Here's Why Betting on a BOJ Rate Cut May Be Doomed to Fail

Here’s why betting on a Bank of Japan rate cut may be doomed to fail.

(Bloomberg) -- Think twice before betting the Bank of Japan will cut interest rates.

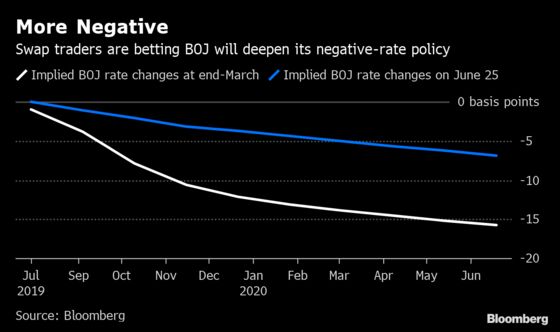

Speculation the central bank will act has been growing in recent weeks, with the main argument being policy makers will follow any Federal Reserve rate cut to prevent the yen from strengthening. The BOJ will lower short-term rates as soon as September, JPMorgan Chase & Co. said in a new forecast this month.

A strong yen is typically one of major catalysts for the BOJ to cut rates. The currency has risen against all its Group-of-10 peers this quarter as investors sought haven assets amid escalating trade and geopolitical tensions. Hedge funds are anticipating further gains, swinging to a net long position on the currency for the first time in a year.

BOJ Governor Haruhiko Kuroda left the door open for further easing last week, saying policy makers wouldn’t hesitate to act if the economy slows.

All well and good -- but there are other factors at play right now that mean a BOJ rate cut is not a given just yet.

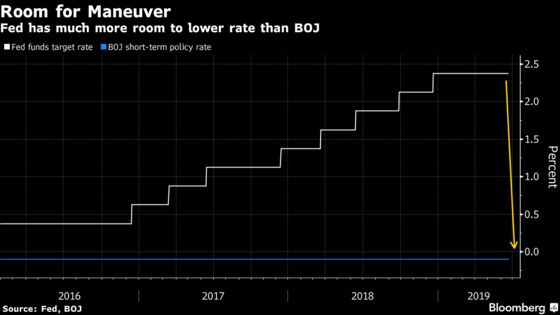

One argument for a BOJ rate cut is that Fed easing would shrink the dollar’s yield premium over the yen, and boost Japan’s currency. The U.S. central bank however has room to cut rates far more times than Japan, meaning the BOJ would be unable to stop the yield differential from narrowing by simply lowering its own rates.

“There’s no need for the BOJ to start a rate-cut competition that it can never win,’’ said Daisuke Karakama, chief market economist at Mizuho Bank Ltd. in Tokyo. “BOJ policy easing would be useless” in preventing yen appreciation, he said.

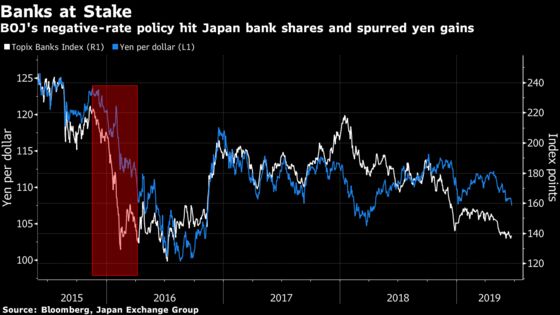

Another reason to deter the BOJ from reducing borrowing costs is this: local banks have suffered under its negative-interest-rate policy and it may be reluctant to add to their burden. The introduction of NIRP in January 2016 saw the Topix Banks Index tumble 26% in the following two weeks. Far from weakening the yen, the financial concerns saw the currency strengthen more than 7% in the same period.

“A BOJ rate cut would be a factor to worsen bank earnings,” said Koichi Sugisaki, a strategist at Morgan Stanley MUFG Securities Co. in Tokyo. “Such a policy move would just reduce interest rates on bank loans rather than reduce funding costs for financial companies. It would be economically meaningless.”

The BOJ may also decide it doesn’t need to cut short-term rates because it has other policy instruments with fewer side effects. The central bank’s steady tapering of bond purchases since 2016 has opened up the possibility it could pause them for a period and allow bond yields to fall below the lower end of its plus/minus 0.2% range to weaken the yen.

The central bank left purchases of one-to-five-year bonds unchanged Wednesday as part of its regular operations.

There’s no need to take an overly strict view on the yield range and it’s appropriate to think flexibly, BOJ Governor Haruhiko Kuroda said last Thursday when the central bank held policy. The BOJ left the purchase amounts at its regular bond-buying operation unchanged the following day, which traders saw as an endorsement of lower yields.

“Kuroda is pretending to be steering toward easing with a flexible stance,” said Ayako Sera, a strategist at Sumitomo Mitsui Trust Bank Ltd. in Tokyo. But, “Kuroda’s true intention must be that he doesn’t want to make any move,” she said.

To contact the reporters on this story: Masaki Kondo in Tokyo at mkondo3@bloomberg.net;Chikako Mogi in Tokyo at cmogi@bloomberg.net

To contact the editors responsible for this story: Tan Hwee Ann at hatan@bloomberg.net, Nicholas Reynolds

©2019 Bloomberg L.P.