Fed to Focus on Next Steps to Save Economy: Decision Day Guide

The Federal Open Market Committee is all but certain to keep its benchmark overnight rate in a target range of 0-.25%.

(Bloomberg) -- With interest rates near zero, Federal Reserve policy makers are likely to turn attention to other steps they could take to ensure a strong U.S. economic rebound once the coronavirus lock-down ends.

The Federal Open Market Committee is all but certain to keep its benchmark overnight rate in a target range of 0-.25%, where it was lowered at an unscheduled FOMC on March 15 to help soften the pandemic’s blow. The committee will release a statement at 2 p.m. with Chairman Jerome Powell holding a press conference 30 minutes later. Forecasts are not scheduled to be released at this meeting.

“Never underestimate the Fed,” said Diane Swonk, chief economist with Grant Thornton in Chicago. “The Fed will affirm it is still willing to use all tools at its disposal.” A Bloomberg survey of economists expects the central bank to keep rates near zero for three or more years.

Facing an unprecedented disruption that has put 26.5 million people out of work in the last five weeks, the Fed has slashed rates and pledged up to $2.3 trillion in loans to aid businesses and state and local governments. Government data released on Wednesday showed the U.S. economy shrank at an annualized 4.8% pace in the first quarter, the steepest decline since 2008.

Powell can expect questions on whether the Fed is prepared to expand the scope of some of its lending programs, provide assistance to specific industries, and is it considering yield-curve targeting, among other topics.

Here’s a preview of what to expect:

Lending Facilities

The Fed has already announced an expansion of its lending to municipalities to include smaller cities and counties than initially planned. Another area that might need support is mortgage servicers, and Powell has previously noted the important role the housing market plays in the economy.

In addition, Treasury Secretary Steven Mnuchin has raised the possibility of extending aid to oil companies struggling with the collapse in the price of oil. But that prospect may face significant hurdles because the central bank is averse to lending to specific industries to avoid picking winners and losers.

Because lending facilities are authorized by the Fed’s board of governors, they could be announced in conjunction with an FOMC meeting or at another time.

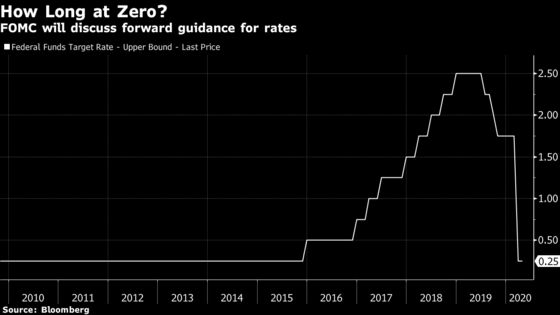

Forward Guidance

Forward guidance for interest rates will be a key issue for the committee. At the last meeting, the FOMC said it would keep rates near zero until the economy weathers the crisis and moves toward meeting the central bank’s full employment and price stability mandates.

“The current forward guidance is confusing,” said Roberto Perli, a former Fed economist and partner at Cornerstone Macro LLC in Washington. “I expect the FOMC to clarify and lean more” in the direction of meeting its mandates, which may mean zero rates for several years.

Some Fed watchers advocate officials adopt specific thresholds to anchor how long they will keep rates near zero, including reprising targets the Fed used back in 2012 to assure investors that there would be no rate hike until unemployment falls to a certain level and inflation rises.

But this meeting may be too soon to provide that level of guidance, which is deliberately designed to stimulate economic activity, given millions of Americans are still sheltering from the virus at home.

What Bloomberg Economists Say

“As consequential as Fed actions have been over the past several weeks, Bloomberg Economics expects the April FOMC meeting to be comparatively quiet with no major policy announcements.”

-- Carl Riccadonna, Yelena Shulyatyeva, Andrew Husby and Eliza Winger

FOMC Statement

The committee will need to adjust its statement to reflect very weak economic data since the last meeting, including record jobless claims, rising unemployment and falling consumption. First-quarter economic growth likely declined by the most since the last recession, according to economists surveyed by Bloomberg.

“I’d expect the opening paragraph to reference the grim employment and consumer spending data that have come out, as well as the unprecedented decline in energy prices and the broader disinflationary forces that are at work,” said Jonathan Wright, economics professor at Johns Hopkins University in Baltimore and a former Fed economist.

Balance Sheet

The FOMC is also certain to discuss its balance sheet expansion with purchases of Treasury notes and mortgage-backed securities during the crisis. It has bought hundreds of billions of dollars of bonds in recent weeks, ballooning its balance sheet to a record $6.57 trillion and declaring on March 23 that its purchases would be open-ended and “in the amounts needed to support smooth market functioning.” But it has more recently been scaling back the buying as market conditions calmed, though it continues to add to its securities holdings.

While the Fed has primarily been buying assets to smooth market functioning, one option would be to explicitly shift to say it was buying securities to try to push longer term rates lower as a financial stimulus measure also known as quantitative easing. That might be an announcement for the months ahead as the economy reopens, rather than this meeting with the lock-down still in place in many parts of the U.S.

Yield Curve Control

Yield curve control -- a cousin of QE -- where the Fed announces it is targeting a specific yield for a specific maturity of Treasury securities, has been discussed by policy makers including Governor Lael Brainard as an option to strengthen the central bank’s forward guidance. At the moment the Fed sets the overnight rate and allows market forces to determine longer-term borrowing costs.

The Bank of Japan began experimenting with yield-curve control in 2016 and currently maintains a target of 0% for the yield on 10-year government bonds, versus a target of -0.1% for its benchmark rate. Advocates say the benefit is a central bank may have to purchase fewer assets overall if it commits to pegging yields at a certain maturity.

Again, it may be too soon for the Fed to announce a decision to adopt such a measure -- but Powell could certainly flag it as a possibility in the future if it comes up during the press conference.

Interest on Reserves

Officials could tweak a secondary rate, known as interest on excess reserves, which helps to keep their benchmark rate in its target range. But that would be a technical move, not a change in policy.

The effective rate -- the average rate paid by U.S. banks when borrowing dollars overnight from other banks -- dipped to 0.04% on April 27 after trading at 0.05% for most of April. The Fed has on multiple occasions adjusted IOER when the effective rate drifted to within 5 basis points of the range’s upper or lower bound.

Press Conference

Powell, in his recent public appearances including on NBC’s “Today” show on March 26, has tried to strike a reassuring posture, noting that while the economy is declining, this is not a typical downturn and he remains hopeful for a robust recovery.

“Powell is unlikely to change his tone much, while reiterating his recent optimism that there’s no reason that the economy can’t quickly recover following the end of the Covid-19 pandemic,” said Tom Garretson, senior portfolio strategist for RBC Wealth Management.

©2020 Bloomberg L.P.