Fed Policy Shift Raises Heat on the ECB

Fed Policy Shift Raises Heat on the ECB

(Bloomberg) -- The European Central Bank is probably a step closer to aiming for periods of inflation above its goal now that the U.S. Federal Reserve has adopted that strategy, according to economists and its former vice president.

The Fed’s new approach, unveiled by Chair Jerome Powell on Thursday, is to seek inflation that averages 2% over time. That would allow it to tolerate a faster pace after periods of weakness, avoiding early interest-rate hikes when price growth moves close to its target.

President Christine Lagarde could find that a tempting option as she resumes an ECB strategy review that was delayed by the pandemic. It would allow her to keep monetary policy looser for longer, worrying less about the hardliners who tend to talk about reining in stimulus even on the rare occasions that inflation has neared the current goal of “below, but close to, 2%.”

“I can’t help but think that the Fed has been setting the tone across major central banks,” said Piet Christiansen, chief strategist at Danske Bank. “I’m sure the ECB would weigh the pros and cons of this measure.”

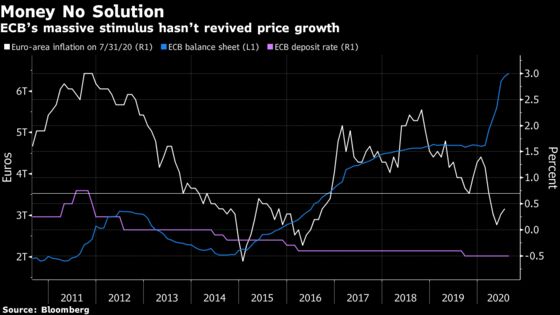

Low inflation has been a longstanding concern for major central banks. The worry is that it morphs into deflation -- a downward spiral of prices and wages that has historically wrecked economies -- during a shock, such as the current pandemic. They’ve responded by pumping trillions of dollars worth of currency into the financial system, with only limited success.

Former ECB Vice President Vitor Constancio is among those saying his prior employer would benefit from so-called average inflation targeting, especially because price stability is its primary mandate. In contrast, the Fed has in the past pointed to full employment as evidence it has met at least part of its dual mandate.

The ECB will soon have the chance to take such a step. It’s conducting its first strategic review since 2003, expected to conclude in the second half of next year. The Fed did a similar evaluation before deciding on its latest change.

Lagarde’s wide-ranging appraisal includes climate change and digitalization, but the reasons for low inflation -- globalization, aging populations and weak productivity -- are at the core.

The key question is whether the current goal itself is part of the problem, by encouraging policy tightening too soon.

It could prove to be a thorny topic. Officials such as Bundesbank President Jens Weidmann, who has frequently opposed looser ECB policies, and Austrian Governor Robert Holzmann, who’s suggested a lower inflation target, may have to be persuaded of any shift that allows price gains above 2%.

Bank of France Governor Francois Villeroy de Galhau, who has previously endorsed a look at average inflation targeting, declined to speculate much when he spoke at an event hours after Powell’s announcement.

“I won’t anticipate the result, but you can be reassured that a credible and symmetrical inflation objective will remain at the heart of our action,” he said.

Read more...

|

A change might also be a hard sell publicly. Years of extraordinary monetary stimulus has stoked criticism, with politicians in some countries regularly lambasting the ECB for the impact on savers. Its deposit rate has been below zero for six years.

“The Fed saying this is different from the ECB saying it, because the Fed had actually hiked rates several times,” said Rishi Mishra, an analyst at Futures First. “So they can say ‘hey, we might have been too hawkish last time around. This time, we would wait longer.’ What would the ECB say? ‘Hey, we have been waiting forever, and would continue to wait forever?’”

Economists and strategists including Carsten Brzeski at ING Groep NV and Frederik Ducrozet at Pictet & Cie reckon the ECB will change its goal, but that it won’t follow the Fed entirely, in part because of skepticism on the Governing Council.

More likely, it’ll settle on a so-called “symmetric” goal of 2% with flexibility, they say. In practice, that means it’ll tighten policy when inflation is above that rate, and loosen when it’s below, but won’t rush too quickly to do so.

“There won’t be a majority at the Governing Council to simply copy the Fed’s move,” said Brzeski. “In the euro zone, the concept of average inflation targeting has been more controversial.”

©2020 Bloomberg L.P.