Goldman Sachs’s FICO Warning Is a Call to Get Smarter

Goldman Sachs’s FICO Warning Is a Call to Get Smarter

(Bloomberg Opinion) -- In the fixed-income world, nothing gets investors’ attention quite like the idea of “grade inflation.” After all, certain widely accepted, easy-to-understand scores from credit rating companies still hold huge sway over the global market for debt, even though they were partially to blame for the financial crisis.

So it’s little wonder, then, that this article from Bloomberg News’s Adam Tempkin drew a lot of interested bond traders: “Inflated Credit Scores Leave Investors in the Dark on Real Risks.” In it, analysts from Goldman Sachs Group Inc. and Moody’s Analytics argue that FICO credit scores from Fair Isaac Corp. have been artificially inflated over the past decade and don’t reflect borrowers’ true ability to pay what they owe in the event of a downturn.

“Every credit model that just relies on credit score now -- and there’s a lot of them -- is possibly understating the risk,” Goldman Sachs analyst Marty Young said in an interview. “There are a whole bunch of other variables, including the business cycle, that need to be taken into account.”

…

The concern that’s come up, Goldman and Moody’s say, is that lenders haven’t adjusted their underwriting standards as average credit scores have risen during one of the longest economic recoveries on record. So as cracks start to appear in the economy, someone whose credit score rose to 650 from 550 since the Great Recession may pay their bills more like they did 10 years earlier.

“Borrowers’ scores may have migrated up, but inherently their individual risk, and their attitude towards credit and ability to pay their bills, has stayed the same.”

This is stating the obvious and doesn’t suggest any sort of sinister grade inflation. The U.S. economic recovery that began 10 years ago has pushed the unemployment rate to about its lowest in half a century. Average hourly earnings are rising at the fastest pace since the recession ended. It follows that a number of Americans who were previously jobless now bring in a steady income and have higher credit scores. That, in turn, affords them greater access to credit.

So, what’s the problem? Cris deRitis, deputy chief economist at Moody’s, says he’s concerned about “smaller, less sophisticated firms that lend to people with poor credit histories.” He added that “car loans, retail credit cards and personal loans handed out online are the most exposed to the inflated scores.” Tempkin notes that there’s about $400 billion of that kind of debt outstanding, with a quarter of it bundled into securities that investors now hold.

I realize companies that cater to weaker borrowers can serve a vital function. Some subprime borrowers simply need a lifeline to get their finances back in order. JPMorgan Chase & Co. Chief Executive Officer Jamie Dimon even said in congressional testimony this week that when it comes to mortgages, loosening constraints on lending to people with low incomes or prior defaults could single-handedly boost U.S. economic growth by 0.2 percent.

Still, forgive me for not shedding a tear for firms that don’t look beyond FICO scores, or for investors who snapped up high-yielding asset-backed securities.

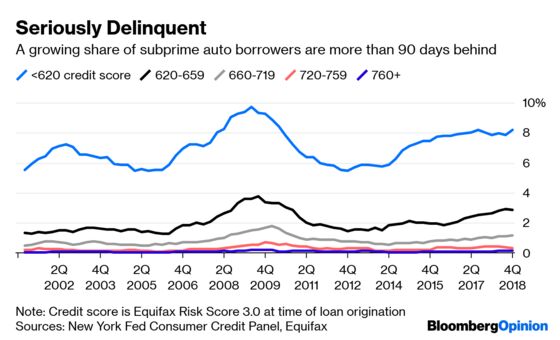

In February, I looked at subprime auto loans and concluded that they’re far from a systemic risk, even though more more than 7 million Americans were at least three months behind on their car payments, the most ever. The most at-risk lenders include names like Global Lending Services, GO Financial and Skopos Financial. As I said then: “If the worst-case scenario is that some private-equity backed new entrants to the auto-loan business close shop, and investors who were reaching for yield get burned, that doesn’t seem so bad.”

The hand-wringing over FICO scores feels very much the same. Goldman attributes the growing number of delinquent auto loans to the general increase in credit scores. But again, it comes back to who’s doing the lending. Large banks certainly use more than just FICO scores to determine whom they choose to underwrite and at what terms. There’s a reason for that, and it probably has precisely to do with scores looking rosy during good economic times.

It’s not even as if FICO pretends to be a perfect reflection of a borrower’s creditworthiness. From Tempkin’s piece:

“The relationship between FICO score and delinquency levels can and does shift over time,” said Ethan Dornhelm, vice president of scores and predictive analytics at FICO. “We recognize there’s a lot more context you can obtain beyond a consumer’s credit file. We do not think that score inflation is the issue, but the risk layering on underwriting factors outside of credit scores, such as DTI, loan terms, and even trends in macroeconomic cycles, for example.”

It’s not hard to come up with ways to alleviate concerns about elevated FICO scores. Lenders can require a broader range of information before extending credit, or they can simply bump up their FICO thresholds to account for the prolonged business cycle. The same goes for investors in asset-backed securities. They could easily just be more selective in what they purchase. But with the Federal Reserve no longer raising interest rates and the reach for yield back in style, that doesn’t seem likely. If the bundles of loans turn bad, they’ll have no one to blame but themselves.

It’s tempting to look for signs of stress now that the U.S. economy is on the verge of the longest expansion in history. And it’s true that private-label credit cards and online loans are seeing an uptick in missed payments. But just as the inverted yield curve served as a reminder that all business cycles must end (though not necessarily imminently), these delinquent payments are simply a call for lenders and investors to get smarter.

To contact the editor responsible for this story: Daniel Niemi at dniemi1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Brian Chappatta is a Bloomberg Opinion columnist covering debt markets. He previously covered bonds for Bloomberg News. He is also a CFA charterholder.

©2019 Bloomberg L.P.