Fed Wins Year-End Repo Battle, But War to Control Rates Drags On

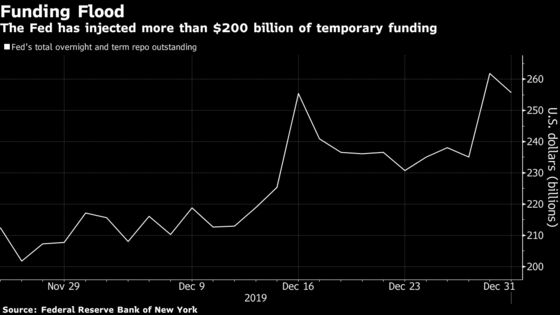

The Fed has provided roughly $230 billion of liquidity for the end of the year to avoid a cash crunch.

(Bloomberg) -- The Federal Reserve may have succeeded in thwarting major year-end turmoil in funding markets, but 2020 is likely to bring a whole new set of concerns.

The U.S. central bank has been injecting liquidity into markets through repurchase-agreement operations since mid-September in a bid to keep control of short-end rates. Earlier this month the Fed ramped up its offerings to help smooth the market’s path into January. It has also been bolstering system reserves through Treasury bill purchases.

The results of the most recent repo actions, which were undersubscribed, suggest that there is now ample funding for the year-end turn. And while the rate on overnight general collateral repurchase agreements was slightly elevated on Tuesday morning, the market is not witnessing the kind of spike seen in September -- when overnight repo rates surged to 10% from around 2%. Whether the Fed can end its interventions without chaos re-emerging, though, is less clear.

“Stopping operations will be difficult since the market is still short of reserves when excluding repo operations,” Gennadiy Goldberg, senior U.S. rates strategist at TD Securities, said Monday. “If the Fed were to pare back liquidity too quickly, they could risk sparking another shortage.”

While the rate on overnight general collateral repo first traded at 1.88%/1.85% on the final day of 2019, it subsequently slipped back to 1.65%/1.45%, based on ICAP pricing. That’s within the target range of 1.50% to 1.75% that the Federal Reserve has in place for the effective fed funds rate, the policy target benchmark. The final overnight operation of 2019, meanwhile, was undersubscribed.

Fed Chairman Jerome Powell said during his press conference following the Dec. 11 Federal Open Market Committee meeting that there would come a time when it’s appropriate for overnight and term repo operations to “gradually decline.” He did not, however, offer any indication as to when that would be and officials have so far said they would conduct the repo operations through January. The release of the minutes from that meeting on Friday could provide more hints as to how policy makers are thinking about removing temporary liquidity from the system.

The Fed has provided roughly $256 billion of liquidity for the end of the year to avoid a cash crunch. The final operation of 2019 saw just $25.6 billion pumped into the system, compared with a maximum available offering of $150 billion.

It plans to conduct another $150 billion overnight action on Jan. 2.

Mark Cabana, head of U.S. interest rates strategy at Bank of America, expects the Fed’s repo offerings to continue beyond January, but reckons officials will adjust the interest rate on operations rather than the size of them, when the time comes.

“If they boost the rate, the dealers will likely naturally decrease reliance on the Fed for funding,” he said Monday. “This is especially true since bill purchases keep adding reserves.”

The New York Fed is expected to announce the next repo operations schedule on Jan. 14. At that point, the central bank could announce “smaller and less frequent” term operations in the second half of the month and first half of February, said Jefferies money-market economist Thomas Simons.

“We would also not be surprised to see them eliminated altogether,” he wrote in a note to clients on Tuesday. [Simons also expects the New York Fed to cut the size of the overnight operations to $75 billion from $120 billion.]

On top of the temporary liquidity that’s been added via repo operations, the Fed has also bolstered permanent reserves by around $157 billion through its bill-purchase program, and that is set to continue at a pace of $60 billion per month until some time in the second quarter at least.

Powell has also said the Fed would be willing to extend its reserve-management purchases of Treasuries to coupon-bearing securities, if needed, although such a move could add fuel to the debate about whether the program can be considered quantitative easing.

TD’s Goldberg said the Fed won’t begin weaning the market off of repo operations until the end of the first quarter or the beginning of the second, once the central bank has had a chance to increase the reserves in the system. Any earlier risks upending the repo market once again.

“The Fed will not want to exit repo operations until they are absolutely certain the market can stand on its own two feet,” he said.

To contact the reporter on this story: Alexandra Harris in New York at aharris48@bloomberg.net

To contact the editors responsible for this story: Benjamin Purvis at bpurvis@bloomberg.net, Nick Baker

©2019 Bloomberg L.P.