Hedge-Fund Longs, Hawkish Rate Bets Mean Kiwi Has Room to Fall

Hedge-Fund Longs, Hawkish Rate Bets Mean Kiwi Has Room to Fall

(Bloomberg) -- There’s a wealth of positive news out there for the New Zealand dollar. All the more reason it may be poised to weaken.

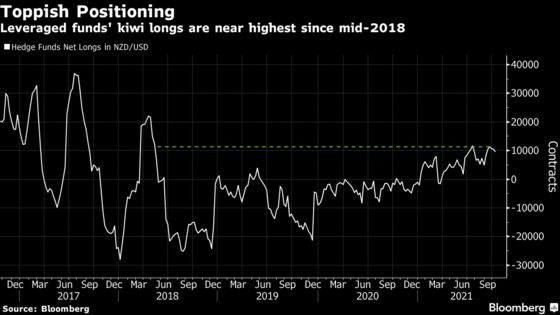

Leveraged funds’ long positions are near a three-year high, while traders are pricing in more than a 90% chance of another central-bank interest-rate hike next month. With all this good news already in the price, there is plenty of room for disappointment.

There are a number of possible catalysts that may convince the Reserve Bank of New Zealand to delay its intended interest-rate hikes. These include any worsening in the current Covid outbreak or a slowdown in the pace of job creation -- both factors it has flagged as possible reasons to delay tightening.

At the same time there is a big underlying negative. The Federal Reserve has reaffirmed its commitment to cut back on bond purchases as it progresses toward normalizing policy, which will create a consistent bid for the U.S. dollar.

“We see limited further upside for NZD/USD because interest-rate markets are fully pricing an RBNZ rate-hike cycle, while we still see room for U.S. markets to adjust their Fed Funds rate expectations higher,” said Kim Mundy, a currency strategist at Commonwealth Bank of Australia in Sydney.

In addition, “the prolonged Covid-19 restrictions in New Zealand can weigh on NZD if it causes interest-rate markets to reassess the outlook for RBNZ rate hikes,” he said.

Overnight index swap markets are pricing in a 92% chance of a 25 basis-point rate increase at the next RBNZ meeting on Nov. 24, and an 86% probability of an additional one at its following gathering in February. The central bank has a track record of doing the unexpected. It raised its benchmark for the first time in seven years on Oct. 6, but only after disappointing hawks that had expected a move in August.

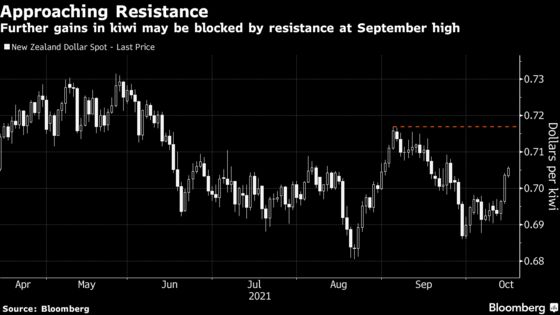

Technical analysis also identifies a challenge. While the kiwi-U.S. dollar exchange rate climbed above 0.70 last week from September’s low of 0.6860, it is now approaching resistance at last month’s high of 0.7170. A failure to breach that level may send it moving lower again.

The kiwi faces a more immediate threat in the form of inflation figures due Monday. Economists surveyed by Bloomberg predict consumer prices probably accelerated to at an annual rate of 4.2% last quarter. If the reading falls short of that, then more doubts may start to creep in as to whether a November rate hike is really a done deal.

Here are the key Asian economic data due this week:

- Monday, Oct. 18: New Zealand 3Q CPI, China 3Q GDP, retail sales, industrial production, and fixed asset ex-rural, RBA’s Heath speaks, Singapore non-oil domestic exports

- Tuesday, Oct. 19: RBA minutes, Bank Indonesia rate decision

- Wednesday, Oct. 20: China 1- and 5-year loan prime rate, Japan trade balance, Taiwan export orders

- Thursday, Oct. 21: Australian 3Q business confidence, South Korea 20-day exports/imports, New Zealand credit card spending,

- Friday, Oct. 22: RBA Lowe speaks, Japan CPI and PMIs, Malaysia CPI, Thailand customs trade balance

©2021 Bloomberg L.P.