(Bloomberg Opinion) --

A General Electric Co. earnings release is never a straightforward event; Wednesday’s felt particularly inconclusive. Turnarounds are prone to fits and starts, and at GE, it’s apt to be a particularly long and difficult road. There was little in the latest quarter’s results to convert doubters of CEO Larry Culp’s recovery efforts into believers, and, similarly, nothing concretely terrible enough to shake supporters out of their faith. On the positive side, there were signs of stabilization in the struggling power division. The unit posted operating profit of $117 million in the quarter, down significantly from a year earlier but hey, it wasn’t a loss. Orders were up 28% on an organic basis in the gas turbine side of the business. Also, GE raised its adjusted industrial cash flow guidance and now sees the potential to actually generate as much as $1 billion for the full year. That compares with a previous call for cash flow to be at best breakeven in 2019.

It’s not really clear how we got to that raised guidance, though. GE says the improved outlook reflects better-than-expected first-half results for power and health care, and lower restructuring expenses and interest costs. It now says cash flow for the power business could be flat relative to last year’s $2.3 billion burn (adjusted for the reallocation of the grid operations to the renewable energy division), versus an earlier forecast for a substantial year-over-year weakening. Gordon Haskett analyst John Inch estimates a $500 million boost to expectations for the power unit. GE also said it thinks it can spend $500 million less on cash restructuring this year, while still achieving the same level of cost savings. This is odd. Recall that Culp’s predecessor John Flannery was ousted in part because of a perceived lack of urgency and aggression on cost-cutting. Analysts have debated how much more cost-cutting GE could actually do, given already comparatively low levels of back-office and R&D expenses and relatively high sales per employee. The European footprint GE inherited from the Alstom SA deal also complicates its efforts to fire people and shutter factories. For me, the lower restructuring bill raises questions as to whether the multi-year cost-cutting opportunity is as large as billed.

Either way, working against the better power performance and lower restructuring expenses is GE’s estimate of a $1.4 billion hit to 2019 cash flow from operating activities if Boeing Co.’s 737 Max stays grounded through the duration of this year, a likely outcome at this point. GE provides the engine for the Max through its CFM International joint venture with Safran SA. One possible explanation is that Culp was trying to give the company room to fix itself in 2019 and set a low enough bar with his initial guidance that he could simply roll over it. Given GE’s past history with over-promising and under-delivering, I can’t knock the logic of this rationale. But if that is the case, it feels a little too carefully orchestrated. Why give guidance at all really if you’re going to be uber-conservative and continue to rely on heavily adjusted metrics? Why not let the results and the turnaround speak themselves? Perhaps the optics of a potential “beat” proved irresistible. It doesn’t change the fact that GE is losing some of its cash-generating ability through divestitures and likely to face historically low levels of cash flow for the next few years. One thing that seemed notably less carefully orchestrated was the announcement that Chief Financial Officer Jamie Miller would be stepping down. In an interview with Bloomberg News, Culp said this was his decision and he felt the time was right because “things were stable enough.” That suggests it’s a change he’s been contemplating for a while and was just waiting for the proper moment, which makes it all the weirder that GE announced the reshuffling without having a replacement lined up.

NEVER-ENDING TARIFFS

So much for the doldrums of August. President Donald Trump kicked off the typically quiet month by announcing the U.S. would slap 10% tariffs on $300 billion of Chinese imports not yet subject to duties because he doesn’t feel Chinese President Xi Jinping is moving “fast enough” to resolve trade tensions. The tariffs are set to take effect Sept. 1 and Trump has said he may even raise the duties to 25% or higher if talks with China continue to stall. The direct cost of this latest batch of tariffs will likely be incremental for industrial companies, with many of the products and components they import from China included in the $250 billion of goods already taxed by the Trump administration at 25%. It’s a much nastier surprise for consumer-goods companies like Apple Inc., which thus far have managed to stay out of the fray, and for the average American who’s about to see higher prices on some of their favorite toys and electronics. My Bloomberg Opinion colleagues Shira Ovide and David Fickling have great pieces out on this, which you can read here and here. But for manufacturers, this adds to a general environment of uncertainty that CSX Corp. CEO James Foote deemed “one of the most puzzling” economic backdrops of his career. With China reportedly contemplating blacklisting FedEx Corp. over the erroneous rerouting of packages involving Huawei Technologies Co. documents and products, Trump’s latest trade broadside could inspire retaliation against other U.S. companies. The slide in Boeing shares on the tariff news suggests investors are worried about backlash toward the planemaker, whether through canceled or scrapped orders or a tougher regulatory review of its grounded Max jet. More tangibly, this re-escalation of the trade war means the sales slowdown that was a frequent theme this industrial earnings season is unlikely to dissipate and instead set to get worse.

