Goldilocks Year Awaits Emerging Markets Defying Pandemic Rout

Here are three reasons to be optimistic about the outlook for emerging currencies in 2021.

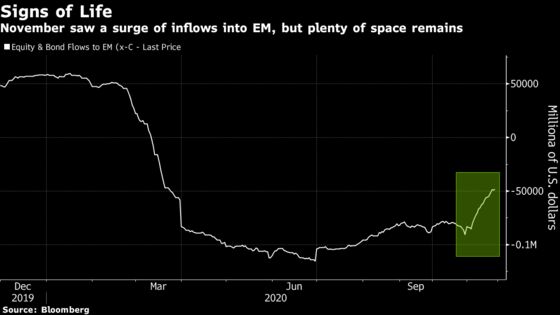

(Bloomberg) -- Emerging-market investors seem to have everything going for them right now, with the November rally offering a hint of what 2021 may have in store.

A plethora of tailwinds from accommodative central banks to an impending change of U.S. president and Covid-19 vaccine progress has put the assets of developing nations on course for some impressive milestones. Bonds have wiped out their year-to-date losses, while MSCI Inc.’s currency index is poised for the best month since January 2019 as well as a second successive annual gain. The MSCI stocks gauge is on track for its best month since March 2016.

Underpinning the recovery is a resurgence in foreign-investor interest. Fourth-quarter portfolio inflows to emerging markets are poised to hit the highest in eight years, data from the Institute of International Finance show. Yet, for all the euphoria, foreign positioning in bonds and equities for developing nations excluding China remains light, and Deutsche Bank AG’s Sameer Goel, says the rally is far from over.

“It’s Goldilocks for emerging markets’ under-invested assets as we go into 2021,” said Goel, the bank’s head of emerging markets macro research in Singapore. They “have considerable cyclical catch-up potential.”

Deutsche Bank isn’t alone in seeing further gains. Goldman Sachs Group Inc. and JPMorgan Chase & Co. have made bullish calls on the asset class in recent weeks. UBS Group AG said last week emerging-market assets may benefit from the prospect of “near-complete normalization” in global economic mobility by the end of next year.

Read More: Alternative Data Show Advanced Economies Sliding While EMs Keep Gains

Mobility is key to the recovery, which is why the possibility of a spike in Covid cases remains a risk as average temperatures drop in many of the developed economies and people socialize over end-of-year holidays. Moves by some central banks including those in Taiwan, South Korea and Thailand to become more assertive in stemming currency strength might also limit gains. The behavior of China’s central bank will also be watched for any signs of resistance to the yuan’s strength.

Below are three reasons to be optimistic about the outlook for emerging currencies in 2021 and key events and data to watch out for in the coming week:

Attractive Valuation

Exchange rates in developing economies are still modestly undervalued, with an average Z-score of minus 0.4 using a simple metric of the current REER versus the five-year average. Countries such as Brazil, Turkey, Russia, Hungary and Malaysia have even lower scores, with readings of minus 1.4 or below.

History suggests that there’s scope for improvement. The average valuation Z-score hit positive 0.9 in April 2010 following the Global Financial Crisis in 2008. It also reached plus 0.7 in April 2013 following the implementation of the third round of quantitative easing by the Federal Reserve. Conditions in both periods were similar to those prevailing this year, with historically low U.S. real rates and improving global manufacturing activity.

Real Yield Advantage

An abundance of caution from the Fed -- which under average inflation targeting, has pledged to allow inflation to run at above 2% -- implies that real yields will fall further.

Read more: In Praise of Inflation, Or What Risk Assets Need: Macro View

With the stock of the world’s negative-yielding debt exceeding $17 trillion, the hunt for yield favors emerging markets. Juxtaposed against already low U.S. real yields, the 10-year real yields of developing economies -- based on Bloomberg consensus economists’ forecasts –- enjoy a Z-score of positive 0.8 versus the three-year average. The highest scores are for China and South Africa, which both have plus 2.0 readings.

Investor Demand

Trailing 12-month foreign flows into emerging-market bonds have an average Z-score of negative 0.7 versus the five-year average. For equities, the figure stands at negative 1.3. Considering the light positioning in the debt universe, Indonesia’s rupiah and the Mexican peso are well placed to benefit, while currencies of South Korea, Taiwan, Thailand, Malaysia and Turkey stand to win based on data for stocks.

To see the Z-Scores tabulated for all emerging markets, click here.

