Harvard's Reinhart Sees Rising Risk of Big Emerging-Market Sovereign Defaults

Harvard's Reinhart Sees Rising Risk of Big Emerging-Market Sovereign Defaults

(Bloomberg) -- Carmen Reinhart, the Cuba-born economist whose warning in May of emerging-market perils proved prescient, says things may get worse in 2019 as rising U.S. interest rates, slower Chinese growth and potential defaults put more stress on the developing world.

"Markets are pricing in bad stuff, but not necessarily a credit event," the Harvard professor said in an interview from Cambridge, Massachusetts, naming Argentina, Ecuador and Costa Rica among her top concerns. "I still go back to that as my number one factor that could really shake things up."

What’s your outlook for EM in 2019?- "It’s not great. I can’t emphasize enough that during the 2007-2009 global financial crisis, what made EM snap back strongly was China. From 2003 to almost 2013, it consistently grew over 10 percent per year. That’s unlikely in 2019. You have a slowing economy with over-leveraging of the corporate sector. There’s an overvalued currency, capital outflows and trade concerns with the U.S. It’s hard to make a case that 2019 is a growth rebound in China or in other advanced economies."

- "The last crisis was coupled with strong growth in China and sharply lower interest rates. So you closed one door but another door opened. Now, U.S. rates are poised to increase. China will, on the whole, trend toward slower growth and be more reticent about lending abroad than the previous decade. For a country like Ecuador, that’s a big thing."

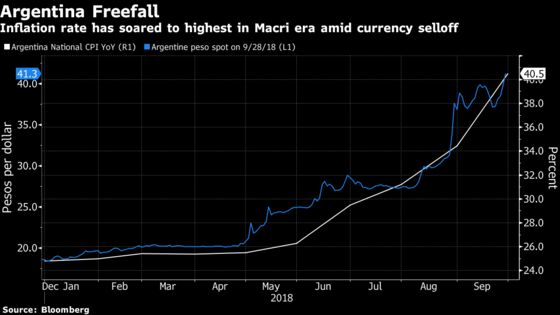

- "Argentina continues to be the weakest of the set. They don’t have much margin for any kind of error or negative surprises."

Can we see a rebound in any of this year’s laggards?- "Argentina has a very narrow, frail path. They’re keeping rates high with the aim of stabilizing the peso. They seem to be getting some traction. You would say that’s really good. But the stabilization isn’t translating immediately to dampening inflationary pressures. Inflation runs higher than the rate of depreciation, so the competitiveness gained from the peso slide is being lost again. You need a weak peso in real terms to close your current-account deficit. At the same time, you don’t need a weak peso because they’re a dollar-debt economy, unlike Brazil. You’re in a situation where you’re damned if you do and damned if you don’t."

- "Brazil has a serious debt problem. They have a fiscal problem and unlike Argentina, it’s a real problem not a dollar problem. The worst part is they don’t have much discretionary spending on the fiscal side. Their fiscal outlays are mostly transfers and debt servicing. It’s not like the government has a lot of room to show big improvements in the short run. I think sooner or later Brazil’s answer will be inflation again."

- "Turkey’s problem from the get-go was the private corporate debt rather than government debt. They have lessened their reliance on external flows and closed their current-account deficit at an impressive clip. That lessens their immediate vulnerability because they need less funding. However, that doesn’t mean they look good."

Will new Latin American leaders boost markets?

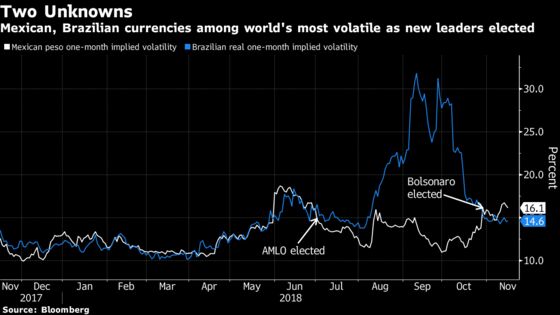

- "In Brazil, Jair Bolsonaro was seen as the lesser of two evils. It’s not that he was a great choice. It’s not like this guy has a vision. You had a breath of relief. We’ll see how long it lasts. It’s a very dysfunctional situation. There’s fragmented decision-making. Let’s say he takes the bull by the horns and says we have to tackle our pension problem. It will do a lot to confidence if he succeeds. However, the fiscal effects are delayed. It would be more about mustering confidence."

- "Latin America has a long, dark history of military governments. Democracy is not something you can take for granted. In good times, you tend to see more liberalization of markets and less capital controls, and the reverse in harder times. There is that element right now that if conditions, as I would expect, remain difficult, that it increases the probability of backtracking. Policy reversals usually come in bad times."

- "In Mexico, markets talked themselves into believing that AMLO (Andres Manuel Lopez Obrador) would be maybe another Lula because his campaign remarks had been on the moderate side. Then more recently, of course, just before he takes office, the reaction has been, ‘Gee, maybe what he’d been saying the last 30 years is still what he believes.’"

- "You never know what a good scare will do. If markets get spooked and the peso goes on a big slide, you might get religious very quickly or you might not. In Turkey, Recep Tayyip Erdogan was for a long while voicing strong opinions that he didn’t believe raising rates was the way to go, and then the cumulative slide in the lira changed that. Certainly, AMLO’s leanings and recent YouTube videos don’t seem to suggest that he is the more moderate guy we saw at election time. We don’t see that."

What risk do trade tensions pose?- "What’s the worst-case scenario? You end up with a big hike in tariffs across the board. There’s been much discussion about supply chain disruptions and output consequences but such a big pop in tariffs across the board would also act like a supply shock, which in the 1970s also was associated with a price spike. Back then, you saw big increases in the prices of washing machines. If somehow the outcome of Trump and Xi’s discussions ends up being an across-the-board hike in tariffs which then leads to a price spike in the U.S., that really complicates things. What does the Fed do? Do they say this is a once-and-for-all increase? How do interest rates react? That could be a real adverse outcome of all of this."

Where do you see bright spots?- "There are EMs that look pretty good in terms of resilience. Take for example Peru. It’s hard to make the case that their vulnerabilities are any higher now than they were a while ago. Their external debt has been pretty stable. Thailand is another stable country relative to a lot of the jitters in Indonesia and the Philippines. They’re not issuing a lot of debt. It’s not like these are countries that have been big in tapping international capital markets, which is perhaps why they’re relatively attractive. Their vulnerabilities haven’t increased."

- "Colombia is not great, but relative to the other concerns, certainly isn’t alarming. Within EMs, the ones that are the most desirable are the ones that are most elusive. One rough cut you can make is those that depend less on international funding are going to do better. Those that have a more variable rate of short-term debt will, all things being equal, do worse, because your funding costs are simply higher."

To contact the reporter on this story: Ben Bartenstein in New York at bbartenstei3@bloomberg.net

To contact the editors responsible for this story: Rita Nazareth at rnazareth@bloomberg.net, Alec D.B. McCabe, Brendan Walsh

©2018 Bloomberg L.P.