This week brought more evidence of weakening demand from nVent Electric Plc, Gardner Denver Holdings Inc., Parker-Hannifin Corp. and even Siemens AG’s automation software business. The Institute for Supply Management’s gauge of U.S. manufacturing activity came in at 51.2 for the month of July, according to data released Thursday. That’s still indicates expansion, but it’s the fourth straight month of declines and the lowest reading in nearly three years. Thus far, manufacturers have generally been successful at passing along price increases and that, combined with stepped-up cost-cutting, has helped companies deliver earnings beats even as their sales growth slows. The durability of that dynamic will be tested if this wobbling in demand turns into a more clear-cut slump. There had been some hope that a Federal Reserve interest-rate cut would buoy the sector. Whatever push toward new investment may have been inspired by this week’s quarter-point reduction is likely now wiped out by this reopening of the trade-war tensions. Of course, there’s also the possibility that this tariff threat was Trump’s way of forcing the Fed into more rate cuts. Maybe it’s a bluff, like the threat to impose tariffs on all Mexican imports. Who knows? Meanwhile, the bright spots this week were strong numbers from Ingersoll-Rand Plc and Johnson Controls International Plc, which both posted much better organic sales and order growth for their HVAC businesses than we saw earlier in the reporting season from United Technologies Corp.’s Carrier unit and Lennox International Inc. We’ll see if that lasts.

ROUNDING UP MORE PLAINTIFFS

Bayer AG is now facing lawsuits from 18,400 plaintiffs claiming the company’s Roundup weed killer caused their cancer; that represents an increase of 5,000 litigants since April. In a call this week to discuss disappointing quarterly earnings, Bayer CEO Werner Baumann moderately walked back the company’s resistance to settlement talks, saying he’d be open to a “financially reasonable” agreement as long as it resolves all Roundup litigation. The continued buildup in the number of claimants makes it less likely a settlement will meet both those criteria. Last month, a judge reduced a $2 billion jury award to a California couple to $86.7 million, following similar payout reductions in the other two Roundup cases that have gone to trial. But a lawyer representing that California couple noted that the average judgment per plaintiff now sits at $47 million. Every case is different and the awards per plaintiff are likely to be lower in a mass tort settlement, but that’s still a troubling precedent. Analysts’ estimates for a Roundup settlement range from $2.5 billion to $20 billion. Bloomberg Intelligence’s Holly Froum estimates $6 billion to $10 billion, given the surge in lawsuits, and said she’s skeptical a settlement would remove Roundup litigation risks for Bayer as non-parties who may claim injury in the future wouldn’t be bound to it. While Bayer agreed last month to sell the Dr. Scholl’s foot-care business to Yellow Wood Partners for $585 million and is looking to offload its animal-health business, the uncertainty surrounding the Roundup litigation likely limits its ability to consider a bigger breakup.

