HDFC Bank’s Margins to Lure Investors as Indian Rivals Struggle

HDFC Bank Ltd. reported net income growth of nearly 18% and ramped up bad loan provisions in the latest quarter

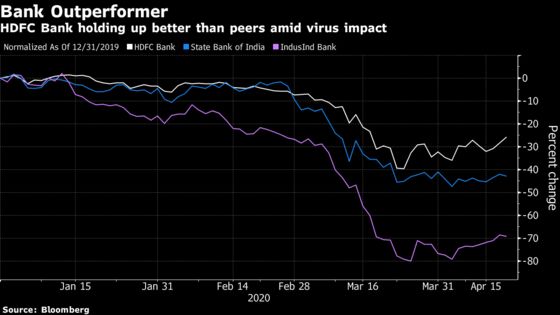

Analysts remain bullish on HDFC Bank, with an average rating of 4.76 on a Bloomberg scale where 5 is a unanimous buy. The lender is seen being able to better withstand the pandemic impact due to its position as a market leader. Its shares are down 26% this year, the least of all Nifty Bank Index members. The stock climbed as much as 5.6% on Monday and was headed for its highest close since March 17.

“HDFC Bank’s business growth remains robust despite economic activity getting impacted due to the Covid-19 outbreak,” Nitin Aggarwal, an analyst with Motilal Oswal Financial Services Ltd., said in a note. “A strong liability franchise will support margins, while higher liquidity levels would enable the bank to ride the current crisis and gain further market share.”

The bank’s net income rose to 69.3 billion rupees ($907 million) in the quarter ended March 31, compared with an average 72.5 billion rupees estimate in a survey of eight analysts. Provisions against soured debt jumped to 37.8 billion rupees from 18.9 billion rupees a year ago.

“The bank could take market share from India’s large public lenders, with a retail portfolio likely to stay second only to State Bank of India,” Diksha Gera, an analyst with Bloomberg Intelligence, said in a note.

Despite the optimism over HDFC Bank, market participants remain cautious on the sector overall. India financials have been reeling from a shadow-banking crisis that culminated in the Yes Bank Ltd. bailout. The pandemic struck just as lenders were about to see signs of stability. The Reserve Bank of India has moved to further ease liquidity and bad-loan rules to keep funds flowing through the economy.

“If a bad loan cycle begins for retail, the fear psychosis of taking risk off the table will reduce the credit to the segment,” said Kenneth Andrade, chief investment officer at Old Bridge Capital Management Ltd, overseeing assets of $400 million.

Here’s a roundup of analyst comments on HDFC Bank’s results:

Axis Capital Ltd. (Manish Karwa)

- Growth likely to be steady despite bank’s tightening of its credit filters resulting in higher rejections of loan applications.

- Rural strategy on track; investment in digital is leading to strong build-up of deposit base.

- Reduces growth estimates for both loans and fee income as retail will slow down sharply.

- Rated buy, price target 1,250 rupees

ICICI Securities Ltd. (Sandeep Joshi)

- HDFC Bank better positioned to weather the storm; however, in times of economic dislocation, it is sensible to remain conservative.

- Expects bank’s loan growth to moderate to 12%, net interest margin to contract by 9 basis points and credit cost to be elevated at 1.7% in FY21.

- Near-term earnings impact doesn’t overshadow bank’s balance sheet strength, competitive advantage.

- Maintains buy with price target cut to 1,339 rupees from 1,604 rupees

Prabhudas Lilladher (Pritesh Bumb)

- Contingency provisions to cushion shocks from nasty surprises; early part of FY21 remains uncertain on business & asset quality.

- Bank stress tested its loan portfolios and things are quite manageable; confident on its risk assessment process.

- Retains buy with price target lowered to 1,105 rupees from 1,124 rupees

Kotak Institutional Equities (M.B. Mahesh)

- Early commentary on impact of coronavirus is not as bad as expected.

- Valuations attractive.

- Bank well positioned to navigate crisis despite larger exposure than peers to some sectors that could be impacted by economic downturn.

- Maintains buy with fair value unchanged at 1,050 rupees

©2020 Bloomberg L.P.