France Ready to Nationalize as EU Heavyweights Take Charge

France Ready to Protect Big Companies Through Nationalization

(Bloomberg) --

France is ready to use the ultimate weapon to protect its biggest companies from the market turmoil set in motion by the coronavirus: nationalization.

With European Union leaders pulling out all the stops to try to get control of the situation and France tearing up its budget plans to promise billions of euros in support for the economy, Finance Minister Bruno Le Maire said the state will intervene in any way necessary to protect the country’s economic assets.

“I will not hesitate to use all the means available to me,” Le Maire said. “That can be capitalization, that can be by taking stakes, I can even use the term nationalization if necessary.”

Following President Emmanuel Macron’s promise to guarantee 300 billion euros ($335 billion) of bank loans last night and Chancellor Angela Merkel earmarking another 550 billion euros of state lending to support German businesses, the EU’s economic heavyweights are deploying their budget muscle to support companies as the continent shuts its doors to ride out the pandemic.

The EU also plans to clear the way for national efforts. A draft proposal, circulated by Brussels, says curbs on state handouts should be loosened to aid virus-stricken industries while Spain pledged to mobilize as much as 200 billion euros to shore up activity.

As the continent heads for a savage recession, the measures are designed to backstop the economy, preserve jobs and reassure investors as the leaders ask their citizens to accept unprecedented curbs on daily life in order to control the spread of the deadly virus.

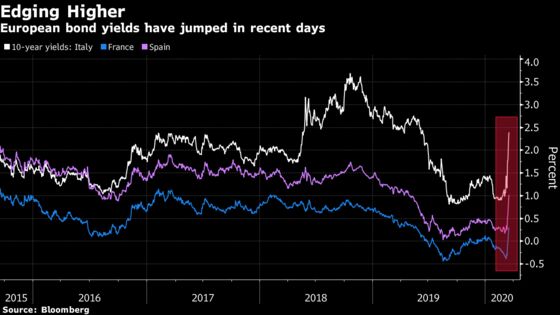

European bonds markets have been in turmoil as investors try to gauge the impact of the outbreak -- and they weren’t helped by European Central Bank President Christine Lagarde’s botched intervention on Thursday.

While Italian yields have surged this month, with 10-year rates more than doubling to around 2.4%, they remain well short of the almost 7.5% euro-era record seen during the debt crisis. German yields have also rebounded from record-lows as investors ready for more spending, but 10-year rates are still negative.

EU leaders will hold another emergency telephone call later on Tuesday to discuss closing borders and other efforts to combat the spread of the virus.

Italy, the worst-hit country in Europe, approved a 25 billion-euro package to support its strained health system while helping businesses and families with delayed tax payments and mortgage relief. Sweden’s central bank added $30 billion to its bond-buying program late Monday, bringing its total package including bank funding and state aid to as much as $200 billion.

Spanish Prime Miniser Pedro Sanchez announced a mix of loan guarantees, state subsidies and private funding that could amount to as much as 20% of the country’s GDP. “These are exceptional circumstances that require exceptional measures,” Sanchez said at a news conference Tuesday.

War Footing

In a series of public addresses Monday night, the leaders of countries from Finland to Germany sought to convince populations of the need for restrictions ranging from school and workplace closures to the shuttering of non-essential shops and services. Alongside efforts to prepare national populations for sacrifice, the EU was battling to maintain cohesion as the crisis threatens to tear at the bloc’s bonds.

“We are at war,” Macron said in an address to the French people on Monday evening, making the case for national unity and shared sacrifice.

Hotels and taxis will be requisitioned for health workers, all proposed reforms, including his controversial pension overhaul, are to be halted, while the government will ensure that no business is allowed to fail. Bank loans will be guaranteed for companies and a solidarity fund created for workers affected by the fallout of the virus containment.

In the process, Macron is upending the economic philosophy that brought him to power in 2017 promising to pare back the presence of the state in economic life.

French Industry

Already last week, Le Maire said the government would back companies in which it has a stake. This includes a broad swathe of the travel sector which has been particularly hard hit. The government holds substantial shares in firms ranging from Airbus SE and Renault SA to Air France-KLM and Aeroports de Paris, as well as an indirect holding in Peugeot maker PSA Group.

Air France-KLM has grounded planes and taken steps to bolster cash by drawing down credit lines, warning that drastic cost-cutting measures can only make up half of the sales lost from taking out as much as 90% of capacity. Global airport operator ADP has also been hit by the near-halting of air traffic, first to China, then the U.S. And now even more broadly.

Europe’s carmakers, including PSA, Fiat Chrysler Automobiles NV and Volkswagen AG,have also taken extraordinary measures to shutter production sites as demand cools, health concerns grow and the delivery of parts gets snarled up.

Still, nationalizations and recapitalizations could involve delicate and complex negotiations with other nations. The Dutch and French governments have already discussed a recapitalization of Air France-KLM, but any move must be coordinated so that the two states aren’t diluted, a person familiar with the discussions said. Italy has stepped up efforts to keep bankrupt Alitalia afloat, with a new 600 million-euro loan under discussion as part of a plan to re-nationalize the carrier.

Stimulus Plan

Le Maire brandished the possibility of nationalizations as he gave details of an emergency budget that will include 45 billion euros of spending to cover salaries of furloughed workers and support companies in addition to the loan guarantees. France’s debt will rise above 100% of economic output.

The action is based on the economy shrinking 1% this year. But even that could be much worse depending on how the epidemic evolves in the coming weeks, Le Maire said.

“This economic and financial war will be long,” he said in a telephone briefing with journalists. “It will be violent and will require all the strength or our nation,” as well as Europe and the Group of Seven, he said.

©2020 Bloomberg L.P.