Hedge Funds Now Burned by Trades That Worked for Decades

Hedge Funds Now Burned by Trades That Worked for Decades

(Bloomberg) -- The sudden breakdown of a decades-long relationship between U.S. and Asian stocks has blindsided hedge funds, turning what were meant to be low-risk bets on volatility into big money losers.

Managers including Nine Masts Capital Ltd. and Myriad Asset Management Ltd. suffered losses in March on wagers that equity-market swings in Asia would be more extreme than those in the U.S. or Europe, according to people with knowledge of the matter. The bets were widespread among traders who focus on volatility, said Govert Heijboer, co-chief investment officer of Hong Kong-based True Partner Capital, a $1.4 billion hedge fund firm whose flagship volatility product gained 10% in March.

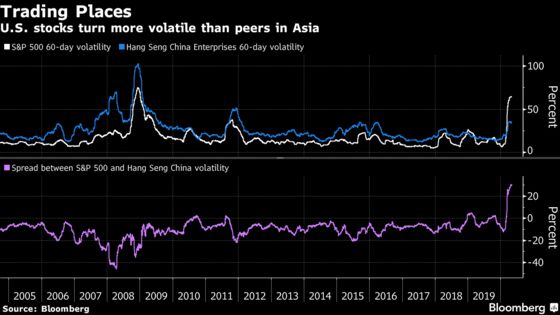

While the trades performed well in back tests over three decades, and produced big returns during the 2008 financial crisis, they fell apart in March as the coronavirus pandemic roiled global stocks. Swings in the S&P 500 Index soared far above those of benchmark gauges in Asia -- hitting a record versus Chinese shares in Hong Kong and touching the highest levels relative to Japanese and South Korean equities since Wall Street’s Black Monday crash in 1987.

The dramatic reversal highlights the risk of relying on historical market relationships to guide investments, an approach that has come under renewed scrutiny this year as many quantitative funds underperformed their benchmarks. Opinions differ on why the link between U.S. and Asian volatility broke down, but some investors have pointed to the growing complexity of U.S. market structure and the stabilizing presence of government funds and central banks in Asia. America has also become the new epicenter of the pandemic, with confirmed cases skyrocketing in March even as infection rates across much of Asia leveled off.

“Being long Asia versus short U.S. volatility worked in 2008, so it back tested well as a trade for stressed environments” Heijboer said. “In practice, it turned out otherwise.”

Nine Masts’ relative-value hedge fund lost 23.5% in March, mostly due to wagers that Asia index price swings would outstrip those in the U.S., according to people with knowledge of the Hong Kong-based firm. Myriad, also based in Hong Kong, ended the month with double-digit losses, said a person familiar with the matter. Its small derivatives book represented its largest losing strategy because of extreme moves in U.S. and European volatility, one of the people said. Representatives for the firms declined to comment.

| Read more on turbulence at volatility-focused hedge funds: |

|---|

| LMR Shutters Two Hedge Funds to Focus on Main Money Pools |

| BTG Closes Volatility Hedge Fund, London Trading Head Exits |

| Ex-Goldman Duo’s Fund to Shut After Volatility Bets Go Awry |

| La Francaise Is Charging Investors to Exit One of Its Funds |

Hedge fund wagers on price swings have swelled in recent years in part due to a steady supply of volatility exposures generated by the structured products desks of big investment banks. In a process sometimes called “risk recycling,” many banks have been offloading these exposures to their trading clients to comply with stricter post-2008 financial regulations.

One of the instruments favored by hedge funds -- the corridor variance swap -- allows for bets on relative volatility but can lead to outsized losses when markets move in the wrong direction. Such swaps contributed to the March downturn at Nine Masts, which oversaw $1.1 billion at the end of February and had made money in nine of the last 10 years. Myriad, which managed $4 billion at the end of 2019, also invested in the swaps. In March, the firm’s multistrategy hedge fund suffered the worst monthly performance in its eight-year history.

La Francaise Investment Solutions’ LFIS Vision Premia Opportunities Fund, which has invested in corridor variance swaps and other similar instruments in recent years, saw its net asset value drop about 23% in March. While the firm hasn’t disclosed details of its losing trades, it said in a March filing that the market environment was “unprecedented, with financial parameters at historically distorted levels and liquidity severely impacted.” La Francaise declined to comment.

The trades have been a “disaster” for some hedge funds, said Bharat Sachanandani, head of Asia-Pacific flow strategy and solutions at Societe Generale SA. They were based on the assumption that “when the U.S. sneezes, Asia catches a cold and vols spike much higher,” Sachanandani said. “It didn’t happen.”

One factor behind the subdued swings in Asia may have been the stabilizing effect of Chinese government intervention in the economy and markets, said Steve Diggle, who made $2.5 billion from volatility trades at Artradis Fund Management Pte between 2007 and 2008.

China’s central bank has kept the financial system flush with liquidity this year, while the so-called National Team of state-backed funds has helped underpin confidence in stocks after stepping in to support prices in the wake of a market crash in 2015. The sanguine mood has also buoyed Hong Kong shares, which attracted a record HK$137.9 billion ($18 billion) of net inflows in March via exchange links with the mainland.

Meanwhile in Japan, the central bank has been pouring money into Tokyo-listed exchange-traded funds as part of its unorthodox monetary stimulus program -- often buying on days when the stock market declines. The Bank of Japan owned an estimated 31 trillion yen ($290 billion) of ETFs at the end of March, according to NLI Research.

U.S. stocks have also gotten plenty of indirect support from the Federal Reserve. But the market has nonetheless become more vulnerable to sudden price swings as central bank stimulus fueled the popularity of leveraged investment strategies that are structurally short volatility, according to Gwilym Satchell, a fund manager at Invesco.

When shocks like the pandemic force leveraged U.S. investors to unwind their bets on low volatility, the argument goes, bouts of market turbulence are amplified. Some analysts blamed the phenomenon for sharp swings in U.S. stocks in late 2018, one of the rare periods before this year when the S&P 500 became more volatile than Asian counterparts like the Hang Seng China Enterprises Index. Up until March, 60-day swings in the U.S. gauge had been smaller than the Chinese index more than 90% of the time since Bloomberg began compiling the data in 1993.

Satchell said he was also positioned for Asian stock swings to exceed those in the U.S. but hedged his exposure to protect against an extreme move in the other direction. He ended up making about $150 million from the trades in March, skirting what could have been a $120 million loss without the hedge.

What happens next is far from clear. It’s possible that March was just a blip and that the historical U.S.-Asia volatility relationship will reassert itself. But for True Partner’s Heijboer, that’s a risky bet.

“It is difficult to predict,” he said, citing uncertainties around structured product sales, the economy and the varying impact of the virus. “There are many moving parts.”

©2020 Bloomberg L.P.