Listen to the EM Weekly Podcast: China PMI, Unexpected Liquidity; Inflation

India Decides

- The Reserve Bank of India is expected to leave its key rate unchanged on Friday as inflation has been running above target for seven consecutive months

- The RBI may also raise its near-term inflation forecast given the upside surprise since its October review, according to Bloomberg Economics

- Governor Shaktikanta Das also said last week that the economic recovery had been more rapid than expected, and accordingly, the RBI is expected to raise its GDP forecast for fiscal 2021

- The RBI has cut interest rates by “a great deal” and more policy space can be created when inflation eases, its executive director and interest rate-panel member Mridul Saggar said

- READ: India Enters Recession as Virus Pummels No. 3 Asian Economy

- The rupee closed 0.2% weaker last Friday after data showed India entered an unprecedented recession

- The Bank of Thailand’s minutes on Wednesday may contain more information about plans for halting the appreciation of the baht

- The Thai currency was the the third-worst performing currency in emerging Asia after the yuan and the Taiwan dollar last week as the chorus of pressure aimed at the central bank to slow appreciation continued

China PMI, Korea Restrictions

- China’s manufacturing purchasing managers’ index rose to 52.1 in November from 51.4 in the previous month, according to official data released Monday. That was the highest since September 2017 and beat the 51.5 median estimate in a Bloomberg survey of economists

- The yuan’s outperformance has partly been because of the recovery in the domestic economy

- Markit manufacturing PMIs are due on Tuesday for the rest of Asia, with China’s Caixin indicators on Thursday

- These diffusion indicators have shown a steady improvement over the past four months

- South Korea’s October industrial production data, which showed a a larger-than-expected drop from the previous year, kicked off a busy week of economic reports, including a third-quarter gross domestic product reading on Tuesday and current-account data on Friday

- South Korea will maintain social-distancing rules in the greater Seoul area at the current level while adding restrictions to more venues, and tighten measures outside the capital region

- The won was Asia’s top-performing currency last week, in line with its economic performance and external accounts, despite continued concerns about the impact of currency strength

- READ: Here Are the Low-Yield Asia FX to Watch for Returns: Macro View

- Malaysia’s October trade balance showed another surplus in data that was released last Friday, ahead of the original release date this Monday

- The ringgit is little changed after being the second-strongest currency in Asia last week as commodity prices extended gains and the government passed the budget

- Thailand’s current account and trade balance for October remained in surplus, according to data released on Monday

- The constitutional court is due to rule on Prime Minister Prayuth Chan-Ocha’s qualification to serve on Wednesday -- after allegations of abuse of power resulting from his residence in army accommodation, despite no longer being a serving officer

- There’s a slew of inflation figures due in Asia, including those from Indonesia, South Korea, the Philippines and Thailand

Eastern Europe Rates

- Poland’s central bank will probably leave its policy rate unchanged near zero for a sixth consecutive meeting as the eastern European country tightens measures to combat the spread of the coronavirus

- Policy makers in Hungary will announce their decision on Thursday after leaving the key rate unchanged at 0.75% at the previous nine meetings

Polish GDP, Turkey CPI

- Poland reported final third-quarter GDP on Monday, which showed a 1.5% contraction from the previous year; data will be followed by November PMI and CPI prints on Tuesday

- South Africa posted a sixth straight monthly trade surplus in October and M3 money supply growth accelerated, according to data released on Monday

- Reports on manufacturing, vehicle sales and business confidence will give clues about the strength of the recovery from the coronavirus lockdown

- Russia’s consumer inflation probably accelerated in November to a seven-month high, a report may show on Friday, complicating the central bank’s policy options for the remainder of the year

- The manufacturing and services PMIs, gold and forex reserves, and money supply are also due this week

- Turkey’s consumer inflation rate probably rose to 12.7% in November, the highest in more than a year, data may show Thursday. A report on Monday showed the economy rebounded in the third quarter, posting growth of 6.7% from the same quarter last week, compared with a 4.8% estimate

Brazil Spending Reforms

- Investors will have their eyes on the Brazilian Congress this week to see if debates on fiscal spending reforms and the 2021 budget will resume. Third-quarter GDP data on Thursday are expected to show signs of a recovery, according to economists surveyed by Bloomberg. Industrial production numbers on Wednesday will give a glimpse into fourth-quarter output

- Chile’s economic activity is expected to have rebounded in October, data due on Tuesday may show

- Retail sales surged by the most in a decade and copper production fell slightly in October, according to data published on Monday

- Minutes from the November meeting of Colombia’s central bank due later today are likely to show policy makers will not provide additional monetary policy relief in the near future and will opt to wait for more information. PMI data and the third-quarter current account balance will be reported on Tuesday

NOTE: Simon Flint is an emerging-market strategist at Bloomberg News. The observations he makes are his own and not intended as investment advice.

©2020 Bloomberg L.P.