Goldman, Pimco Detect Irrational Inflation Mania in Bonds

Goldman, Pimco Detect Irrational Inflation Mania in Bond Market

(Bloomberg) -- Goldman Sachs Group Inc. and bond titan Pacific Investment Management Co. have a simple message for Treasuries traders fretting over inflation: Relax.

The firms estimate that bond traders who are pricing in annual inflation approaching 3% over the next handful of years are overstating the pressures bubbling up as the U.S. economy rebounds from the pandemic.

Add to that certain technical distortions in the way market-based inflation expectations are priced, and Goldman Sachs, for one, says the overshoot could be as large as 0.2-to-0.3 percentage point. That gap makes a difference with key market proxies of inflation expectations for the coming few years surging this week to the highest in more than a decade. The 10-year measure, perhaps the most closely followed, eclipsed 2.5% Friday for the first time since 2013, even after unexpectedly weak U.S. jobs data.

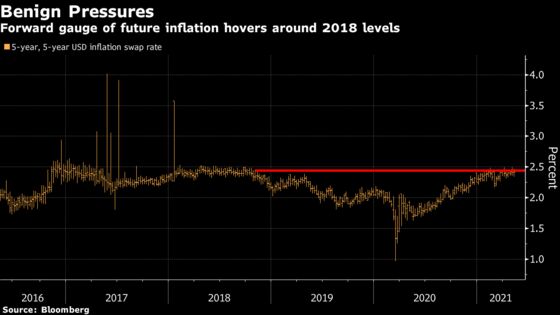

There’s at least one market metric that backs up the view that the pressures, which have been building for months, aren’t about to get out of hand and may even prove temporary. A swaps instrument that reflects the annual inflation rate for the second half of the next decade has been relatively stable in recent months.

The debate over inflation is crucial as policy makers and investors navigate the recovery from the pandemic. The Federal Reserve has been hammering home that it sees any spike in price pressures as likely short-lived, and that it’s willing to let inflation run above target for a period as the economy revives.

Now it appears to be catching a break with its campaign. Not only are the likes of Goldman and Pimco laying out the case for a more benign inflation outlook, but traders in recent weeks have also trimmed bets on rate hikes by the end of 2023.

“We do not see the sort of inflationary pressures that markets appear to be fearing, and high growth rates will not necessarily translate into a higher inflation rate,” said Praveen Korapaty, Goldman’s chief interest-rate strategist.

Market measures known as breakeven rates, which are derived in part from Treasury Inflation-Protected Securities and represent expectations for annual increases in consumer prices, surged anew this week as the reopening of major industrial economies progressed.

Commodities Link

Inflation worries have been mounting against a backdrop of soaring commodities prices -- copper, for example, set a record high Friday. It’s all happening as lawmakers in Washington debate another massive fiscal-stimulus package.

But it’s worth noting that two-year breakevens -- which reached an almost 13-year high close to 2.9% on Wednesday -- are firmly above where traders see inflation expectations in the second half of the coming decade. That shows the market is positioned for price pressures to eventually ebb.

Korapaty calls the outlook for inflation “benign.” His view is that the market is overly optimistic with its inflation assumptions, with the greatest mismatch to be found on the three- and five-year horizon. At roughly 2.75% and 2.7%, respectively, those rates are around 20 to 30 basis points higher than they should be, in his estimate.

“If we are right and inflation readings come off, we might be tempted to fade Fed pricing and take the view that markets can push back when pricing Fed liftoff,” Korapaty said. In addition, he says, that would be the right time to sell three-year breakevens.

New Approach

The discussions around price pressures come amid unease in markets and in Washington over the extent of fiscal stimulus. On Tuesday, Treasury Secretary Janet Yellen stirred markets by saying interest rates will likely rise as government spending swells and the economy achieves faster growth. She walked back the remarks hours later.

The Fed has signaled that it intends to keep policy ultra-loose at least through 2023. In August, it adopted a new approach that lets inflation run above 2% for longer before raising rates. The goal is to get inflation to average 2% over time, to make up for previous shortfalls. The Fed has failed to achieve that level on a consistent basis for much of the past decade.

Futures are now pricing in Fed liftoff around the end of the first quarter of 2023, earlier than officials project. Traders have also reduced wagers on additional hikes by the end of that year. They see a total of 65 basis points of tightening by the end of 2023, down about a quarter-point since April 1.

Granted, some on Wall Street are more concerned about inflation risks. JPMorgan Chase & Co. chief global markets strategist Marko Kolanovic is warning that some money managers face an “inflation shock” to their portfolios.

TIPS Caveats

Breakevens have long carried the caveat that they can’t be taken at face value because of the illiquidity of TIPS and the risk premium that investors demand due to uncertainty over the path of inflation -- both of which lead to higher rates than would otherwise be the case.

Fed officials have developed models to account for those variables, and Pimco has followed up with its own. Its conclusion, in a nutshell, is that inflation expectations are even further below the Fed 2% target than officials assume. That means traders may need to pull back on expectations for Fed liftoff from near zero.

“We basically argued that inflation expectations are a little below where the Fed sees them” after coming in at around 1.75% as of March, the most recent reading in Pimco’s model, said Tiffany Wilding, an economist.

Moreover, she sees the recent rise in five-year, five-year forward breakevens, which strip out short-term noise like fluctuations in oil prices, as partly due to uncertainty around the inflation outlook -- as opposed to just an acceleration of expectations.

“Because we think front-end rates are pricing in a more aggressive Fed path than we believe, we do like shorter-dated nominal bonds, and think there’s value there,” she said.

©2021 Bloomberg L.P.