(Bloomberg Opinion) -- China’s bond market has been eerily quiet lately.

Over the past year, investors in China’s U.S. dollar bonds had gotten used to the idea of defaults. As early as 2015, the government started allowing some state-owned enterprises to renege on their commitments, a painful but welcome step that helps differentiate healthy firms and troubled ones.

But there hadn’t been a single case since China Minsheng Investment Group Corp. triggered a cross-default in April. Until Friday, that is – when the Shanghai-based company said it wouldn’t be able to repay a $500 million bond due Aug. 2.

You could argue this is an idiosyncratic case. The five-year-old conglomerate’s stunning rise relied on the false impression of political backing, so it makes sense that its fall would be just as spectacular. More likely, however, is that China Minsheng is the tip of the iceberg. Buckle up: More defaults are on the way.

That’s because liquidity is tightening again. Buoyed by what Beijing had perceived as progress in trade talks with the U.S., officials in April started turning back to President Xi Jinping’s campaign to wring excess borrowing from the financial system.

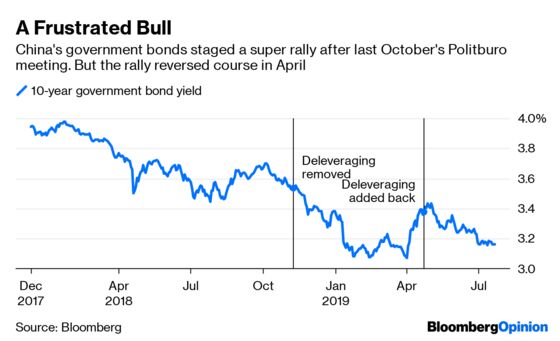

Just look at the Politburo’s language from its latest quarterly meeting. In a Communist Party statement, key phrases such as “deleveraging” started to reappear, as well as Xi’s exhortation that “apartments are for living in, not for speculation.” That’s quite a turnaround from October, when officials removed all references to corporate debt or property curbs as the trade war escalated.

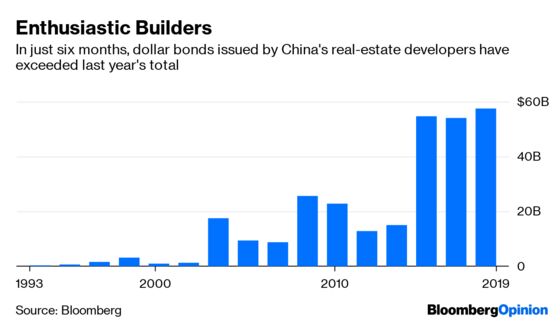

As Bloomberg Intelligence analysts Kristy Hung and Patrick Wong meticulously chronicled, property deleveraging is also back in full swing, with regulators choking off all funding channels. China Evergrande Group, the most avid offshore issuer, postponed dividend payouts last week to preserve cash. Issuing dollar bonds had become an important channel for developers, accounting for roughly a quarter of non-bank financing last year.

Funding is getting tight for other junk-rated developers, too. In July, Tahoe Group Co. issued a three-year bond with a 15% coupon, doubling the interest payment it offered as recently as January 2018.

To make matters worse, low-quality borrowers in the offshore market are finding that few investors want to lend over longer horizons, which has triggered a surge of issuance in short-dated bonds. Last year, 78% of new issues had maturities of one to three years, up from less than half in 2017. This will only make default scares more common: After all, honoring interest payments is a lot easier than paying off principal, or rolling over debt.

With trade talks now stalled, and the Federal Reserve all but certain to cut rates at the end of the month, there’s hope that the People’s Bank of China will start easing, too. Domestic bond traders, however, aren’t convinced, even as top bureaucrats convene to discuss China’s economic priorities. The 10-year sovereign yield spread over U.S. Treasuries widened to 110 basis points from 26 basis points in November.

The word default, itself, isn’t so scary. After all, evaluating credit risk is a bond investor’s job. What’s really scary in China, as I’ve written, is the prospect that very little can be clawed back. A 15% coupon payment isn’t so alluring if you can’t recover the principal.

To contact the editor responsible for this story: Rachel Rosenthal at rrosenthal21@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Shuli Ren is a Bloomberg Opinion columnist covering Asian markets. She previously wrote on markets for Barron's, following a career as an investment banker, and is a CFA charterholder.

©2019 Bloomberg L.P.