Multinationals Are The World’s Bogeymen Again

While popular discontent at the role of cross-border companies may have died down, they now are in the sights of another enemy.

(Bloomberg Opinion) -- Once upon a time, multinational corporations were such an essential and respected building block of the world economy that only die-hard anti-capitalists opposed them.

How things have changed. While popular discontent at the role of cross-border companies may have died down, they now find themselves in the sights of a far more dangerous enemy. As the world’s two biggest economies take pot-shots at each other, it’s multinationals that are getting caught in the political firing line.

China’s Ministry of Commerce has said it will establish a list of “unreliable entities” for foreign companies that discriminate against the country’s firms or otherwise threaten its industries or national security. The government started an investigation of FedEx Corp. too, accusing it of misdirecting packages. That looks a lot like a retaliation against President Donald Trump’s decision last month to blacklist Huawei Technologies Co., preventing U.S. companies from doing business with the Shenzhen-based telecommunications giant.

The new atmosphere is bad news for companies like Apple Inc., Toyota Motor Corp., and Constellation Brands Inc., which depend on supply chains spanning borders where tariff levies are now rising. At the same time, it’s little more than an acceleration of a trend that’s been crystallizing for a while.

The former can be considered the extent to which industries concentrate their activities in countries with the strongest comparative advantage, improving productivity by (say) locating a car company’s tire-making in a place with ready access to rubber while its final assembly is set up somewhere with a large workforce.

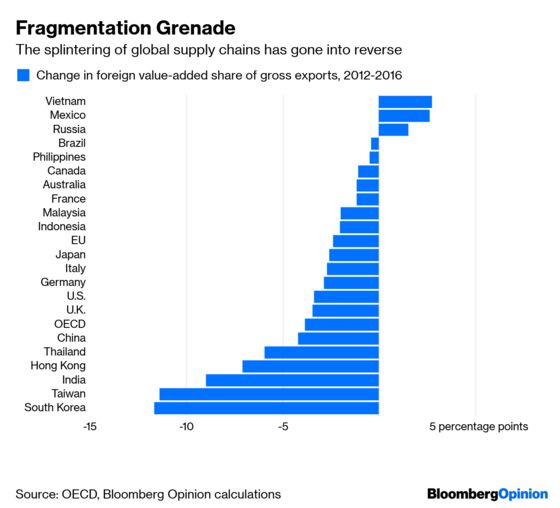

Such fragmentation had been sharply retreating even before Trump’s election as U.S. president. The share of foreign value-added in gross exports from members of the Organization for Economic Cooperation and Development fell to 19% in 2016 from 23% in 2012, according to figures from the group, meaning activity was increasingly happening in fewer countries. That trend has been even more pronounced in emerging markets, falling to 33% from 38% in Thailand; to 30% from 41% in Taiwan; and to 16% from 25% in India over the same period. Next to those countries, China’s decline to 17% from 21% looks almost modest.

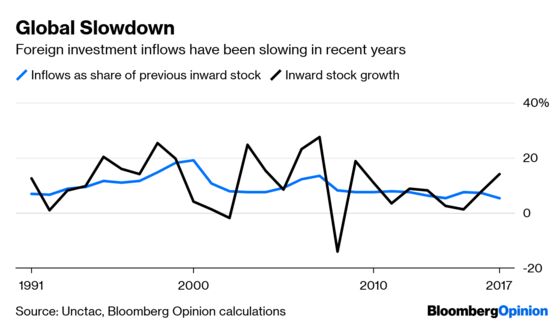

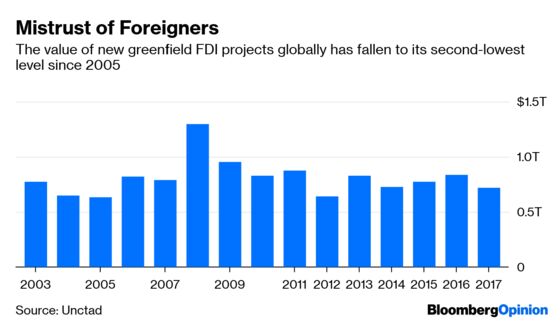

To split up a supply chain, you must first spend money on the myriad facilities it will use around the world. But growth in foreign direct investment is heading toward its weakest levels since the Cold War. New FDI inflows of $1.43 trillion in 2017 came to just 5.2% of the existing $27.66 trillion inward investment stock. The value of new greenfield FDI projects came to just $720 billion in 2017; that was the second-lowest figure since 2005, after 2012. The $53 billion of greenfield investments in China was the lowest since 2003.

That decline is what makes the current situation particularly risky for multinationals. In their days as the bogeymen of anti-globalization protesters, they were unpopular because they were powerful. Now, they’re losing influence because they’re weak. Carlos Ghosn, the embodiment of Davos Man, sits under virtual house arrest in Japan, removed from his positions at Renault SA and Nissan Motor Co. and cut loose by the French government. In Vancouver, Huawei’s chief financial officer, Meng Wanzhou, awaits her next extradition hearing. Executives considering travel to Japan, or China – or even, now, Hong Kong – will want to think twice about whether the journey is worth the legal jeopardy.

It’s hard to see this changing soon. President Trump’s mantra of bringing jobs home depends on knitting those fractured supply chains back together, but this time in America. The increasing use of Washington’s Office of Foreign Assets Control to extend U.S. jurisdiction not just to domestic companies, but to any company globally that transacts in dollars, means that every step outside home territory is freighted with risk.

China, too, has been getting less and less dependent on foreign trade for more than a decade, in line with its rising wealth and increasingly state-directed economy. The risk of becoming an “unreliable entity” means companies are increasingly being forced to choose sides between Beijing and Washington.

Multinationals will no doubt survive this. Their first incarnations grew up in an epoch when trade barriers were so high that you often had to set up a plant in a foreign country if you wanted to sell products there at all. Compared with that, times aren’t so hard. But the era of the apolitical global company dedicated only to its bottom line seems increasingly in the past. Henceforth, businesses that don’t want to play politics will increasingly find that politics ends up playing them.

To contact the editor responsible for this story: Matthew Brooker at mbrooker1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

David Fickling is a Bloomberg Opinion columnist covering commodities, as well as industrial and consumer companies. He has been a reporter for Bloomberg News, Dow Jones, the Wall Street Journal, the Financial Times and the Guardian.

©2019 Bloomberg L.P.