Flirting With Negative Rates Is Reality of a Zero-Bound World

Fed successfully quashed bets of negative interest rates in the U.S., only to see yet another benchmark rate dip below zero.

(Bloomberg) -- The Federal Reserve appears to have succeeded in quashing bets on a future of negative interest rates in the U.S., only to see yet another benchmark rate dip below zero.

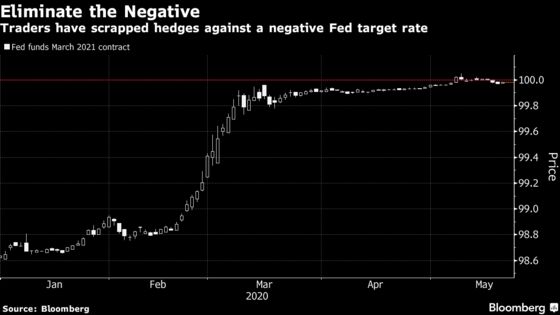

Hedges against a further rate cut disappeared from swaps and fed funds futures contracts this week, after a string of Fed officials, including Chair Jerome Powell himself, reiterated their aversion to a policy of negative interest rates. Then the benchmark for secured funding markets, the general-collateral rate, dropped below zero again Wednesday.

The Fed’s unlikely to sweat this drop, as technical factors are key to both the behavior of general collateral and the derivatives trades that showed up earlier this month. But it’s the reality of this world, with rates barely above zero in the U.S., that questions of whether and how key rates can remain positive are likely to keep popping up.

Speculation may get harder to dismiss, as negative rates are a live topic on the other side of the Atlantic. The European Central Bank is showing no signs of abandoning its policy, and the Bank of England is increasingly split on the issue, with Governor Andrew Bailey saying Wednesday that the central bank isn’t excluding the idea of taking borrowing costs below zero. The U.K. sold its first bond with a sub-zero yield Wednesday.

The drop in the U.S. overnight GC repo rate below zero may prove short-lived. These rates tend to slip as government-sponsored enterprises park cash for principal and interest payments in the repo market around mid-month, and that money typically exits the following week in distributions to mortgage-bond holders.

Strategists have attributed the positioning that popped up in futures for fed funds and overnight index swaps earlier this month to technical accounting issues. But their evaporation this week may mean that the market has heeded the Fed’s message that it’s not ready to embrace a policy that could harm savings, not to mention the $4 trillion money-market industry and bank profits.

©2020 Bloomberg L.P.