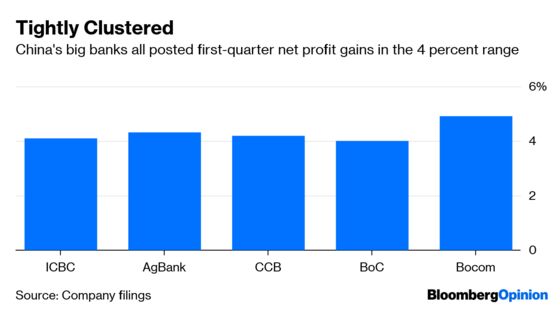

(Bloomberg Opinion) -- China's banks doled out a fifth more loans in the first quarter than a year earlier, so profit increases shouldn't be surprising. What’s striking is just how small – and similar – those gains are.

On Monday, Industrial & Commercial Bank of China Ltd., Bank of China Ltd., China Construction Bank Corp. and Bank of Communications Co. posted higher net income. Including Agricultural Bank of China Ltd., which reported last week, rises at the big five clustered in a range from 4.1 percent to 4.9 percent.

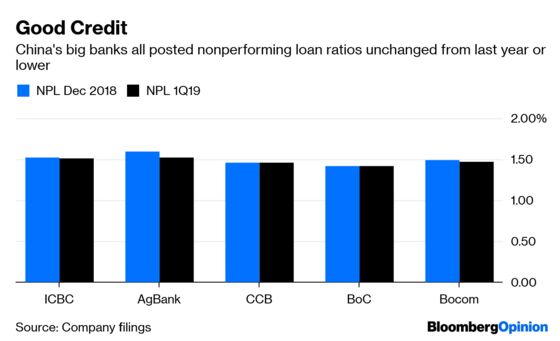

At the same time as profit climbed, nonperforming loans as a ratio of total lending dropped – though overall levels of bad debt increased.

The reason is that most of the biggest banks set aside more money against soured loans (BoCom was the exception, keeping its provisions little changed). AgBank, for instance, raised its bad debt coverage ratio to 263.9 percent in the first three months, from 252.2 percent in the period through December.

Why crimp profit growth by raising these buffers when they are already so conservative? The government requires a 120 percent to 150 percent level of provisions to guard against defaults. Global banks have far lower protection levels: London-based Standard Chartered Plc, for instance, had a coverage ratio of 59 percent last year.

Leaving aside the obvious explanation that the banks’ actual bad debt levels are higher than reported, the answer has implications that are simultaneously troubling for shareholders and positive for the broader economy. In short, the trend may signal that the government is succeeding in pushing lenders to extend more credit to private entrepreneurs. Banks, in turn, are anticipating more bad debt as a result.

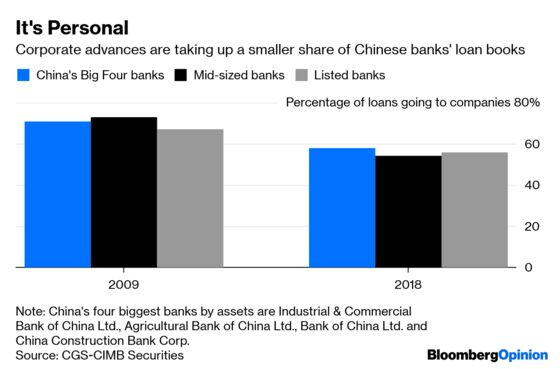

With the economy struggling, the government needs to channel more funds to China’s private sector, which is the engine of most output and job creation. For banks, though, lending to private companies is riskier than providing credit to state firms or consumers. NPL ratios for mortgages are well below those for corporate loans.

A resurgence in corporate lending would signal a break in the trend toward consumer loans, particularly mortgages. By the end of last year, 58 percent of loans by the Big Four banks (excluding BoCom) went to companies, versus as much as 71 percent in 2009, according to Michael Chang, a banking analyst at CGS-CIMB Securities Hong Kong Ltd.

Some reversal was evident during the first quarter, especially for new loans. While AgBank’s corporate lending rose slightly to 59 percent from 58 percent for the whole of last year, corporate advances accounted for 66 percent of new loans in the first three months, versus 36 percent in all of 2018.

It’s another reminder that China’s banks are tools of state policy rather than profit-maximizing commercial entities. Provisions are managed so that earnings don’t surprise too much. That may be a disappointment to investors hoping the first quarter’s eye-popping loan growth would translate into share rallies. Then again, a healthier economy should be good for everyone.

To contact the editor responsible for this story: Matthew Brooker at mbrooker1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Nisha Gopalan is a Bloomberg Opinion columnist covering deals and banking. She previously worked for the Wall Street Journal and Dow Jones as an editor and a reporter.

©2019 Bloomberg L.P.