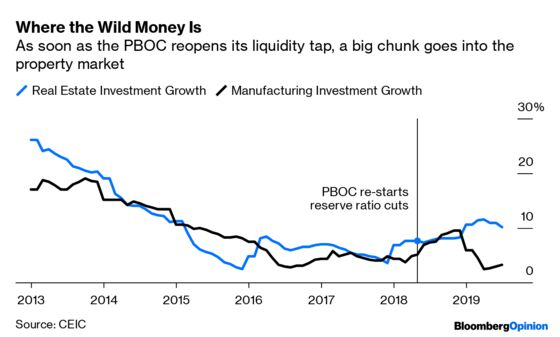

In that light, the hesitation of the People’s Bank of China to unleash an ambitious stimulus program makes sense. Whenever the central bank reopens its taps, a sizable chunk of hot money goes into real estate. The latest mini-easing proved no exception: Property investment shot up, while the manufacturing sector, hit hardest by China’s trade war with the U.S., remains anemic. President Xi Jinping’s mantra, “apartments are to be lived in, not speculated on,” hasn’t been heeded.

Meanwhile, China is using its strict audit system to discourage local governments from relying too heavily on the property market, a problem that beset Hong Kong. Last year, the city collected a quarter of its fiscal revenue from land sales, compared with roughly a third for an average mainland municipality.

To its credit, Beijing wants to prevent moral hazard: If a large chunk of government revenue comes from land sales, local officials are incentivized to keep the property bubble aloft, for instance, by nudging regional banks to dole out easy financing to developers. Shenzhen is now hailed as a model socialist city, in part because personal-income and corporate taxes account for almost all of its fiscal coffers.

Commentators have lamented that China’s reserve ratio cuts and infrastructure spending are too little, too late. They’re missing the point. With the People’s Republic of China about to celebrate its 70th anniversary, social stability is foremost on Beijing’s mind – and that means eschewing the generous stimulus packages that tend to benefit the wealthy and sow the seeds of unrest.

To contact the editor responsible for this story: Rachel Rosenthal at rrosenthal21@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Shuli Ren is a Bloomberg Opinion columnist covering Asian markets. She previously wrote on markets for Barron's, following a career as an investment banker, and is a CFA charterholder.

©2019 Bloomberg L.P.