German Gloom Weakens Rate-Hike Case for Surprise Czech Hawk Mora

German Gloom Weakens Rate-Hike Case for Surprise Czech Hawk Mora

(Bloomberg) --

One of two central bankers who voted to raise interest rates in the Czech Republic just last month signaled he may be ready to change his mind. The koruna weakened against the euro.

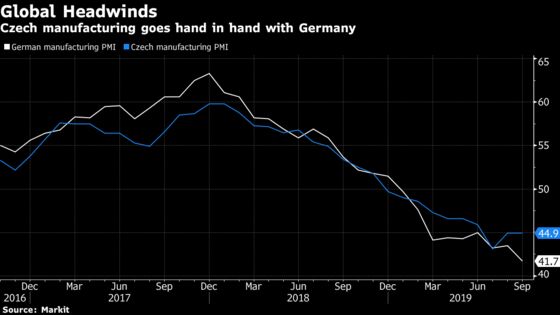

With Germany flirting with recession next door, the export-dependent Czech economy is facing headwinds, undermining arguments to increase borrowing costs, according to Vice Governor Marek Mora. His shift may mean no more monetary tightening, for now, at what’s been one of Europe’s few hawkish central banks.

“With the information I have now, the probability that I will vote for a hike again next month is lower than in September,” Mora, 48, said. “I can’t rule it out, but my arguments for a hike have weakened.”

Since Mora and a colleague unsuccessfully voted to raise the benchmark by a quarter point to 2.25% in September, inflation has slowed, falling back from the top of the bank’s tolerance band. Now he and his colleagues are more likely to keep a wait-and-see attitude when they meet on Nov. 7, he said.

The comments add to diverging views from policy makers this month on how they should tackle persistent domestic price pressures even as the global economic slowdown is compounded by risks including Brexit and trade wars.

The koruna snapped six days of gains after Mora’s comments, weakening 0.3% to 25.647 per euro. The Czech currency has averaged 25.74 this month, more than 2% weaker than the central bank’s forecast for the quarter and underperforming its regional peers, the Polish zloty and Hungarian forint, this month.

‘Very Balanced’

Governor Jiri Rusnok assessed the Sept. 25 debate as “very balanced” between staying put and hiking, and said the Czech National Bank would debate potential tightening again at the next meeting.

Mora, who has usually supported caution on rate hikes, broke with that stance last month because the economy showed resilience to the slowdown in Germany and he wanted to correct what he saw as “completely wrong” market expectations of rate cuts, he said. While investors have since placed some wagers on potential tightening in the next six months, the money market is still pricing in rate cuts later in 2020.

“I wanted people to understand the complexity of our situation and that none of us was certainly thinking about any rate cuts,” Mora said. “I wanted to emphasize that some likelihood of a hike was still there. I wanted to send a signal that I really am targeting 2% inflation and that I don’t want to be stuck near the top of the range or even risk breaching the upper boundary.”

But after inflation slowed to 2.7% in September, the risk that it would break out of the 1% to 3% tolerance band has declined, Mora said. Germany, the biggest buyer of Czech exports, has also shown further signs of weakness.

The board will be armed with fresh staff forecasts on Nov. 7, after twice choosing to disregard the rate hike implied in the August projections.

“If I look around the whole board and at the macroeconomic development, I see rate stability as the most likely outcome,” Mora said. “With such extreme and hard-to-quantify levels of global political uncertainty, the rule of thumb is to simply do nothing.”

To contact the reporters on this story: Krystof Chamonikolas in Prague at kchamonikola@bloomberg.net;Lenka Ponikelska in Prague at lponikelska1@bloomberg.net

To contact the editors responsible for this story: Blaise Robinson at brobinson58@bloomberg.net, Michael Winfrey, Peter Laca

©2019 Bloomberg L.P.