Fed Still on Track for Hike After Jobs Data Deepen 2019 Rate Debate

Despite a slight miss on monthly U.S. payroll data, the Federal Reserve would raise interest rates at its December 18-19 meeting.

(Bloomberg) -- A slight miss on monthly U.S. payroll data hasn’t shifted odds that the Federal Reserve will raise interest rates at its Dec. 18-19 meeting, though the jobs report has made the gathering a lot more interesting.

Investor bets on Friday put the probability of action above 70 percent, according to interest-rate futures. Failing to hike could alarm financial markets that policy makers are more worried about the economy than they’ve let on.

It could also expose Chairman Jerome Powell to accusations he’s caving to President Donald Trump, who has repeatedly complained about rate increases.

But the below-forecast November payroll report, while still showing a healthy labor market, may get some consideration when officials gather later this month. Here are three scenarios for how their deliberations play out.

Scenario 1: Stay the Course

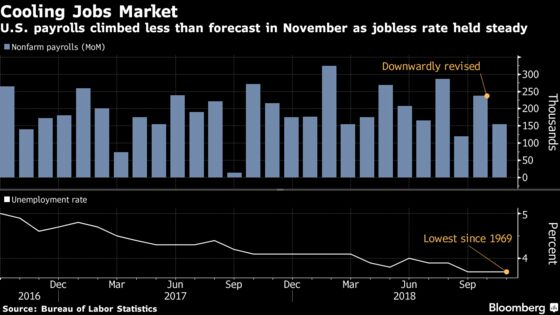

Friday’s jobs report does little to alter the Fed’s outlook. Job gains slowed to 155,000 in November, which is weak relative to the 206,000 average so far this year but well above the number most economists say is needed to keep unemployment steady at a sustainable level.

Policy makers will release a fresh Summary of Economic Projections after their gathering. If economic assumptions hold steady, there would be little reason to dramatically alter the rate path that’s already –- lightly -- penciled in for next year.

Nothing in this payrolls report suggests inflation will take off, and the central bank has been projecting steady price gains around their 2 percent goal. Likewise, the unemployment rate of 3.7 percent has held steady since their last meeting, so they may be able to leave their near-term jobless rate estimates unchanged.

Scenario 2: A Dovish Hike

Fed officials could forge ahead with a rate hike in December and simultaneously rein in expectations for how aggressively they’ll continue raising interest rates thereafter.

“The narrative is now focused on the Fed doing what we know as a ‘dovish tightening,”’ said Carl Tannenbaum, chief economist at Northern Trust Corp. in Chicago. They could do that by “expressing some wonderment over the outlook going forward and wanting to, perhaps, wait a little longer before contemplating their next move.”

That might come in several layers. In their post-meeting statement, officials could drop any reference to “further gradual increases.” They might also massage the language in their assessment of the economy to emphasize that labor growth, while still strong, had begun to wane. And if they’re really feeling dovish, they could declare that risks to their economic outlook -- “roughly balanced” in recent statements -- had tilted to the downside.

If several policy makers, especially in the middle of the pack, drop their forecasts in the SEP for how many rate hikes they foresee in 2019 and 2020, that would send another strong signal.

Finally, Powell can push expectations in any direction he wishes with his post-meeting press conference. Until recently the chairman has talked about an “extraordinary” and “remarkably positive” economy. He could easily pull back on that language and emphasize the Fed is entering a period of policy uncertainty. In the end, if he wishes, Powell could ease financial conditions on the same day the FOMC hikes rates.

Scenario 3: A Surprise Hold

It’s not what investors expect and not what officials have signaled, but the case for a hold in December is one Fed officials could easily defend if that’s how they vote.

Inflation is showing no threat of escalating and is squarely at the Fed’s 2 percent target. What’s more, U.S. central bankers don’t really seem to have an explanation for why it’s not risen more despite decades-low unemployment. That has caught the attention of Vice Chairman Richard Clarida.

“In recent decades, the asymmetry has been toward disinflation forces,” Clarida said in a Bloomberg Television interview Dec. 3. “We are in a world where central banks, including the Fed, are focused on keeping inflation away from disinflation.”

A gauge of inflation calculated by the Dallas Fed, which captures the underlying trend by lopping off outlying contributions to the index, has slowed slightly for three straight months.

A hold would give policy makers more breathing room to assess evolving U.S.-China trade relations and Europe’s economic slowdown, as well as the impact of tighter financial conditions on the economy and what that means for employment.

Standing pat would come with lots of challenges. Investors are already worried about the economic outlook and this could spook them even more. It could look like Powell caved to Trump. And if Fed projections released with the policy statement continue to show more hikes next year, Powell would have to explain in his post-meeting press conference what the trigger is for resumed tightening.

To contact the reporters on this story: Jeanna Smialek in New York at jsmialek1@bloomberg.net;Craig Torres in Washington at ctorres3@bloomberg.net;Christopher Condon in Washington at ccondon4@bloomberg.net

To contact the editors responsible for this story: Brendan Murray at brmurray@bloomberg.net, Alister Bull, Randall Woods

©2018 Bloomberg L.P.