Selling by Foreign Funds Proves Harbinger of Asia Bond Gains

Buying when outflows rise leads to gains at least 77% of time.

(Bloomberg) --

Selling by foreign funds most often results in gains for investors during the following three months, according to a Bloomberg analysis of flow data for six emerging-Asian debt markets.

Investors who bought when outflows climbed above the five-year average made a positive return at least 77% of the time between September 2015 and October 2019, versus a 64% chance of making a profit for all trades during the period, the study found. When outflows climbed to 1.75 standard deviations above the average, the chance of a positive return jumped to 84%.

On the flip side, investing during times of rising inflows frequently ends up being a bad idea, according to the study which looked at Indonesia, the Philippines, Malaysia, South Korea, Thailand and India.

When net purchases climbed to 0.5 standard deviations above the five-year average, 47% of investments lost money in the next three months. This compares with an overall loss rate of 36% for all observations. When inflows increased to 1.25 standard deviations above the average, the chance of losing money rose to 53%.

Coronavirus Impact

The counterintuitive nature of the findings highlight the difficulty of judging when to invest in emerging-market debt, particularly during periods such as the current coronavirus outbreak.

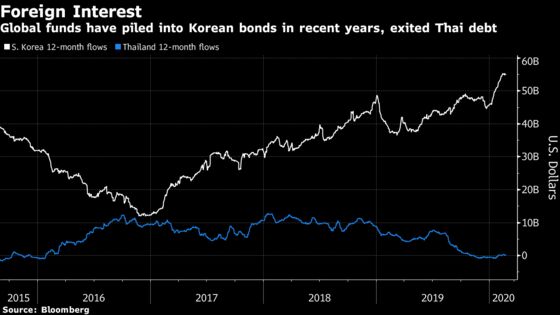

The recent escalation in the epidemic -- which has spread from China to such far-flung countries as Italy and Canada -- has sparked risk-off sentiment that has seen foreign outflows from stocks in all the six countries in the study this year, while there remains a net inflows into their bonds. Rolling 12-month foreign inflows into South Korean bonds are close to a record as the escalation in virus cases increases bets for further easing.

Read more: Hong Kong Stimulus; Korea Cases Top 1,000: Virus Update

At the same time, the extra yield, or carry, for putting money into the six countries may encourage investors to maintain positions for longer, especially with the decline in U.S. Treasury yields. Investors may also decide to hold on due to optimism the virus outbreak will lead to further interest-rate cuts from central banks. U.S. 10- and 30-year yields both dropped to new record lows on Tuesday.

Here’s how the analysis was compiled:

- The study looked at bond flow data for the six economies, which captures a spread of markets in terms of involvement by foreign investors. Global funds own as much as 38% of Indonesia’s outstanding local-currency sovereign debt, compared with as little as 3% of India’s

- Current and historical figures were then analyzed to generate z-scores, which show how far a data point is from the mean. If there was a bond outflow, or negative z-score, and there was a positive return three months later, this would count as a “win.” A bond inflow that led to a negative return, counted as a “loss”

- Returns were calculated using Bloomberg Barclays EM local currency total return unhedged dollar indexes

Standard deviation of foreign outflows versus 5-year average | Occurrences | Win Rate From These Occurrences |

|---|---|---|

| No threshold | 300 | 64% |

| 0 | 152 | 71% |

| -0.5 | 100 | 77% |

| -1 | 64 | 81% |

| -1.5 | 31 | 81% |

| -1.75 | 25 | 84% |

Standard deviation of foreign inflows versus 5-year average | Occurrences | Loss Rate From These Occurrences |

|---|---|---|

| 1.25 | 30 | 53% |

| 1 | 48 | 52% |

| 0.5 | 89 | 47% |

| 0 | 136 | 43% |

| No threshold | 300 | 36% |

--With assistance from Simon Flint, Liau Y-Sing, Hooyeon Kim and Kartik Goyal.

To contact the reporter on this story: Marcus Wong in Singapore at mwong547@bloomberg.net

To contact the editors responsible for this story: Tomoko Yamazaki at tyamazaki@bloomberg.net, Nicholas Reynolds

©2020 Bloomberg L.P.