Fed’s Tone Will Give Clues on 2019 Pace: Decision-Day Guide

The FOMC is widely expected to keep the benchmark target for rates unchanged in a 2 percent to 2.25 percent range.

(Bloomberg) -- Federal Reserve policy makers meeting in Washington will weigh how to describe a moderation in U.S. economic growth as they reinforce expectations for a fourth 2018 hike next month.

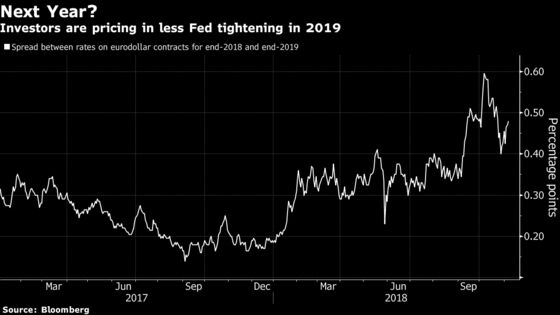

The Federal Open Market Committee is widely expected to keep the benchmark target for rates unchanged in a 2 percent to 2.25 percent range at the conclusion of its two-day meeting on Thursday. Its policy statement, released at 2 p.m., will likely continue to describe U.S. growth and the labor market as strong, reinforcing the outlook for a hike in December. Other tweaks in the statement could suggest less confidence in the need to raise rates three times next year, as officials projected in September.

No press conference with Chairman Jerome Powell is scheduled after this meeting and economic forecasts won’t be updated until December, when pricing in interest rate futures show investors see a roughly 78 percent chance the Fed will hike again.

“December is pretty well baked in, but more important is the tone that is set as we look toward 2019,” said Lindsey Piegza, chief economist at Stifel Nicolaus & Co. in Chicago. “I will be looking for any kind of change in tone that suggests that the economy is not moving ahead on full cylinders.”

The guidance in the statement on more gradual rate hikes -- as well as the characterization of risks to the outlook as “roughly balanced” -- are likely to remain unchanged. New Fed Vice Chair Richard Clarida, in a speech Oct. 25, tweaked that guidance to call for “some further gradual” hikes -- adding the word “some.” Making that change, which is seen as unlikely, would be dovish and suggest the central bank is closer to the end of the rate cycle.

Also unlikely to change is the language on inflation. For the first time since the central bank introduced its 2 percent inflation objective in 2012, both the headline and core measures of year-on-year price pressures hit the FOMC’s goal of 2 percent in September. With U.S. unemployment at a 48-year low of 3.7 percent, officials may welcome some moderation in growth. The Fed has upgraded its economic forecasts this year and some policy makers have voiced worry about overheating, though inflation has remained well behaved.

“Most if not all of the changes in the statement will be in the first paragraph” summing up recent conditions, said Roberto Perli, a partner at Cornerstone Macro LLC in Washington and a former Fed economist. “They might say that economic activity has moderated a bit but remains strong or solid.”

Market Woes

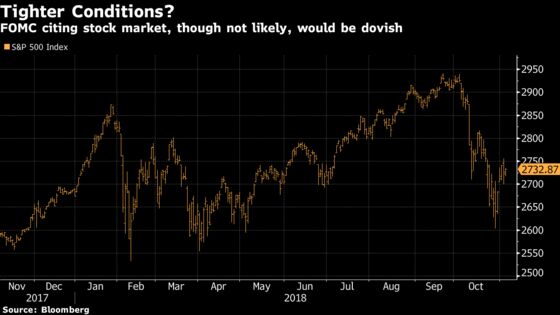

One cloud is the stock market, which has fallen 3.2 percent since the last FOMC meeting in September, while U.S. Treasury yields have risen. As a result, the Fed could mention “tighter financial conditions” in the statement. The housing market has also showed some weakness as mortgage rates have risen.

However, most Fed officials have brushed off the importance of lower equity prices, viewing the decline as normal volatility as opposed to a signal about the outlook. They have also welcomed higher long-term yields as evidence of economic health. Any mention of stocks or housing would be viewed as a dovish signal, suggesting the FOMC is concerned about those developments.

“Over the last two years, the stock market has only gone in one direction and it’s been up,” Atlanta Fed President Raphael Bostic said last month amid the turmoil. “As you know, the stock market can be extremely volatile.”

One line the FOMC might be required to change is that business fixed investment has “grown strongly,” in light of weakness last quarter. That might reinforce the view of the FOMC that $1.5 trillion in tax cuts signed by President Donald Trump have mainly delivered a one-time stimulus to U.S. businesses, as opposed to fostering a lasting increase in investment.

“It suggests that growth from the fiscal stimulus is mostly a standard Keynesian surge in consumption and government spending, without much growth in investment,” said Jonathan Wright, an economics professor at Johns Hopkins University in Baltimore and a former Fed economist. “It could be interpreted as hawkish” since investment that enhanced productivity could permit faster growth without inflation.

What Our Economists Say“Fed officials will be satisfied if the November FOMC meeting is a relative non-event for financial markets. Policy makers will keep interest rates unchanged and will probably leave signaling about a December hike to communications following the meeting. Officials may adjust language from the previous statement describing business fixed investment as having ‘grown strongly’ in light of evidence to the contrary in the latest GDP results. However, they will retain a generally favorable tone toward the outlook for the economy and inflation.”-- Carl Riccadonna, Yelena Shulyatyeva and Tim Mahedy, Bloomberg Economics |

IOER

One change that probably will be discussed during the meeting: A technical adjustment to the interest rate the Fed pays on excess bank reserves, or IOER. In June, they opted to raise it by 5 basis points less than the overall target range. That gap between the two rates was maintained when the Fed tightened in September, taking IOER to 2.20 percent and the top of the range to 2.25 percent.

Since then, the effective funds rate has risen to trade in line with the IOER rate for almost every day for the past couple of weeks, stirring talk that officials might adjust the reserves rate down by another five basis points at this meeting.

Still, it could wrong-foot investors if the Fed announced it was holding the benchmark target range for the federal funds rate unchanged on Thursday, while at the same time making a technical adjustment to IOER that effectively cuts rates in money markets. For that reason and to avoid confusion, it may prefer waiting until December to make the change to IOER, when it it actually raises its main policy target, said Deutsche Bank Securities economist Brett Ryan.

No Politics

The Fed won’t mention the Nov. 6 U.S. midterm congressional elections, as it’s careful to safeguard its political independence, even if the president has not shied away from criticizing its rate increases in recent months. The FOMC meeting began on Wednesday, a day later than usual, to allow staff to vote in the election.

To contact the reporter on this story: Steve Matthews in Atlanta at smatthews@bloomberg.net

To contact the editors responsible for this story: Alister Bull at abull7@bloomberg.net, Randall Woods

©2018 Bloomberg L.P.