Funds Turn Bullish on Worst-Performing Kiwi as Key Job Data Loom

Funds Turn Bullish on Worst-Performing Kiwi as Key Job Data Loom

(Bloomberg) -- These are troubling times for the New Zealand dollar but a whiff of optimism is in the air.

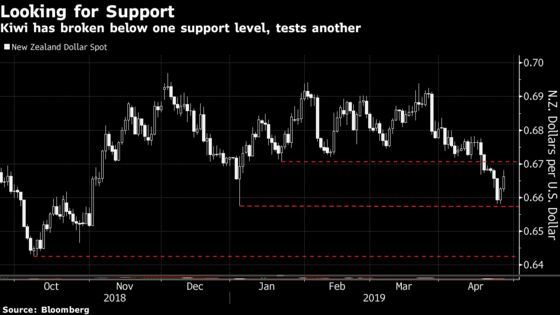

The kiwi has been the worst-performing major currency over the past month, tumbling 3.6 percent, after the central bank said in March the next policy move was likely to be an interest-rate cut. Disappointing first-quarter inflation numbers helped speed its decline.

The double whammy helped push the kiwi to within a whisper of January’s flash-crash low of 65.75 U.S. cents in risk-off trading last week. Momentum indicators such as moving average divergence-convergence and slow stochastics remain in bearish territory.

Amid all this pessimism, one part of the market has turned positive.

Leveraged funds have become bullish on the kiwi for the first time since the start of January, according to data released last week by the Commodity Futures Trading Commission. They held a net long position of 1,845 contracts, compared with a net short position of 25,123 contracts as recently as August.

Positives for the kiwi can be found in its reduced valuation following recent declines, and easing U.S.-China trade tensions that are improving the outlook for risk currencies.

The next big test will be New Zealand’s first-quarter job data due this week. Employment growth is expected to quicken to 0.5 percent, from 0.1 percent in the previous three months, while private wages are also predicted to increase 0.5 percent, according to a Bloomberg survey of economists before the numbers are published Wednesday.

The labor data has taken on added significance since the government passed reforms last year giving the Reserve Bank of New Zealand a dual mandate to include employment in addition to price stability in determining its monetary policy.

There is still plenty of evidence to back the bear case. Swap markets are pricing in a 65 percent chance the central bank will cut rates at its May 8 meeting, compared with little to no odds of a move at that gathering in calculations made in late March.

Any disappointment in this week’s job numbers may see the local dollar take another leg down, and leave leveraged funds wishing they had held on to their short positions.

Below are key Asian economic data and events due:

- Monday, April 29: No major event

- Tuesday, April 30: China manufacturing and non-manufacturing PMI, Australia private sector credit, New Zealand ANZ business confidence, South Korea business surveys manufacturing and non-manufacturing, industrial production, Thailand trade balance and BOP current account balance

- Wednesday, May 1: New Zealand employment change, average hourly earnings and house prices, Japan Nikkei manufacturing PMI, South Korea trade balance, Thailand CPI

- Thursday, May 2: New Zealand building permits, China Caixin manufacturing PMI, South Korea CPI and Nikkei manufacturing PMI, Indonesia CPI, Thailand consumer confidence and business sentiment index

- Friday, May 3: Australia building approvals, Singapore PMI, Malaysia trade balance

To contact the reporter on this story: David Finnerty in Singapore at dfinnerty4@bloomberg.net

To contact the editors responsible for this story: Tan Hwee Ann at hatan@bloomberg.net, Nicholas Reynolds

©2019 Bloomberg L.P.