Fighting Against Bank of Japan May Not Be Crazy After All

The analysts argue that the BOJ’s toolkit is designed to push down yields, rather than lift them.

(Bloomberg) -- Explore what’s moving the global economy in the new season of the Stephanomics podcast. Subscribe via Pocket Cast or iTunes.

Going against a central bank is an investment strategy fraught with peril, but some bond market analysts think the Bank of Japan will fail to steepen the yield curve.

The analysts argue that the BOJ’s toolkit is designed to push down yields, rather than lift them. And even if the central bank succeeds for a time, as it did this week, a tide of money seeking yields in a slowing global economy will prove stronger.

“We usually say, ‘Don’t fight the BOJ!’, but this time I think it works to go against them,” said Koichi Sugisaki, a strategist at Morgan Stanley MUFG Securities Co. in Tokyo. Sugisaki points to how Japanese institutions are waiting to snap up bonds with maturities of 20 years or more whenever yields climb.

The BOJ may be the only major central bank trying to actively fight a global collapse in bond yields that has already seen benchmark Treasury rates more than halve in the past year. It signaled deep cuts in bond purchases for October, and indicated it may even stop buying debt of more than 25 years -- a big step for a central bank that pioneered ultra-loose monetary policy.

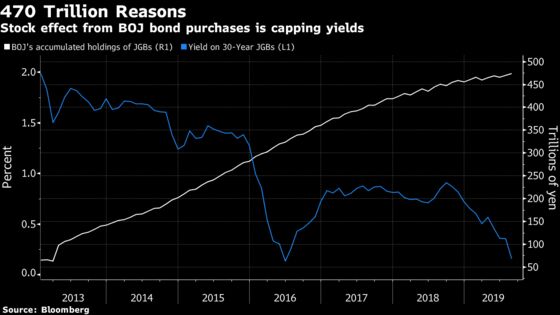

In the six-and-a-half years since Governor Haruhiko Kuroda launched his monetary campaign, the central bank has boosted its holdings of JGBs five-fold to about 470 trillion yen ($4.4 trillion). It has drained almost half of the supply in the market, creating what the BOJ calls a “stock effect” that acts to suppress yields. Cutting weekly purchases, which is about affecting “flows”, may have less impact on how yields behave, according to Nomura Securities Co.

“The stock impact has been strengthening,” said Takenobu Nakashima, a senior rates strategist at Nomura in Tokyo, who pointed to a 2018 research paper from the BOJ that indicated its massive JGB holdings accounted for 90% of the move in yields during a period it studied.

In the past month, as the central bank steadily cut bond purchases, the 10-year yield has climbed about 7 basis points. The impact has been more pronounced for debt maturing in 30 years, with an advance of about 24 basis points.

Yusuke Ikawa, Japan strategist at BNP Paribas Securities in Tokyo, is also skeptical that the steepening will last. “It will be difficult to halt a bull-flattening if overseas yields resume their decline,” said Ikawa.

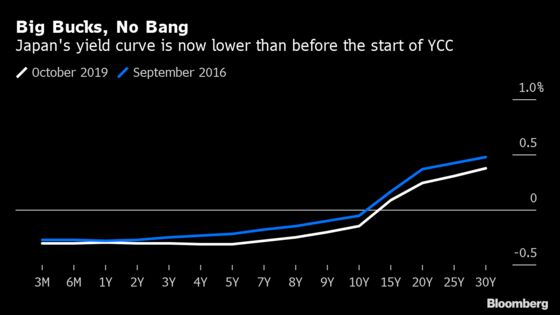

The BOJ’s seeming success has taken place amid a pause in the global bond rally, with Treasury yields rebounding in September. History may be against the Japanese central bank, too. For all the money it has spent, it hasn’t engineered significant change in rates since shifting its policy emphasis to yield-curve control on 2016.

To be sure, analysts agree that yields would be even lower if the BOJ didn’t slow the pace of purchases.

Its October bond market plan announced earlier this week slashed the purchase ranges for four major maturities zones and indicated it could skip some buying operations.

Investors got their first taste on Friday of how the plan plays out, with the central bank announcing purchases of 350 billion yen of the 5-10 year maturities zone. The amount was unchanged from the previous operation on Sept. 26 but well below 480 billion yen just two months ago.

The BOJ is scheduled to buy bonds on Monday in maturity ranges covering 1-3 years, 3-5 years, 10-25 years and over 25 years.

Future monthly bond plans could be tweaked to adjust the boundaries of the maturities zones and the BOJ could also state that it won’t accept offers below certain yield levels, according to analysts.

Click here to see a comparison of the October and September plans

The elephant in the room for the BOJ is what it will ultimately do with its huge hoard of JGBs.

Analysts see the outright sale of bonds by the central bank as unrealistic for now, because it would contradict the broader policy of expanding the monetary base -- and could spur a rally in the yen, which would hurt exporters and efforts to boost inflation.

Market speculation is also rife that the BOJ may cut its short-term policy interest rate -- currently set at minus 0.1% -- even further into negative territory at its next board gathering on Oct. 30-31.

One big risk of doing this, according to analysts, is that instead of steepening the yield curve, it could pull down rates in general.

“It would be contradictory to lower the negative rate and want to prevent long- and super-long yields from falling too much,” said Nakashima.

--With assistance from Paul Jackson.

To contact the reporters on this story: Chikako Mogi in TOKYO at cmogi@bloomberg.net;Masahiro Hidaka in Tokyo at mhidaka@bloomberg.net

To contact the editors responsible for this story: Tan Hwee Ann at hatan@bloomberg.net, Brett Miller

©2019 Bloomberg L.P.