Global Funds See More Pain for India Debt

Modi’s record $100 billion borrowing plan isn’t the only piece of bad news for India’s bond market.

(Bloomberg) -- Prime Minister Narendra Modi’s record $100 billion borrowing plan isn’t the only piece of bad news for India’s bond market, some money managers say.

Debt sales could still fail to bridge a forecast deficit as the government’s budget relies on ambitious revenue collections and one-off items that may not materialize, according to OppenheimerFunds Inc. And Europe’s largest asset manager, Amundi SA, says bonds of other Asian nations offer better value.

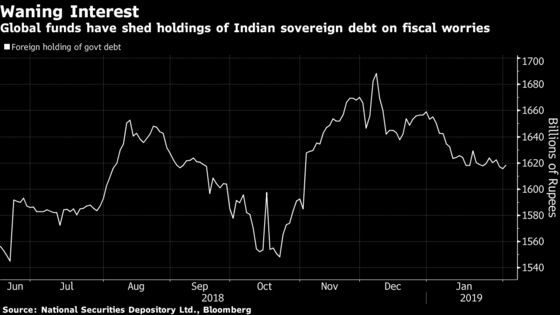

Modi on Friday handed out $13 billion of measures including payouts for farmers and relief for taxpayers to boost support before elections, moves that will end up widening deficits. That’s bad news for the market that has slumped in five of the past six weeks as foreigners sold 43.6 billion rupees of sovereign debt in January, after paring holdings by 179 billion rupees in 2018.

“I suspect the slippage in reality would be far worse,” said Krishna Memani, head of fixed income at OppenheimerFunds. “It is an election budget and the government has concluded that higher rates is a cost it is willing to bear.”

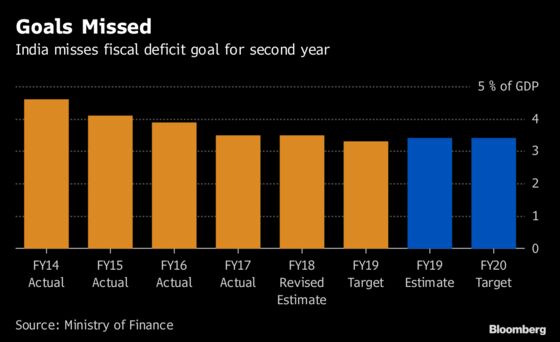

The yield on the most-traded 2028 bonds surged 13 basis points on Friday -- the most since May -- after the budget documents showed widening in the deficit targets for this fiscal year and the next to 3.4 percent of gross domestic product. The government had earlier targeted 3.3 percent for this year and 3.1 percent for 2019-2020.

“I will observe closely the developments in the next few months on the budget side before I consider increasing Indian local bonds,” said Esther Law, senior investment manager for emerging market debt at Amundi. There’s more value in other Asian markets with better fundamentals and valuations relative to rupee bonds, she said.

The yield on the 2028 bond slid four basis points to 7.63 percent as of 1:22 p.m. on Tuesday.

Next trigger for bonds will come from the central bank’s policy decision on Thursday, when it is expected to change its stance to neutral while keeping rates on hold. A dovish signal will help the market take a bit of fiscal slippage in its stride, according to BNP Paribas Asset Management.

“Given a dovish central bank and only slightly deteriorating fiscal situation, we expect a slightly negative impact on yields initially,” said Jean-Charles Sambor, deputy head of emerging-market debt at BNP. “Longer term, we think that the bad news is priced in.”

While global funds were net buyers of government debt on budget day, fiscal slippage and political uncertainty mean Indian bonds will compete with other developing markets that have lower economic and political risks, OppenheimerFunds’ Memani said. Foreigners sold 13.5 billion rupees of sovereign debt on Monday, the most since Dec. 12.

“If the Indian government is looking to foreign investors to finance its deficit, there is nothing in the budget that gets them more comfortable,” he said.

To contact the reporters on this story: Subhadip Sircar in Mumbai at ssircar3@bloomberg.net;Kartik Goyal in Mumbai at kgoyal@bloomberg.net

To contact the editors responsible for this story: Tan Hwee Ann at hatan@bloomberg.net, Ravil Shirodkar, Robert Brand

©2019 Bloomberg L.P.