China’s Stimulus Debate Is Still Alive After Grim Trade Data

A 16% contraction in shipments to the U.S. highlighted the damage that the trade war is doing.

(Bloomberg) --

The contraction in China’s trade in August underscored what economists were already saying about the government’s stimulus efforts: they’re not yet enough to put a floor under the slowing economy.

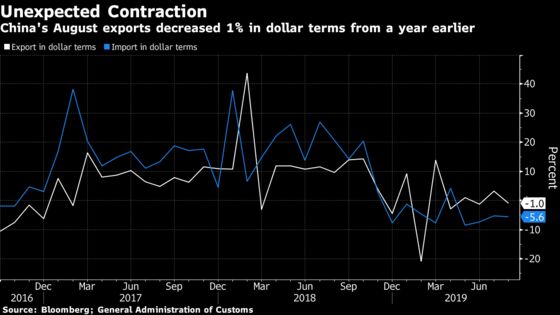

Data released Sunday showed that exports decreased 1% in dollar terms from a year earlier last month, a period when companies could have been expected to try to increase cargoes to the U.S. ahead of higher tariffs that kicked in Sept. 1. Instead, a 16% contraction in shipments to the U.S. highlighted the damage that the trade war is doing.

That makes the injection of $126 billion into the economy announced by the central bank on Friday look more like a cautious move that will need to be followed by further steps if the government wants to keep economic growth above the key 6% level. Yet the fear of a bubble in the property market could still preclude larger-scale action.

“More policy easing will be needed to help stabilize domestic economic growth,” Louis Kuijs, chief Asia economist at Oxford Economics in Hong Kong, wrote in a note Sunday. “The key downside risk to our outlook for growth and imports is policymakers not stepping up policy support sufficiently.”

The State Council, China’s cabinet, last week signaled more stimulus measures are coming, though that raises the perennial question of which selection of tools best does that job while keeping debt under control.

On top of the reserve-ratio cut announced Friday, more government debt sales are in the pipeline. Some in financial markets also expect a cut in the interest rate on the central bank’s medium-term loans to banks, though policy makers skipped an opportunity to do that on Monday.

Here’s a recap of China’s main stimulus measures this year and how they’ve worked:

RRR

Before Friday, the People’s Bank of China had cut banks’ reserve ratios twice this year, unleashing cash to help banks lend more. In the latest move, the required reserve ratio for all banks will be lowered by 0.5 percentage points, taking effect on Sept. 16, the People’s Bank of China said. The PBOC also cut the reserve ratios by one percentage point for some city commercial banks, to take effect in two steps on Oct. 15 and Nov. 15.

The cuts will release 900 billion yuan ($126 billion) of liquidity, the PBOC said, helping to offset the tightening impact of upcoming tax payments.

However, Nomura International Ltd has warned markets to be conservative in estimating the potential of RRR cuts. That’s because current curbs on financing rules for the property sector and the anti-pollution campaign have meant softer overall demand for credit.

Rates

The PBOC has refrained from cutting the benchmark rate or the rates for its market liquidity tools in recent years. Instead, it initiated a long-awaited revamp of the country’s interest rate framework last month, a move aimed at pushing down the cost of borrowing by households and companies without fueling bubbles in housing market.

The new reference rate, called the loan prime rate, stood at 4.25% in August in its first release, a small step lower from the previous benchmark. Some analysts expect the PBOC to cut the interest rate on medium-term lending facility this month in step with the Federal Reserve, which could in turn push the loan prime rate lower.

Tax Cuts

The government has pledged to cut taxes for businesses and households by about two trillion yuan this year in what they described as the largest-ever fiscal stimulus plan in the country. The move has had an effect -- swelling the fiscal deficit to 1.2 trillion yuan in the first seven months of 2019, according to Bloomberg calculations based on official data, compared to a shortfall of 374.5 billion yuan in the same period last year. However, the tax cuts haven’t been able to lift business investment.

Special Bonds

Local governments are allowed to sell 2.15 trillion yuan of so-called special bonds in 2019 to raise funding for infrastructure projects. The issuance has been rapid, and all the debt is to be sold by the end of September. However the money hasn’t led to a significant revival in infrastructure investment growth yet. That’s partly because a majority of the debt was used to buy land and for shanty-town renovation, according to UBS Group AG, uses which has less of a multiplier effect than spending on building railways and airports.

Yuan?

While the PBOC repeatedly said it wouldn’t use the yuan as a tool in the trade war, it has argued that the exchange rate could be a “stabilizer” in the economy as a weaker currency may help absorb some external shocks.

Markets had “looked at the yuan’s exchange rate for the next possible channel of easing amid the trade war,” as China refrained from using traditional easing tools in recent months, Tommy Xie, economist at Oversea-Chinese Banking Corp. Bank in Singapore wrote in a note.

If conventional monetary easing and fiscal stimulus steps up, expectation for using the yuan as the main hedging tool in the trade war will ease, he said.

--With assistance from Kevin Hamlin.

To contact Bloomberg News staff for this story: Yinan Zhao in Beijing at yzhao300@bloomberg.net;Miao Han in Beijing at mhan22@bloomberg.net

To contact the editors responsible for this story: Jeffrey Black at jblack25@bloomberg.net, James Mayger

©2019 Bloomberg L.P.

With assistance from Bloomberg