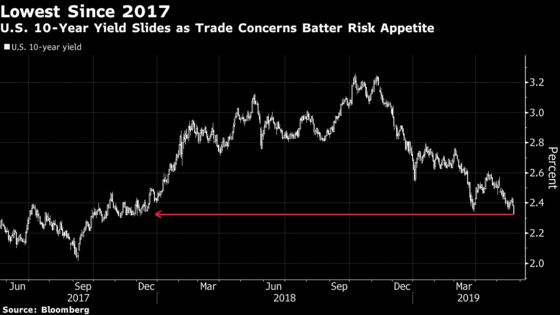

Global Bond Rally Drives Treasury Yields to Lowest Since 2017

The rally wipes out the impact of U.S. policy makers’ five rate hikes since benchmark 10-year yields were last this low

(Bloomberg) -- The U.S.-China trade conflict and cracks in the global economy are herding investors to the safest parts of financial markets, pushing yields to multiyear lows and strengthening bets that the Federal Reserve will cut interest rates in 2019.

Disappointing U.S. economic data helped drive the 10-year Treasury yield down to 2.29% on Thursday, the lowest since 2017. Futures trading gathered pace amid mortgage-related hedging. The yield on the long bond also fell to the lowest since 2017, at 2.73%. Inflation expectations tumbled yet again, and the Bloomberg Dollar Spot Index surged to its highest level this year before retreating.

The rally effectively wipes out the impact of U.S. policy makers’ five rate hikes since benchmark 10-year yields were last this low. It comes as traders are pricing in more than 30 basis points of Fed cuts by year-end, with options activity suggesting some hedging against a half-point easing as officials’ next move. The tariff standoff between the world’s two largest economies has sharpened the focus on signs of faltering growth, which were apparent Thursday in the U.S. and Europe.

“If investors’ worst fears are realized and there is a sharp longer-term ramp-up in the trade war, you could see yields fall further,” said Jon Hill, rates strategist at BMO Capital. “There’s a very bond bullish backdrop.”

Ten- and 30-year yields breached their prior 2019 lows from March, when mortgage-related hedging in the swaps market was also magnifying the move. This activity in swaps may be at work again, though traders suspected investors were better prepared for this drop in yields given the darkening global outlook.

Read here for technical analysis of where yields may go now

Also feeding the haven buying: Political tensions are elevated in the U.K., with the risk of a disorderly Brexit back on the radar.

German 10-year yields dropped three basis points to minus 0.12%, while those on their U.K. peers dropped below 1% for the first time in seven weeks.

“There’s no single smoking gun, but gilts are rallying because of political risks, bunds are doing OK because Germany PMI data were still bad, and equities are suffering as U.S.-China trade-war fears gradually intensify,” said John Davies, an interest-rate strategist at Standard Chartered Plc.

Bonds in Japan, Australia and New Zealand rallied Friday, with the Aussie 10-year yield slipping as much as 5 basis points to a record 1.53%, near the central bank’s policy rate of 1.5%. The yield on similar-maturity kiwi notes slid 3 basis points to 1.73%, while Japan’s benchmark yield fell half-a-basis-point to minus 0.07%, the lowest since April 2. The 10-year Treasury yield rose one basis point to 2.33% in Asian trading.

Thursday’s “decline in Treasury yields seems overdone,” said Masahiko Loo, a portfolio manager of fixed income at AllianceBernstein Japan Ltd. “However, if the trade war causes a sharp decline in share prices, that could push yields lower.”

And if the global backdrop is weighing on growth, it’s crushing inflation expectations.

Thursday brought a further leg down in already-depressed market measures of the path of consumer prices. Breakeven rates -- which are derived from the difference between yields on inflation-linked debt and regular Treasuries -- tipped lower, leaving the five-year down about 10 basis points this week to 1.62%.

--With assistance from Alexandra Harris, Edward Bolingbroke and Chikafumi Hodo.

To contact the reporters on this story: Emily Barrett in New York at ebarrett25@bloomberg.net;John Ainger in London at jainger@bloomberg.net

To contact the editors responsible for this story: Ven Ram at vram1@bloomberg.net, Mark Tannenbaum

©2019 Bloomberg L.P.