Good Budget News on U.S. Relief Package May Be Bad News for Economy

Congressional Budget Office said that the economic relief package passed in March would cost the government $1.8 trillion.

(Bloomberg) -- At first glance, it was good news. The Congressional Budget Office said last week that the mammoth economic relief package passed in March would cost the government $1.8 trillion, not the $2.2 trillion initially thought.

But look beneath the surface, some economists say, and the CBO’s calculations are not that comforting. Why? Because they suggest the government may not be providing the economy with all the support it might need to survive the coronavirus shock relatively intact.

“From a budget perspective, this might seem like good news, but from the larger issue of avoiding economic catastrophe it is a problem,” said former CBO Director Douglas Holtz-Eakin, who now heads the American Action Forum.

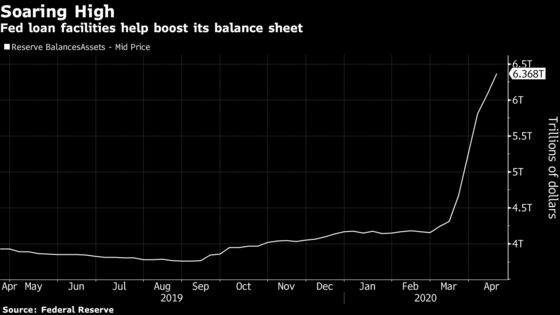

The difference between the CBO’s calculations and the early estimates comes down to a judgment about the Federal Reserve’s financing facilities for companies and state and local governments. Based partly on information from the Fed board, the CBO reckons that the loan programs backed by the relief package won’t add to the budget deficit.

Worse Shape

That may not be as good a result as it sounds. The Fed can avoid making losses on its facilities and increasing the deficit by discouraging participation by riskier borrowers. But that leaves those companies in worse shape, posing a danger to the economy as a whole.

“There’s a concern about losing money that I frankly don’t understand,” former chief White House economist Glenn Hubbard said. “The way not to lose money is to not make any loans or to lend money to people who don’t need it.”

“Those are great strategies but they don’t seem to work in a crisis,” added Hubbard, now at the Columbia Business School.

The gist of the critics’ argument is this: It’s better in an economic emergency such as this to err on the side of taking losses rather than forgo helping borrowers in dire straits through no fault of their own.

Worth the Cost

If that increases the budget deficit because not all of the loans are repaid, so be it. It’s worth the cost to try to make sure the economy comes through the crisis without incurring significant long-term damage.

The central bank is setting up the financing facilities under Section 13-3 of the Federal Reserve Act that allows it to establish emergency lending programs in “unusual and exigent circumstances.” The Fed is prohibited from taking losses on the facilities and so needs money from the Treasury Department to absorb any red ink that might occur from loans going bad.

The Fed and Treasury face a dilemma. They realize that many companies will need help to survive what will be the deepest recession since the Great Depression. But they don’t want to lend to borrowers that have scant chance of being able to repay. That would expose them to attacks that they were just wasting taxpayers’ money.

If the Fed set up a program that was likely to result in losses, “it would be seen as violating its governing law and as such would open itself up to all sorts of political criticism,” said former Fed official Roberto Perli, now a partner at Cornerstone Macro LLC.

Main Street

Congress set aside $454 billion in the CARES Act as a backstop for Fed financing facilities. The central bank has so far outlined plans to deploy some $185 billion of that, including $75 billion to absorb losses on a planned $600 billion Main Street Lending Program.

The Main Street name is a bit of a misnomer. While money is available to companies with up to 10,000 employees, the program seems pitched to middle-sized companies, not small businesses. The minimum eligible loan is $1 million.

Banks are pressing for a lower threshold.

“The minimum loan amount should be no higher than $100,000,” the Independent Community Bankers of America wrote in an April 16 letter to the Fed. “Otherwise, Main Street businesses and community banks will not participate.”

Profit Margins

As presently constituted, it’s assumed that more than 85% of the funding the facility provides will be repaid in full. Ex Fed official Joseph Gagnon suggested it could be more generous -- say 70% -- but then the Treasury would have to kick in more money.

Regardless, many medium sized companies operate on such thin profit margins that they need grants, not loans, said Gagnon, now at the Peterson Institute of International Economics. But Congress did not provide for that – unlike what it effectively did for small businesses.

The Fed has indicated it is open to altering the terms of the yet-to-be-launched program in response to feedback.

The central bank is supporting small businesses through a liquidity facility that went into operation last week. Under that facility, the Fed provides term financing to banks against loans issued under the Small Business Administration’s Paycheck Protection Program. It’s not exposed to any credit losses because the loans are guaranteed by the government.

In calculating that the government won’t lose money on Fed programs backstopped by the CARES Act, the CBO estimated that the new lending will expose the government to default and other losses, but that it will also generate interest and other income that will exceed its borrowing costs.

The budget watchdog also noted that the Fed did not lose money on its emergency lending during the 2008-09 financial crisis and in fact ending up handing over big profits to the federal government.

Holtz-Eakin said the politics are a lot different now. Back then, the government was widely criticized as bailing out banks that were responsible for the economy’s travails.

Today, “nobody caused the problem,” he said. “We’re just trying to get checks to American businesses to keep them afloat.”

©2020 Bloomberg L.P.