It’s the (World) Economy, Stupid!

(Bloomberg Opinion) -- For all that central banks are leaning dovish these days, very few see problems of their own making.

Weaker economic outlooks have been chalked up to global headwinds, crosscurrents abroad and other euphemisms that generally mean China and Europe. Sometimes both are called out directly.

Low inflation is certainly aiding the tilt toward easing, but isn’t the cause of it. In recent years, the pace of price increases has been below target more often than above it for many central banks. So why seize this moment? The deceleration of global activity requires a global response.

While the idea of a single central bank for the world is a stretch, it’s close to existing in all but name. The global shift in monetary-policy stances since the Federal Reserve changed its tune late last month has been swift. And policy makers are eager to look to the state of the world economy, rather than their own backyards.

Don't let the “nothing-to-see-here-folks” line obscure that, with very few exceptions, tides have shifted. Sure, global factors have always played a role. They certainly did in 2007-2009. Yet what we see today isn’t even close to that crisis. (If there is an echo of history here, it may be the 2015-2016 period.)

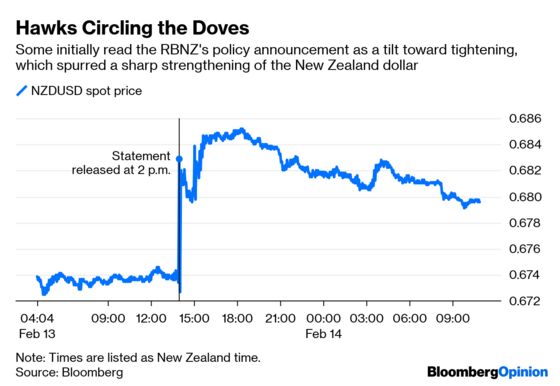

The Reserve Bank of New Zealand's interest-rate decision last week and Governor Adrian Orr's press conference is a case in point. The local economy is peachy, at or near full capacity, so the argument went. The biggest concerns are China and the softening Australian economy. Orr says the RBNZ is in “watch, worry and wait” mode.

Notwithstanding local vim, the Reserve Bank did move in a dovish direction. Don't believe some market commentary claiming the bank was “hawkish.” Projections of a hike were pushed back and the next move could be up or down. After all, there’s no point in worrying without adjusting your risk-management setup.

The RBNZ's decision also stands out because, if an observer relied on market commentary, it wasn’t necessarily clear through the course of the day whether the bank was dovish, hawkish or just insufficiently dovish. There is a lesson here for the plethora of central bank speeches, testimonies and minutes this week. Focus on the commonalities, not on the differences.

What differences there are will be mostly of degree, not kind. (I will set the Bank of England aside on this one. The BOE is unique in that it’s grappling with the Brexit fiasco as well as international economic currents.)

As Roberto Perli of Cornerstone Macro notes, central banks may have been late to the scene, but they are nevertheless on the case. True, some may not actually cut rates this year, such as the Federal Reserve or the European Central Bank. They nevertheless have abandoned or scaled back tightening ambitions. “Better late than never,” Perli, a former Fed official, wrote last week.

The real action is likely to be in emerging markets, including more loosening from China itself. That would be “prudent,” to use the People's Bank of China's words. Beijing has cut taxes and lender reserve requirements. My Bloomberg Opinion colleague Anjani Trivedi described here why a fully blown rate cut is unlikely to do much to jump-start the world’s second-biggest economy. Meanwhile, India gets points for leaning in and cutting as the Reserve Bank of India jettisoned its tightening bias. The two Asian economies often depicted as being the future of the economic world have shown leadership.

How many can follow their lead? When looking at the plethora of monetary communications this week, focus on the direction. Don't let details detract from the big picture.

To contact the editor responsible for this story: Rachel Rosenthal at rrosenthal21@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Daniel Moss is a Bloomberg Opinion columnist covering Asian economies. Previously he was executive editor of Bloomberg News for global economics, and has led teams in Asia, Europe and North America.

©2019 Bloomberg L.P.