Global Tax Talks Race Against Clock as Holdouts Climb Down

Global Tax Talks Race Against Clock as Holdouts Fall Into Line

(Bloomberg) --

Global talks to reshape the corporate tax landscape are resuming on Friday with some holdouts to the international consensus on a minimum rate falling into line to back an agreement that still hangs in the balance.

In a series of climbdowns, Ireland, Estonia and Hungary announced that they would sign up to the deal, providing a boost to talks between 140 countries hosted by the Organization for Economic Cooperation over a wide-ranging accord on the treatment of multinationals.

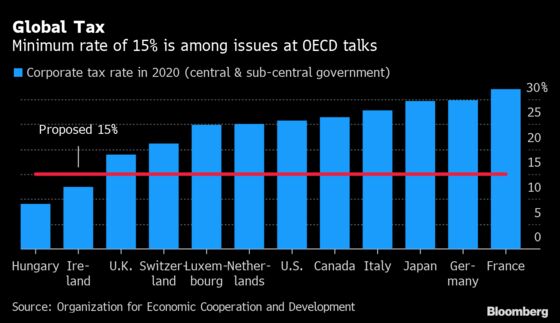

Among ongoing disagreements, some nations are seeking so called carve-outs to partially exempt certain activities from a minimum tax rate of 15%, while others are haggling over separate terms concerning where profits of big firms are levied.

“We’re on the precipice of an historic tax agreement that signals a new era of multilateralism,” Treasury Secretary Janet Yellen said Friday during the virtual B20 Summit. “The international tax agreement will stop the four-decade long race to the bottom on corporate tax.”

The talks are the culmination of years of negotiation that took on new vigor with the advent of President Joe Biden’s administration. The U.S. views Ireland’s move as enormous progress, a Treasury official said, noting that 15% would be a floor, not a ceiling, for company taxes around the world.

While OECD chief Mathias Cormann said this week that he’s optimistic of a deal coming together in time for a Group of 20 summit later this month, French Finance Minister Bruno Le Maire also warned that “it is now or never.” The concern is that a historic window of opportunity may close as chances of U.S. Congressional approval quickly fade thereafter.

“The alternative to this happening is that we see the growth of unilateral tax measures, we see the slow erosion of our global tax architecture,” Irish Finance Minister Paschal Donohoe told Bloomberg Television. “All of those things would bring additional risks, additional instability.”

In another move on the eve of the Friday meeting, Estonia joined Ireland in dropping its opposition to the agreement, determining that the minimum tax will have little impact on local entrepreneurs there.

On Friday, Hungarian Finance Minister Mihaly Varga said the country had managed to win concessions that open the way for it too to back a compromise deal. They include a 10-year transition until the minimum tax takes effect, and the possibility for companies to partially deduct some costs such as payroll.

For the Irish, the floor was a major sticking point. The new minimum rate is 2.5 percentage points higher than the level that has been a pillar of its economic model for a generation, underscoring its significance for a country whose prosperity is linked to its attractiveness for multinationals seeking an operating base in the European Union.

“I believe Ireland entering into the agreement at this point gives the process further momentum at a very, very critical juncture,” said Donohoe.

‘At Least 15%’

While the financial implications may never be realized if the deal isn’t finalized, the importance of the existing 12.5% rate in the Irish consciousness was the reason a government normally aligned with international consensus held out for so long.

Ireland took particular exception to wording in a July draft of the accord that called for a minimum rate of “at least 15%,” a proposal which it didn’t accept due to concerns that the final number could end up significantly higher. The “at least” language has been dropped from the revised draft.

Ireland’s 12.5% rate, which it has held onto since 2003, is well below the average of about 23% throughout the OECD. That’s helped persuade international companies such as Alphabet Inc.’s Google and Facebook Inc. to use it as a base for their European headquarters.

Ireland’s finance ministry estimates it will lose up to 2 billion euros ($2.3 billion) in corporation tax as a result of reforms.

©2021 Bloomberg L.P.