How Central Banks, Governments Are Fighting The Global Slowdown

Central bankers including Federal Reserve Chairman Jerome Powell will be in Jackson Hole, Wyoming from Thursday through Saturday.

(Bloomberg) --

The leaders of the world economy convene this week 8,000 kilometers apart with the same thing on their mind: What more stimulus do they need to support the weakest global growth since the financial crisis?

Central bankers including Federal Reserve Chairman Jerome Powell will be in Jackson Hole, Wyoming from Thursday through Saturday, while Group of Seven leaders, with U.S. President Donald Trump among them, will hold talks in the French resort of Biarritz over the weekend and Monday.

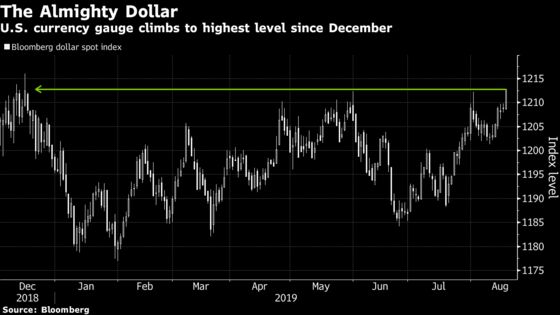

At the heart of the debate in both locations will be an economic outlook dimmed by the U.S.-China trade war and unnerving financial markets, with investors diving into the perceived safety of the dollar and still-positive yields on U.S. Treasuries.

With the Fed having cut interest rates and the European Central Bank likely to follow next month, investors are pressing for even more monetary stimulus. Governments are also under pressure to ease budgets, with Germany already considering action.

“The recent plunge in long-term borrowing costs shows how easy it has been for central bankers to create high expectations. The difficulty now lies in validating them,” said Bloomberg economist Jamie Rush. “There is plenty of scope for slip ups to create volatility in months to come.”

While low borrowing costs, large debts and cautious instincts limit their room for maneuver, here’s what key officials have done recently and may do in coming months in a bid to stave off recession:

Federal Reserve

The Fed is expected to cut interest rates again when it meets next month and ease further before the end of the year. Powell opened the door to more action when he explained policy makers’ quarter-point reduction on July 31 -- their first in a decade -- and investors are looking for additional hints when the chairman speaks on Friday at the central bank’s annual retreat in Jackson Hole.

The U.S. has more room to move than other major central banks, who’ve driven rates into negative territory. But it’s under relentless attack from Trump and will risk looking like it caved to political pressure by acting again.

The ECB

European Central Bank President Mario Draghi is expected to at least cut interest rates at the next meeting in September, shortly before his term ends, and fellow policy maker Olli Rehn says the bank should come up with a bigger stimulus package to overshoot market expectations.

Whatever the ECB decides, it can’t readily be accused of moving too slowly -- unemployment has declined and the economy, while cooling, is still growing.

Whether it’ll have much impact is arguable though. The euro zone is flooded with liquidity and the deposit rate is at a record-low minus 0.4%. More rate cuts will squeeze the profitability of banks, who can’t easily pass the charge onto retail depositors, raising concerns that they’ll pull back lending.

Bank of England

Despite the U.K. economy shrinking in the second quarter, Bank of England policy makers are essentially stuck until at least Oct. 31. That’s when Prime Minister Boris Johnson says he’ll take the nation out of the European Union, whether or not he reaches a transition agreement.

BOE Governor Mark Carney insists that even in a disorderly Brexit, his response won’t be automatic. Inflation is already at target and a slumping pound, coupled with any shortage of goods as tariffs are imposed, would make matters worse. Investors, though, still think Carney would cut rates.

Bank of Japan

Governor Haruhiko Kuroda has said the Bank of Japan can deliver more monetary stimulus if necessary, but it needs to take care due to side effects on the financial system.

In an interview with Bloomberg earlier this year, he cited four policy options: cutting the -0.1% negative rate further, lowering the target for 10-year yields, increasing the monetary base or boosting asset purchases. Amid the rally in global bonds, most market focus has been on the 10-year yield target, which Deputy Governor Masayoshi Amamiya said this month could be widened from the current range of about 0.2 percentage point either side of zero.

