Five Charts Showing Why Chinese Bonds Will Lure Foreigners

Five Charts Showing Why Chinese Bonds Will Lure Foreign Buyers

(Bloomberg) -- Chinese government bonds -- one of the few investments to have a positive return this year -- are likely to hold their appeal to foreign investors in 2019, despite recent selling.

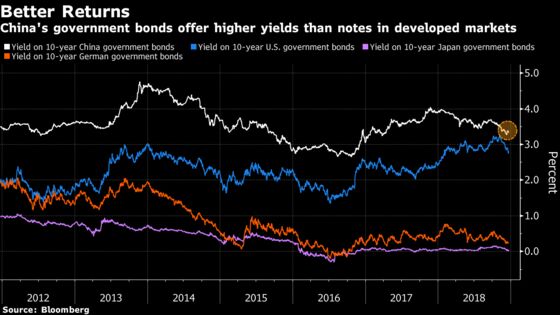

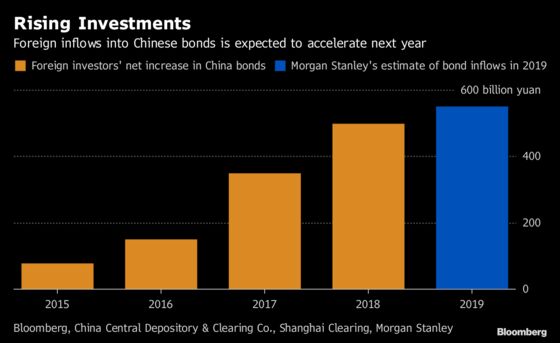

The yield on 10-year government debt fell 55 basis points to 3.35 percent this year as the economy slowed and a collapse in the stock market sent investors to the shelter of state debt. While foreigners turned net sellers of Chinese bonds last month for the first time in almost two years, overseas net inflows so far this year were more than 450 billion yuan ($65 billion).

Positive tailwinds for the $12 trillion market next year include a potentially steadier yuan, lower funding costs and continued monetary easing. China’s top policy makers confirmed last week that more stimulus will be rolled out to support a slowing economy in 2019. Although the rally in debt has been called a bubble, bonds may be buttressed by passive inflows thanks to global index inclusions. Foreign holdings remain small, at about 2 percent of the market, according to official data.

"We are short-term bullish on Chinese government bonds," said Manu George, director of fixed income at Schroder Investment Management in Singapore, adding that the company has been adding to onshore debt during the year. "With China’s economy moderating and stimulus programs likely to pick up in the future, the bond market is poised to deliver attractive returns."

Read more: State Street Global Advisors, Pictet Asset Management and JPMorgan Asset Management are among investors bullish on China bonds

Here are five charts that show why government debt is likely to hold its appeal:

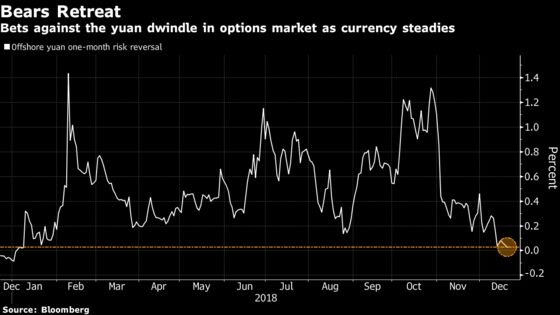

The offshore yuan’s one-month risk reversal last week dropped to its lowest level since January, reflecting weaker demand for bets against the Chinese currency in the options market. Global investment banks including Goldman Sachs Group Inc. and UBS Group AG have raised their forecasts on the yuan, while Standard Chartered Plc expects a 3.7 percent advance to 6.65 per dollar by the end of next year. The currency has fallen 5.7 percent in 2018.

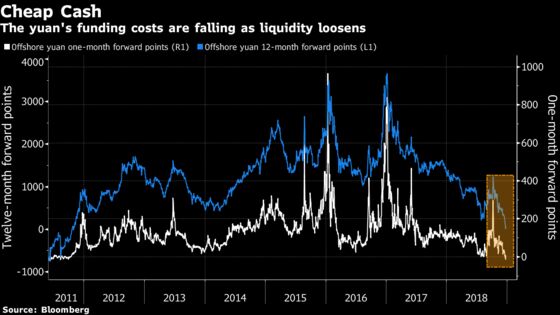

Cheap funding costs are another incentive for foreigners to buy onshore bonds. The offshore yuan’s 12-month forward points tumbled to its lowest level since 2011 amid loose liquidity last week, making it much cheaper for overseas investors to borrow the Chinese currency. Its one-month forward points slumped into negative territory, suggesting overseas funds even get paid by obtaining yuan financing.

Despite the year’s declines, the yield on China’s sovereign notes due in a decade remains higher than those of government bonds in developed markets. The debt also offers diversification benefits with low correlation to other global asset classes, according to Cary Yeung, a portfolio manager at Pictet.

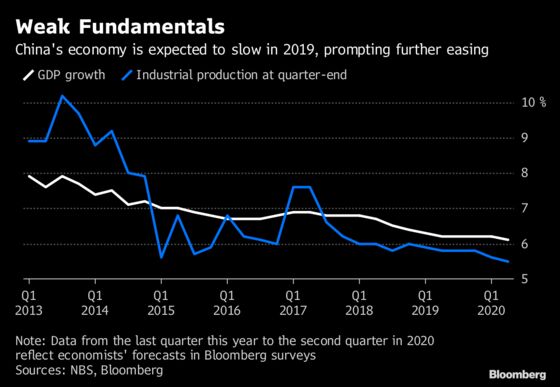

China’s economy is likely to slow further in the coming years, with the growth in gross domestic product expected at 6.2 percent at the end of 2019, according economists’ median forecasts in a Bloomberg survey. That could prompt the central bank to further ease monetary policy -- China International Capital Corp. projected at least 200 basis points of reduction in the reserve requirement ratio next year.

China’s bond market will see $80 billion of inflows next year, according to Morgan Stanley, with some of the onshore debt on track for a phased-in inclusion in the Bloomberg Barclays Global Aggregate Index in April. Another $140 billion of foreign funds may enter the market if two other bond indexes follow suit, the bank said.

"One of our top picks for 2019 is still Chinese bonds," Hayden Briscoe, head of fixed-income for Asia Pacific at UBS Asset Management, said on Bloomberg Television Monday. "We think liquidity is still going to be pumped into the economy," adding that more plentiful cash supply would be "very, very supportive" for the debt market.

--With assistance from Claire Che and Ron Harui.

To contact the reporters on this story: Tian Chen in Hong Kong at tchen259@bloomberg.net;Xize Kang in Beijing at xkang7@bloomberg.net

To contact the editors responsible for this story: Richard Frost at rfrost4@bloomberg.net, Magdalene Fung, Philip Glamann

©2018 Bloomberg L.P.