(Bloomberg Opinion) -- That was quick. Workers in Hong Kong’s finance industry returned to the office after a long weekend of violent protests to find that their stock exchange has decided not to pursue a takeover bid for its London counterpart.

The limp end to its month-long courtship has left Charles Li, chief executive officer of Hong Kong Exchanges & Clearing Ltd., looking rather silly. One can’t help wondering if the exchange has any leadership, vision or ambition left.

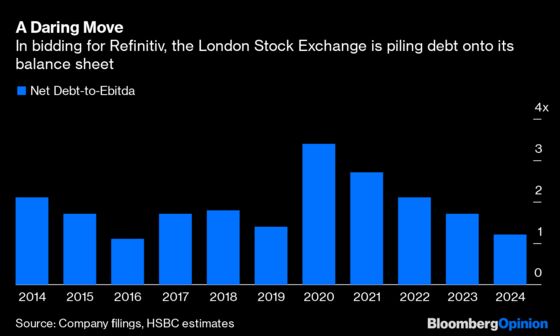

The same can’t be said of London Stock Exchange Group Plc. By bidding for Refinitiv, the LSE is taking on a lot of risk. On completion of the deal, the exchange’s net-debt-to-Ebitda ratio would rise to 3.5 times, well above the 1 to 2 times range that its management deems comfortable. It will take the LSE more than two years to bring its debt level back down – and even that estimated time scale is seen as ambitious by analysts. Yet the London exchange is charging ahead, in the face of Brexit and a deteriorating global economic outlook, to diversify away from trading revenue that’s being eroded by the rise of passive investing.

HKEX’s pursuit was half-hearted at best. With a squeaky-clean balance sheet, the company could have done a lot more. If it had been willing to bring its leverage ratio to the same level that LSE is tolerating, HKEX would have had more than $18 billion in cash to sweeten its offer. While LSE management was scathingly dismissive of the HKEX offer, many of its shareholders might well have been tempted – especially if the Hong Kong exchange had increased the cash component of its bid. After all, immediate cash-on-hand is always appealing for passive fund managers, which account for almost all of LSE’s ownership.

What’s left for Hong Kong? The 200,000-odd finance professionals employed in the city will be asking themselves. HKEX CEO Li, who earned HK$29 million ($3.7 million) last year, likes to talk up Hong Kong as the gateway for foreign capital to China. Reality suggests otherwise. Wary that the Trump administration will limit U.S. investments into China, American fund managers are already tiptoeing away. They got their latest warning on Monday, when Hangzhou Hikvision Digital Technology Co. was placed on a U.S. blacklist. In 2018, foreigners owned more than 10% of the surveillance camera maker.

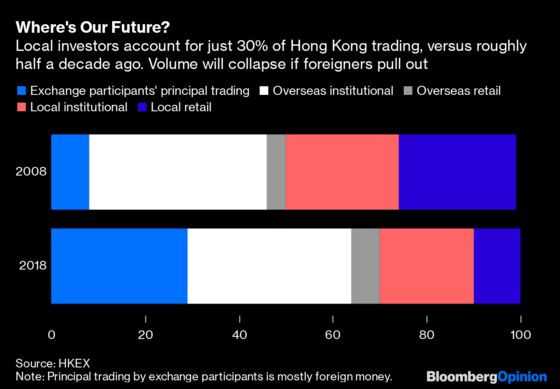

Local retail and institutional investors accounted for only 30% of HKEX trading last year, according to the exchange. Americans are the second-largest outside investors, after those from mainland China, accounting for 10% of Hong Kong’s total trading. The actual number is likely to be quite a bit higher, as U.S. banks also trade Hong Kong stocks using their principal accounts. Billions of dollars will flee as U.S.-China trade tensions escalate.

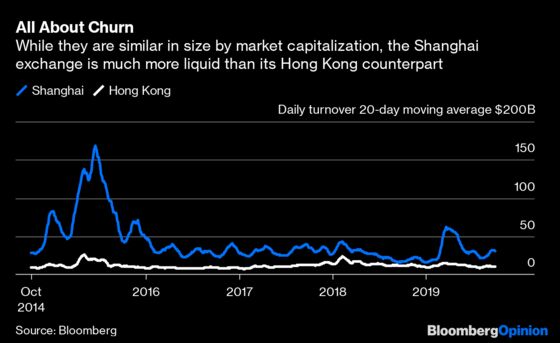

Those still brave enough to stick around may look to the mainland market instead. China’s announcement that it will remove quotas on buying Chinese stocks and bonds in September is a clear sign that Beijing is looking for an onshore alternative to Hong Kong. There’s something to be said for the Chinese market: While the Shanghai and Shenzhen exchanges are near par with Hong Kong by market cap, stocks there are a lot more liquid.

At times of economic distress in the mainland, state-owned enterprises routinely perform national service, piling on debt to build roads to nowhere and provide employment. With almost half its board appointed by the Hong Kong administration and its chairman picked by the city’s chief executive, HKEX has the characteristics of a local government financing vehicle in China. So why is the exchange so timid in its drive to maintain Hong Kong’s relevance as a financial center? HKEX shareholders may be cheering after it dropped the LSE bid. Many finance workers won’t be.

To contact the editor responsible for this story: Matthew Brooker at mbrooker1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Shuli Ren is a Bloomberg Opinion columnist covering Asian markets. She previously wrote on markets for Barron's, following a career as an investment banker, and is a CFA charterholder.

©2019 Bloomberg L.P.