Bank of Canada

At their last rate decision in early July, Bank of Canada officials began to more seriously flag elevated concerns about mounting global trade tensions, but showed little willingness to consider immediate easing. That’s why investors continue to see fewer moves, and a slower pace of cutting from Canada, than the Federal Reserve.

A strong run of economic data is affording the Bank of Canada opportunity to resist the dovish turn in global monetary policy, and as a result the country is expected to end up with the highest policy rate among advanced economies within the next 12 months.

People’s Bank of China

The PBOC is in the midst of a major reform to its system of benchmark interest rates, a project that’s intended to make them more market oriented with the side-effect of a short-term reduction in borrowing costs.

With the economy slowing to its weakest pace in almost three decades in the second quarter, the central bank is pushing on with the reform even amid heightened calls for outright cuts to its traditional tools. As the nation faces off against the U.S. in a broadening economic confrontation, officials are signaling they won’t be deflected from their policy aims by a mere dip in growth.

Fiscal Policy

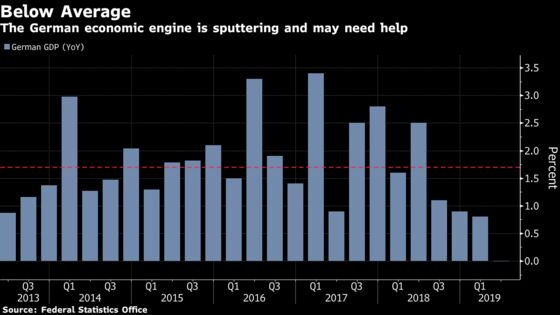

On the fiscal front, Germany’s government is suddenly open to the prospect of stimulus as the economy slides toward recession. Officials are getting ready to bolster domestic output if needed with measures that could include incentives to improve the energy efficiency of homes and support for short-term hiring. Finance Minister Olaf Scholz has said he could muster 50 billion euros in a crisis.

Europe’s largest economy certainly has money to spend after half a decade of budget surpluses and the ability to borrow at negative rates for as long as 30 years, but public spending is bound by constitutional limits and political pressure. So the government might have to wait until things get significantly worse to make its case.

France

French President Emmanuel Macron rolled out a a 17 billion-euro household stimulus package earlier this year in response to the Yellow Vest protests, yet the tax cuts failed to turbo-charge the economy. Growth unexpectedly slowed in the second quarter and consumer spending softened.

France has received warnings from the EU for breaching the bloc’s deficit rules -- and with a budget shortfall that may exceed 3% of GDP this year, the country is looking increasingly like a serial offender.

Italy

Teetering on the brink of recession, Italy could benefit from a fiscal boost. But public debt over 130% of GDP means greater spending would likely bring censure by the European Union and scare the bond market.

To complicate matters, the government is in turmoil after Prime Minister Giuseppe Conte resigned, accusing his deputy Matteo Salvini of a self-interested and irresponsible rebellion. Salvini is pushing for early election and has promised Italians 50 billion euros of tax cuts and public spending if he can take control of the government.

Spain

Spain’s economy has slowed, but it’s still expanding at a decent pace compared to the rest of the euro area, and Madrid is focused on whittling down the budget deficit this year. In any case, acting Prime Minister Pedro Sanchez is struggling to rally support for a new government and could be forced to call another general election in November, leaving his administration little room to approve any stimulus plans.

U.K.

Britain could be in for significant fiscal boost regardless of the terms on which it leaves the EU. Since becoming prime minister last month, Johnson has been announcing spending pledges at a rate of about 2 billion pounds ($2.4 billion) a week, in a deliberate change of course after a decade of austerity. With a no-deal Brexit looming large, the country might need it, though that could also crimp the administration’s ability to deliver.

U.S.

The White House is looking at the potential for more tax cuts to juice the economy -- after an overhaul of levies in 2018 -- as fears of a recession mount. Trump signed legislation earlier this month to suspend the U.S. debt ceiling and boost spending levels for two years.

--With assistance from Paul Gordon, Brett Miller, Theophilos Argitis, Yinan Zhao and Nacha Cattan.

To contact the reporters on this story: Piotr Skolimowski in Frankfurt at pskolimowski@bloomberg.net;Alister Bull in Washington at abull7@bloomberg.net

To contact the editors responsible for this story: Margaret Collins at mcollins45@bloomberg.net, Simon Kennedy

©2019 Bloomberg L.P.