Fed's Mester Says an Interest-Rate Cut Would Be ‘Bad Policy’

Fed's Mester Says an Interest-Rate Cut Would Be ‘Bad Policy’

(Bloomberg) -- For Loretta Mester, returning inflation to the U.S. central bank’s 2% target requires restraint more than drastic action.

In an interview with Bloomberg News, the president of the Federal Reserve Bank of Cleveland dismissed the notion that policy makers should cut interest rates to raise inflation. Instead, officials should simply be careful not to react too quickly when prices move back up again, as she expects them to later this year.

“If you really wanted to get inflation expectations moving up you’d have to take really aggressive action -- if that was your only goal,” Mester said. “But that would be bad policy because we have another goal and the risk you’d be running on the other goal would be excessive,” she added, referring to Fed’s employment mandate.

“Since we’re not far from our goal, I’d rather do something that is more prudent, which is be willing to keep interest rates low,” said Mester, who’s viewed as modestly hawkish on inflation, in an interview conducted Wednesday.

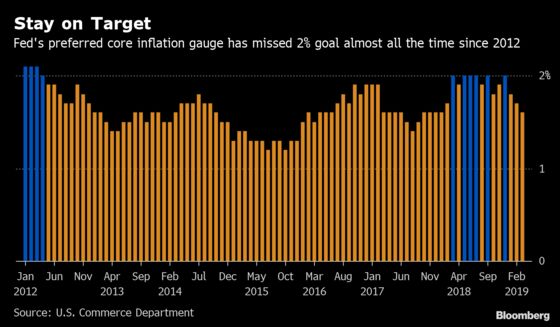

The Fed’s favorite measure of price gains has for years run consistently below the 2% objective, raising worries that below-target results would become ingrained in the public’s expectations for inflation. That’s why the Fed is undertaking a broad review this year of its policy framework, including its inflation-targeting strategy.

Against that background, price gains minus food and energy took a surprising dip in the first quarter, falling to 1.6% in the year through March. That raised speculation among investors that the Fed might cut rates this year to combat the decline even though unemployment has hit a 49-year low at 3.6% -- well below the level at which Fed officials think it should provoke higher inflation.

If inflation were continuing to move down and demand in the economy were declining, that might call for a response, Mester said. Absent that, policy makers should be “opportunistic” in allowing inflation to rise, whether that happens through wage pressures or unexpected shocks.

“Let’s hold rates where they are and be more willing to do that even though we have a very low unemployment rate,” she said.

Mester made clear she’d be equally unconcerned by an overshoot of the target if that was not expected to persist.

“Suppose we get some readings on inflation that are above 2%,” she said. “I’d feel the same way. We really don’t have to respond to that.”

Opportunistic Disinflation

Mester’s thinking represented, she said, something of a mirror to an approach popularized by Fed Governor Laurence Meyer in the 1990s that he termed “opportunistic disinflation.” It proposed that central banks should sometimes hold rates steady while allowing a slowing economy to ratchet down inflation. In the reverse, it might counsel holding rates steady to allow an expanding economy to lift inflation.

On trade, Mester acknowledged that uncertainty over deteriorating U.S.-China relations was weighing on companies in her district, which includes Ohio, western Pennsylvania and eastern Kentucky. But, she added, tariffs were not their biggest worry.

“They can’t find workers, they have increased wages and will probably have to do that more if they can’t continue to get workers,” she said. “That’s their number one focus. It’s not on tariffs or that demand is falling off. They say demand is good.”

Trade War

Even with tariffs on goods imported from China bumping up to 25%, “the actual direct impact even in our district is not that large in terms of both prices and GDP growth,” she said.

On the Fed’s ongoing review of its inflation-targeting strategy, Mester sounded skeptical that any fundamental change was necessary. Some economists have proposed a so-called inflation make-up strategy, so any persistent undershoot of inflation would be followed by a deliberate overshoot to keep expectations for inflation anchored around their target. Currently, the Fed seeks to move inflation toward 2% without respect to past misses.

The new proposals work very well in economic models, Mester said, but may be hard to pull off in real life. And if a new strategy failed to work, that would damage the Fed’s credibility.

“We have a framework that we’ve articulated,” she said. “To actually say we’re going to change the framework now, you’d better be able to deliver on it.”

To contact the reporter on this story: Christopher Condon in Washington at ccondon4@bloomberg.net

To contact the editors responsible for this story: Margaret Collins at mcollins45@bloomberg.net, Alister Bull, Sarah McGregor

©2019 Bloomberg L.P.