Growth Fears Leave ECB Exposed as Negative Rate Relief Doubted

Money markets are pricing in a 40% chance that the ECB will cut rates by the first quarter of 2020.

(Bloomberg) -- Go inside the global economy with Stephanie Flanders in her new podcast, Stephanomics. Subscribe via Pocket Cast or iTunes.

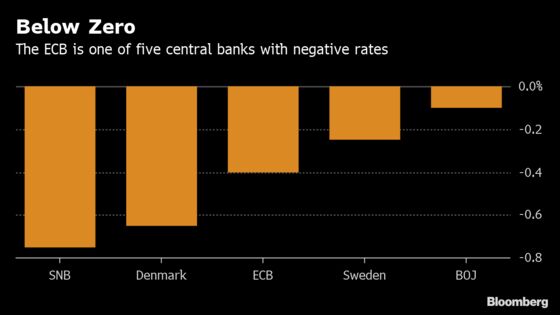

European Central Bank officials dragging their feet over a potential revamp of their negative interest rates might be shutting off one way to convince investors they are serious on stoking inflation.

Money markets are pricing in a 40% chance that the ECB will cut rates by the first quarter of 2020. Some traders have capitulated on bets for higher borrowing costs because of global trade tensions and renewed concern over Italian debt, while others have been burned by a rally in German bonds that has pushed yields down to the lowest since 2016.

Yet unlike counterparts with even lower borrowing costs, the Frankfurt-based ECB lacks a system to lessen the squeeze on lenders’ profitability by exempting part of their reserves from the negative deposit rate. That makes it hard to perceive further rate cuts for now, unlike at the U.S. Federal Reserve, which has raised rates enough to have space to lower them again if global growth goes awry.

“People complain that the Fed doesn’t have many bullets to combat the next recession because rates are still historically very low,” said John Taylor, a money manager at AllianceBernstein Holding LP in London. “By comparison, the ECB don’t even have a gun.”

While ECB President Mario Draghi first touted the possibility of softening the impact of negative rates in March, his fellow policy makers have shown little enthusiasm and in some cases outright opposition to the idea. A surprise pickup in euro-region growth data has also eroded any urgency to address the matter.

Still, perhaps more worryingly, a gauge of inflation expectations has slumped close to the lowest since 2016, giving investors reason to suppose that officials might need to add stimulus.

So-called tiering of the deposit rate would open up the possibility of cutting it further if needed from the current minus 0.4%. It might also offer a tactical option to respond to any Fed rate reduction that narrows the difference with the ECB’s borrowing costs and strengthens the euro.

The case for easier policy in the U.S. and elsewhere is bolstered by evidence of a global slowdown. Bundesbank President Jens Weidmann said on Thursday that an escalation of the trade dispute between the U.S. and China would be “poison” for the world’s economic prospects.

“If the Fed were to cut, it’s more likely that the ECB will have to do something,” said Christian Keller, head of economics research at Barclays Bank Plc. “If you have tiering in place, you protect banks that have a large liquidity surplus. That by implication means that you could either keep negative interest rates for longer -- or you could probably try to go from minus 40 basis points to minus 50.”

Officials last formally considered the prospect of tiering in March 2016, citing the “complexity” for deciding against such a structure even as they cut the deposit rate to its current level.

Bank of France Governor Francois Villeroy de Galhau most recently pushed for a rethink this March. Later that month, Draghi publicly aired the idea of some kind of mitigation of the impact on banks.

The move met with little enthusiasm, and ECB Executive Board member Benoit Coeure this week signaled that officials are in no rush to soften the policy. Weidmann, who favors stimulus withdrawal, poured more cold water on the idea, saying that the net effect could be be negative by postponing a monetary policy normalization.

The problem for the ECB is that its current sub-zero regime risks limiting its easing options, narrowing the toolkit to existing measures such as a proposed extension of long-term loans for banks.

The Innovators

For now, policy makers can take comfort in an economy that is enjoying the lowest unemployment since 2008, rising wages and an unexpected pace of expansion in the first quarter. That propitious combination has eased concerns that they might need to cut their forecasts again at their June 6 decision after already dramatically lowering them in March.

However, experience under Draghi also suggests the ECB will still find a way to respond to a worsening outlook if it needs to.

“The ECB has a pretty impressive track record of being quite innovative in terms of coming up with additional measures when we do get an environment where they’re obliged to ease policy further,” said Anton Heese, European macro strategist at Morgan Stanley Investment Management. “We could see further innovative easing measures coming up.”

--With assistance from Stephen Spratt.

To contact the reporters on this story: John Ainger in London at jainger@bloomberg.net;Craig Stirling in Frankfurt at cstirling1@bloomberg.net

To contact the editors responsible for this story: Paul Gordon at pgordon6@bloomberg.net;Ven Ram at vram1@bloomberg.net

©2019 Bloomberg L.P.