(Bloomberg Opinion) -- Don't cheer too early for the yuan's renewed strength. It's largely a reflection of a weakening dollar, and that trend isn't guaranteed to persist.

The outlook for China's currency has turned around, helped by progress in trade talks with the U.S. and, particularly, the Federal Reserve's shift to a more cautious policy stance. Having flirted with the psychologically important level of 7 per dollar last year, the yuan is at its strongest since July and heading for its best week since 2005.

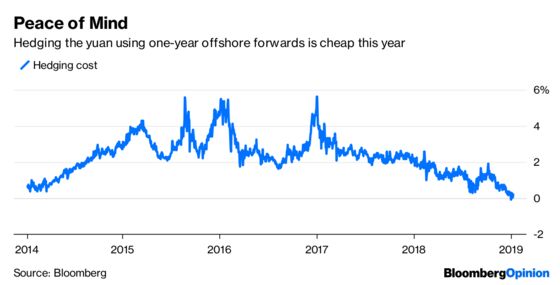

Predicting currencies is a fool's errand, though. Rather than trying to forecast the direction of future exchange rates, dollar-based investors in yuan assets should take advantage of the U.S. currency’s weakness and hedge now. The costs of protection have become far cheaper: hedging the yuan with offshore one-year forwards will set you back only 0.2 percent, compared with 5.6 percent at the beginning of 2017 and 2.2 percent at the start of 2018.

The yuan’s rally is part of a broad comeback for emerging-market currencies this year. The Brazilian real leads the Fragile Five club (which also includes India, Indonesia, Turkey and South Africa) with a 4.4 percent gain. The Chinese currency is up about 1.7 percent.

The Fed’s dovish turn has widened the expected differential between U.S. and emerging-market interest rates, making currencies of the latter more attractive. The implied rate of the December 2019 Fed funds futures has fallen to 2.43 percent this week from 2.93 percent in early November. Futures traders see no further tightening this year.

That’s logical given what’s happening to the U.S. economy. Having been supercharged by President Donald Trump's corporate tax cut last year, growth looks to be slowing. Across industries, bellwether companies from courier FedEx Corp. to retailer Macy’s Inc. have pared back their sales outlooks.

Traders are again paying attention to interest rate parity, which governs the theoretical relationship between interest-rate differentials and spot and forward foreign-exchange rates. But these are theories only. Unexpected events can interfere.

Take the collapse of Lehman Brothers Holdings Inc. a decade ago. Even with the U.S. on the brink of a financial crisis, the dollar rallied 15 percent in the space of two months. When fear grips, the greenback is the ultimate refuge. It’s still often referred to as the “beautiful gold” in China.

In the case of emerging-markets currencies, fiscal and current-account deficits may be more important to watch than interest-rate differentials.

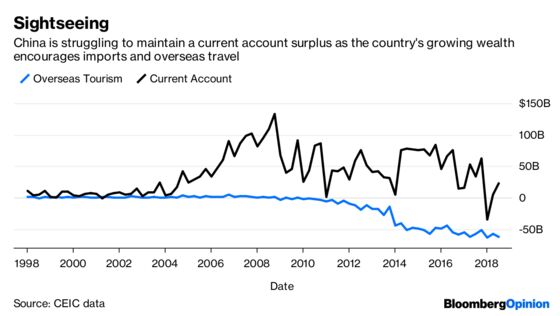

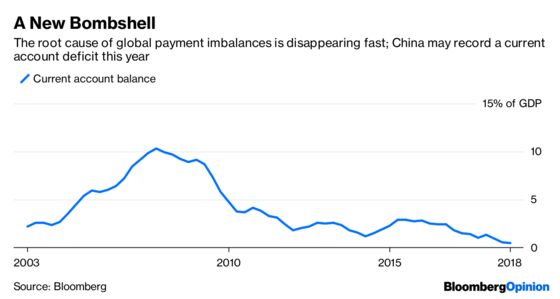

A new bombshell may drop from China in 2019: its first current-account deficit in more than two decades. This is a huge deal for the world: After all, China’s current account surpluses were the root cause of global payment imbalances, surpassing 10 percent of GDP as recently as 2007.

Slower export growth – driven by the trade spat with the U.S. and the global economic slowdown – will put a dent in the country’s external accounts. But the picture is more nuanced than that. China is no longer a frugal nation, selling a lot abroad and buying little back. In the third quarter, China’s middle class spent about $63 billion on overseas travel. This is eating away the hard-won surplus earned by exporters.

This brings us back to interest-rate parity. Thanks to the theorem’s renewed primacy in foreign-exchange markets, it’s becoming cheaper to take risk off the table in such an uncertain environment. Investors should take advantage.

To contact the editor responsible for this story: Matthew Brooker at mbrooker1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Shuli Ren is a Bloomberg Opinion columnist covering Asian markets. She previously wrote on markets for Barron's, following a career as an investment banker, and is a CFA charterholder.

©2019 Bloomberg L.P.