For the Roaring U.S. Dollar, Factory Slowdown Is Just a Speed Bump

Even the first U.S. manufacturing contraction since 2016 can’t keep the dollar down.

(Bloomberg) -- Even the first U.S. manufacturing contraction since 2016 can’t keep the dollar down amid spiraling U.S.-China trade relations and dim European economic prospects.

That’s the view of analysts at firms including Societe Generale and TD Securities who expect the dollar to power past Tuesday’s surprisingly weak manufacturing release.

While the print shows that the U.S. isn’t immune to global trade weakness, economic data will need to slow more dramatically before traders ditch the greenback, according to SocGen’s Kit Juckes, given that U.S. yields are still higher relative to the rest of developed markets.

“It’s like trying to start your car on ice or in mud,” said Juckes, chief global FX strategist. “You’re going to have to run this engine for a bit before you get any traction on a weaker dollar.”

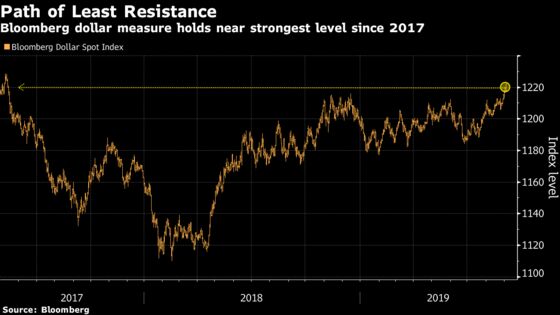

The Bloomberg dollar index surged to its strongest level since May 2017 Tuesday, following two months of gains amid weakness in the euro and yuan. The gauge remained close to that level, despite a 0.2% tumble.

Unwinding Hedges

Washington’s refusal to delay tariffs on China over the weekend is helping fuel the dollar’s rally as traders unwind risk-on hedges, according to Jordan Rochester, a currency strategist at Nomura International Plc. The onshore Chinese yuan tumbled in August, suffering its biggest monthly loss since January 1994, when the modern exchange-rate regime was adopted.

“There were folks who had to hedge for the slight possibility that U.S.-China found a way to de-escalate trade tensions before the latest round of tariffs came in this weekend,” Rochester said, adding that bullish offshore yuan and Australian dollar positions and short yen bets were likely the preferred methods. “Those short-term risk-on hedges were taken off yesterday. As a result, dollar headed higher.”

In the near-term, Rochester remains bullish on the dollar. Factors that could see the greenback weaken would include fiscal stimulus from China, the Federal Reserve embarking on a new round of quantitative easing, or geopolitical events in Europe calming down, but that’s “all unlikely for the time being,” he said.

Boston Fed President Eric Rosengren said in a speech Tuesday evening that if economic data continues to show growth, there is no need for the central bank to change its policy stance. While Rosengren is a voter this year, he dissented against the central bank’s rate cut in July and is seen as a moderate monetary policy hawk.

European Easing Expected

Investors would be remiss to pile into bullish euro positions ahead of the European Central Bank’s meeting next week, cautioned TD Securities analyst Mazen Issa. He expects the central bank to deliver a 20 basis point deposit rate cut and renewed quantitative easing to the tune of $40 billion per month.

“EUR/USD continues to trade on its backfoot after the floorboards at 1.10 broke on Friday,” Issa wrote in a note Tuesday. “We do not think the move should be faded ahead of the ECB’s large-scale easing next week.”

The common currency fell as low as 1.0926 Tuesday, its weakest level since May 2017. The euro briefly erased losses following the weaker-than-expected U.S. manufacturing data, before resuming its slide.

Best of the Rest

While U.S. economic growth has slowed -- the latest evidence on display Tuesday with manufacturing data contracting for the first time in three years -- it still looks resilient relative to the rest of the world. And with the global stock of negative-yielding debt now amounting to $17 trillion, it’s little wonder the greenback remains bid as investors search for yield, according to Juckes.

Even as Citigroup Inc.’s Economic Surprise Index for the U.S. is in negative territory -- meaning reports are tending to miss expectations -- it has rebounded in the past few months, and is well above Europe’s gauge.

“The U.S. has had more growth, higher rates, higher bond yields -- money flows to the U.S.,” Juckes said. “I wouldn’t over-think it when you’ve got negative yields in Japan, the Eurozone, in Switzerland.”

To contact the reporters on this story: Katherine Greifeld in New York at kgreifeld@bloomberg.net;Sarah Ponczek in New York at sponczek2@bloomberg.net

To contact the editors responsible for this story: Benjamin Purvis at bpurvis@bloomberg.net, Debarati Roy, Mark Tannenbaum

©2019 Bloomberg L.P.