Fed’s Policymaking Panel Tilts Even More Dovish in 2021 Rotation

Changes to the Fed’s rate setting panel will make the central bank even less likely to tighten monetary policy in the new year.

(Bloomberg) -- Changes to the Federal Reserve’s interest-rate setting panel will make the U.S. central bank even less likely to tighten monetary policy in the new year, no matter how much of a jolt the economy gets from the rollout of Covid-19 vaccines.

In the annual rotation of voters on the Federal Open Market Committee, the four regional Fed presidents who receive that privilege in 2021 will be marginally more dovish -- or inclined to favor easy policy -- than the four they replace. The most notable shift comes as Chicago’s Charles Evans, one of the most predictably dovish officials, takes the vote held this year by Cleveland’s Loretta Mester, a relatively hawkish figure on the panel.

In addition, a new permanent vote now belongs to Christopher Waller, the former research director of the St. Louis Fed who was sworn in as a member of the Fed’s Board of Governors on Dec. 18. In one important respect Waller is decidedly dovish: He has long championed the view, more recently embraced by the Fed’s leadership, that low unemployment doesn’t automatically generate higher inflation.

“If vaccines take hold, the prospect of rate hikes might get a little closer than it feels like today,” said Stephen Stanley, chief economist at Amherst Pierpont Securities. “But they’re still not likely to be moving rates in 2021.”

| New 2021 Voters | Replaces |

|---|---|

| Charles Evans, Chicago | Loretta Mester, Cleveland |

| Thomas Barkin, Richmond | Patrick Harker, Philadelphia |

| Raphael Bostic, Atlanta | Robert Kaplan, Dallas |

| Mary Daly, San Francisco | Neel Kashkari, Minneapolis |

| Christopher Waller, Board of Governors | Board vacancy |

It’s hard to overstate how intent the FOMC is on keeping policy easy well into this economic recovery. For reasons that have nothing to do with Covid-19 and everything to do with longer-term trends in inflation and growth, Fed officials -- led by Chair Jerome Powell -- this year adopted a new monetary policy framework that commits them to a more patient approach to raising rates than at any other time since the early 1970s.

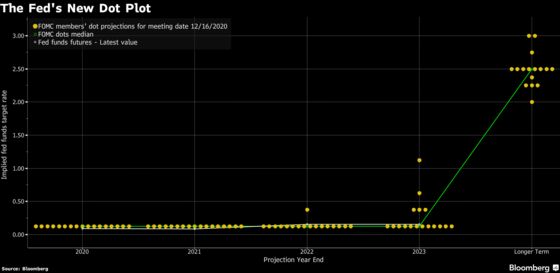

The committee has backed that up in two ways. Its members have declared they won’t hike before the labor market has reached their estimate of maximum employment and inflation is on its way to exceeding their 2% target. They also submitted economic projections in December showing 12 of 17 FOMC members didn’t expect a single rate hike until at least 2024.

“We are in very unusual circumstances in which the Fed, as a group, has taken a turn that is much more dovish than any time prior,” said Gregory Daco, chief U.S. economist with Oxford Economics.

Still, the changes on the FOMC this year could influence the fine-tuning delivered by the Fed’s asset-purchasing program. The bank is currently buying $120 billion a month worth of Treasuries and mortgage-back bonds in an effort to suppress longer-term borrowing costs for households and businesses. An unexpected negative turn for the economy could lead to calls to ramp up those purchases.

Bloomberg Economics 2021 Fed Spectrometer

But with vaccines being distributed and a new $900 billion stimulus package just passed by Congress and signed into law by President Donald Trump, the economy may be poised for a robust rebound in the second half of 2021. That makes it more likely the Fed comes under pressure to taper its bond purchases.

“Attitudes toward asset purchases might vary even among the group that is extremely dovish,” Stanley said. “So, I do think the change in composition matters in that sense, at least at the margin.”

Two other factors that could play a role: inflation and financial stability. On the first, inflation is on track to show a sharp year-on-year increase come spring, based purely on price drops triggered by the pandemic last March and April. A burst in economic activity could push that higher, leading to a debate over whether price gains might persist.

Powell has already signaled he’d view sharp price increases in 2021 as “transient.” And the more dovish makeup of the committee, in that scenario, makes it less likely that he’d provoke votes of dissent at Fed policy meetings by ignoring inflation.

But there could also be new concerns over financial stability if a brightening outlook and super-low rates cause corporations to go on another debt binge and financial markets to react giddily.

“As we shift gears from a delicate phase to one that’s more likely to see an acceleration in the pace of the recovery, the Fed’s attention will also have to shift and pay closer to attention to these financial stability concerns,” Oxford Economics’s Daco said.

©2020 Bloomberg L.P.