Fed Shadow Rate at 5.45% Shows Stock Rout Justified: SocGen

Fed Shadow Rate at 5.45% Shows Stock Rout Justified, SocGen Says

(Bloomberg) -- The worst monthly sell-off in stocks since the global financial crisis was justified given that the Federal Reserve has tightened overall monetary policy more than in past episodes, according to Societe Generale SA.

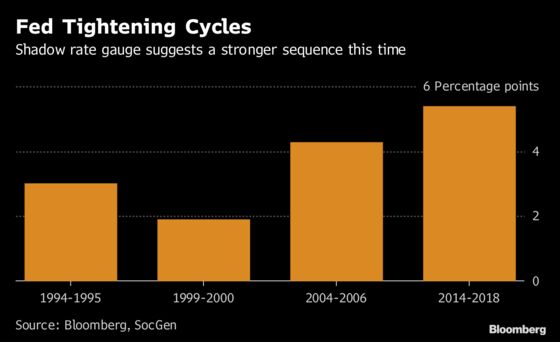

While the Fed’s policy target at a range of 2.25 to 2.5 percent is less than half its pre-crisis level, the true magnitude of tightening needs to account for the withdrawal of quantitative easing. That’s according to a concept called the shadow rate, which incorporates an estimated 3 percentage points of implicit rate hikes from 2014 until 2015 -- between the end of the Fed’s bond-purchase program and the start of boosting the benchmark interest rate proper.

“The recent market turbulence is well justified in the context of an approaching tightening peak,” Solomon Tadesse, a Societe Generale equity quant analyst in New York, wrote in an emailed response to questions. “After the December rate hike, the current implicit effective fed rate (reflecting the shadow short rate) stands at around 5.45 percent.”

Looking at it another way, the current tightening cycle relative to the prior easing cycle is now right at the average, considering Fed history from 1984 to 2007, Societe Generale calculates. Tadesse and colleague Andrew Lapthorne last May had judged that point would be the “best forecast” for when the Fed stopped raising rates.

“We are at the very peak of this tightening cycle” in wake of the Fed’s December hike, Tadesse said. “The height of tightening (accompanying the end of a business cycle) signifies maximum monetary-policy brake, signaling upcoming economic downturns,” he added.

While many Fed forecasters do see further rate hikes this year, projections have been cut in the wake of the stock slump last quarter, and after repeated messages from policy makers that they are prepared to be patient on any further moves.

Societe Generale quant strategists have favored positioning in value stocks in preparation for tougher times, saying Jan. 14 that earnings estimates could go “double-digit down” if there’s a real global economic slowdown.

Though the Fed continues to shrink its bond portfolio by up to $50 billion a month, Tadesse said the continuing quantitative tightening isn’t pushing up the shadow rate further, suggesting that a pause in boosting the target federal funds rate would be enough to bring policy moves to a halt. The 3 percentage points in shadow rate rises earlier this decade already reflected expectations for some liquidity “drainage” via QT, he said.

Only if the Fed continued QT beyond current market expectations would there be an impact, he said. Analysts have had varying views on the effect that QT is having on markets, with a Morgan Stanley model showing every $20 billion shift in bond holdings equaling a 0.37 percent change in stock prices, and Barclays Plc concluding the connection with equity declines is “weak.”

--With assistance from Eric Lam.

To contact the reporter on this story: Christopher Anstey in Tokyo at canstey@bloomberg.net

To contact the editors responsible for this story: Christopher Anstey at canstey@bloomberg.net, Joanna Ossinger, Ravil Shirodkar

©2019 Bloomberg L.P.