DEALS, ACTIVISTS AND CORPORATE GOVERNANCE

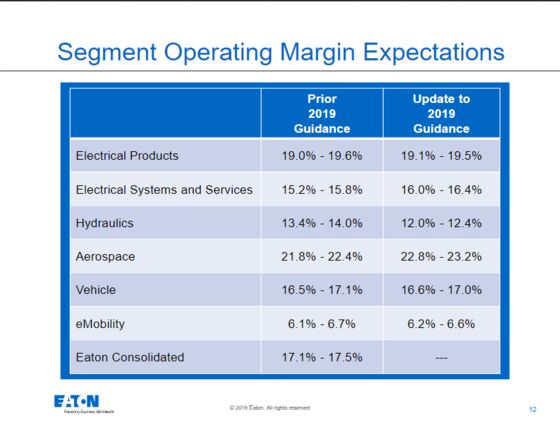

Eaton Corp.’s second-quarter results released this week did little to endear analysts and investors to its current structure. While the company’s aerospace and electrical divisions put up strong numbers despite currency pressures and a more challenging economic environment, the hydraulics and vehicle units were disappointments, yet again. Eaton now estimates organic growth in the hydraulics business will be flat to up 1% for the full year, down from a previous guide of 3% to 4%. Margin expectations for that unit were also slashed. In the vehicle division, Eaton sees as much as an 8% decline in organic sales this year. Asked by Goldman Sachs Group Inc. analyst Joe Ritchie about the hydraulics unit’s long-term fit within Eaton’s portfolio, CEO Craig Arnold pointed out that the company’s overall performance was solid “despite the fact that we have one of our businesses that's not today firing on all cylinders.” That’s true, and yet while I’m wary of industrial companies’ passion for breakups going too far, “despite” is really the key word in Arnold’s comments. This isn’t a momentary slip-up for either the hydraulics or the vehicle business, and they’re increasingly perceived as more cyclical roadblocks holding up even greater margin improvement and sales growth for the overall company. Arnold has signaled in the past that if the company can’t get struggling businesses to targeted profitability levels, that could be a catalyst for divestiture.

Parker-Hannifin agreed to buy Exotic Metals Forming Co. for $1.73 billion. The name might lead you to believe this company crafts metalworks on some sort of tropical island, but it’s based in Washington and makes complex high-temperature engine components and exhaust-management systems for aircraft including the Boeing 737 Max and Lockheed Martin Corp.’s F-35 fighter jet. On the one hand, the addition of Exotic Metals will boost the share of Parker-Hannifin’s revenue tied to faster-growing, more profitable aerospace products to more than 20% by Bloomberg Intelligence’s estimate, which will help to offset the sales slowdown in its industrial-products divisions. At about 13 times 2019 estimated adjusted Ebitda, the Exotic Metals deal is cheaper on that basis than the $3.7 billion acquisition of adhesives and coatings company Lord Corp. that Parker-Hannifin announced earlier this year. But this is another debt-fueled bet on the aerospace industry at a time when skepticism is growing about how much longer the multi-year boom in that sector will last. Exotic Metals’s already high Ebitda margin of nearly 30% and compound annual sales growth of more than 16% over the last three years leave little room for improvement. A goal of a high single-digit return on invested capital in year five for the Exotic Metals deal isn’t terribly impressive to begin with; the risk is, even that is optimistic.

nVent agreed to buy Eldon, a Spanish provider of electrical enclosures, for $130 million. This is nVent’s first takeover of size since the company was spun off from Pentair Plc in 2018. It’s a good deal for CEO Beth Wozniak to start with: the purchase price is a reasonable 1.4 times the $90 million of sales Eldon generated in 2018 and the business is clearly complementary to nVent’s existing electrical protection systems. Eldon will give nVent more products that adhere to European electrical standards, giving it access to a wider swath of customers, RBC analyst Deane Dray wrote in a report. Eldon is also a bit ahead of the curve on automation and digital initiatives and the deal could help speed nVent’s efforts in those areas. In that respect, the Eldon purchase may serve to make nVent a more well-rounded takeover target in its own right, Dray writes.

BONUS READING

Regulators Found High Risk of Emergency After First Boeing MAX Crash

Bad Week for Energy Stocks? Wait Till Next Year: Liam Denning

Shareholders Voted Them Off the Board, But the Board Said No

Helicopter Bankruptcy Highlights Surprise Medical Bill Backlash

Ford Acquires Defense Contractor to Get Robot Rides on the Road

Aston Martin Is Struggling to Stay on the Road: Chris Hughes

To contact the editor responsible for this story: Beth Williams at bewilliams@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Brooke Sutherland is a Bloomberg Opinion columnist covering deals and industrial companies. She previously wrote an M&A column for Bloomberg News.

©2019 Bloomberg L.P.