Shoot Now and Risk Firing Blanks: Lagarde’s Virus Dilemma at ECB

Shoot Now and Risk Firing Blanks: Lagarde’s Virus Dilemma at ECB

(Bloomberg) -- The first crisis of European Central Bank President Christine Lagarde’s four-month tenure will force her to decide this week whether to fire one of the few monetary-policy bullets she has left.

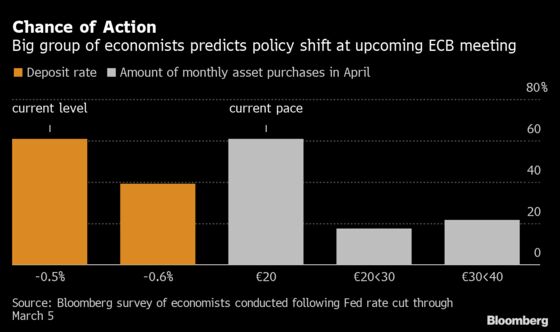

Days after the Federal Reserve slashed interest rates, Lagarde and fellow policy makers must judge if the economic effect of the coronavirus merits cutting the euro area’s benchmark from the current minus 0.5%.

Plunging global markets on Friday were a reminder that investors are seeking more stimulus, and oil’s crash on Monday heightened the sense of financial shock.

An ECB reduction of at least 10 basis points on Thursday should satisfy those expectations and add the euro-area central bank to the list of monetary authorities using rates to shield their economies. But it could also backfire by doing little to address the specific impact of a health emergency, undermining financial stability and reducing policy space the bank might be better off preserving.

Bank economists are split. UBS and Goldman Sachs are among those forecasting a cut, while Bank of America, Morgan Stanley and HSBC expect no change in rates.

Some expect the pace of quantitative easing to be stepped up.

“Even though the ECB doesn’t cater or shouldn’t cater to financial markets, you have to take into consideration the risk of disappointing markets and triggering a further correction,” said Katharina Utermoehl, senior economist for Europe at Allianz in Frankfurt. “A rate cut is not going to help problems in the real economy, so it has to be a part of a more comprehensive package.”

Mindful that disruptions to global supply chains and travel are straining cash flows at companies, Lagarde and her 24 Governing Council colleagues are seen delivering measures to support liquidity when they meet. Options likely under consideration include incentives for banks to keep funding virus-hit firms.

Lenders are already making overtures -- for instance, Germany’s HypoVereinsbank is advertizing options to refinance loans or extend repayment deadlines -- though they’d no doubt welcome ECB support.

While European governments are slowly starting to offer help to companies, Lagarde is also likely to issue another plea for fiscal backup.

But how to deploy interest rates is sure to be a headache. While Lagarde has pledged to do what’s needed, the limited space for monetary policy puts her in a much tighter bind than her international peers. The Fed’s target rate is still above 1% even after last week’s reduction of half a percentage point.

The ECB’s prevailing limitation is that the longer it pursues its ultra-loose policies of negative rates and bond purchases, the worse the side effects will get. Bank margins could be squeezed so hard that lending dries up, and overvalued asset prices -- such as homes -- could cause financial instability.

Economists aren’t convinced that blunt monetary stimulus is the best strategy anyway. Former ECB Vice President Vitor Constancio weighed in on that topic on Twitter last week.

Lagarde’s pledge to deliver “targeted” measures if needed suggests the ECB may adapt its existing program of long-term loans to financial institutions or plan a new variant of it. The initiative, which has run on and off since 2014, gives banks an incentive to lend to companies and households, and could probably be tweaked to target SMEs.

It may be the most appropriate response -- JPMorgan Chase economist Greg Fuzesi has even come up with a model for how it could be designed -- but on its own it might not satisfy the investors who Lagarde has said “interpret, misinterpret or overinterpret our actions.”

What Bloomberg’s Economists Say...

“Smaller firms are particularly at risk of bankruptcy when facing temporary cash shortages and we expect the ECB to launch a new refinancing program specifically targeted at small and medium-sized enterprises.”

- Maeva Cousin, David Powell and Jamie Rush. Read their ECB PREVIEW

Elsewhere, the Bank of England and the U.K. government are coordinating complementary measures for maximum impact. The U.S. agreed a $7.8 billion emergency spending bill, and is said to be drafting more measures to blunt the economic fallout. Japan, which also has negative rates, will offer interest-free loans to SMEs experiencing a sharp drop in revenue.

In Europe, only Italy has so far announced significant fiscal measures. Germany, the region’s largest economy and the one with the most public cash to spare, agreed after more than seven hours of talks late Sunday to loosen rules on wage support for companies that halt production. It will also invest an additional 12.4 billion euros ($14.1 billion) between 2021 and 2024 -- falling short of a full-blown stimulus package.

For Nick Kounis, an economist at ABN Amro in Amsterdam, the slowness of fiscal responses is a reason for Lagarde to be decisive now.

“I do believe that the ECB will eventually do whatever it takes,” he said. “Looking like you are being dragged kicking and screaming into it doesn’t look great. You need to give people more clarity.”

--With assistance from Carolynn Look.

To contact the reporters on this story: Paul Gordon in Frankfurt at pgordon6@bloomberg.net;Piotr Skolimowski in Frankfurt at pskolimowski@bloomberg.net

To contact the editors responsible for this story: Paul Gordon at pgordon6@bloomberg.net, Jana Randow, Craig Stirling

©2020 Bloomberg L.P.