Fed’s Jumbled Talk Leaves Balance-Sheet Message in ‘Disarray’

The Federal Reserve’s best laid plan for a below-the-radar rundown of its $4.1 trillion balance sheet has gone awry.

(Bloomberg) -- The Federal Reserve’s best laid plan for a below-the-radar rundown of its $4.1 trillion balance sheet has gone awry.

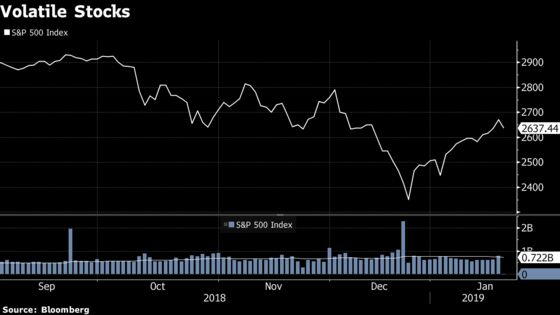

Rather than operating in the background as policy makers intended, the strategy has been thrust into the spotlight as investors and President Donald Trump have attacked it for fueling last month’s stock market sell-off.

“The sudden and unwanted attention that market participants attached to balance sheet policy has thrown the Fed’s communications on the topic into disarray,” JPMorgan Chase & Co. Chief U.S. Economist Michael Feroli said in a recent note.

The risk is that could lead to renewed market turmoil as investors try to parse the Fed’s plan for a draw-down that some consider more significant than policy makers do.

Chairman Jerome Powell will get a chance to explain the approach when he briefs reporters Jan. 30 after a two-day Federal Open Market Committee meeting in Washington. No change is expected in its strategy of reducing its bond holdings by a monthly maximum of $50 billion. Interest rates are also seen being left on hold.

It’s not only Wall Street that’s wrong footed the Fed. Washington has too.

Republican lawmakers’ criticism of the bloated balance sheet as inflationary has been drowned out by Trump’s attacks on the Fed’s move to reduce it when price pressures are muted.

“Trump has done an extraordinary job of articulating” the market’s unease with Fed policy at key points, said PGIM Fixed Income Chief Economist Nathan Sheets.

U.S. central bankers have already re-crafted their message about the unwind of quantitative easing in response to December’s stock slump.

No longer do they say the reduction is on autopilot. Instead, they assure that policy isn’t on a preset course and that they’re prepared to alter balance sheet plans if necessary to keep the economy on track.

The trouble is that the new formulation leaves much unsaid and could sow more uncertainty.

“Fed officials’ attempts to calm market panic over ‘quantitative tightening’ create further risk for confusion,” TD Securities Head of Global Macro Strategy Michael Hanson said in a note.

The chances of that happening are heightened by disagreement between the Fed and market pros like billionaire investor Stanley Druckenmiller over how consequential the unwind is. Central bankers just don’t buy the argument it sparked the fourth quarter stock sell-off.

“We don’t believe that our issuance is an important part of the story of the market turbulence,” Powell said Jan. 4. He instead pointed to investor concerns about slowing global growth and U.S.-China trade negotiations.

The FOMC is holding in-depth discussions on the balance sheet that Vice Chairman Richard Clarida said will reach important decisions this year.

But those conversations have centered on what Hanson called “micro” issues, such as what operating framework the Fed should use in managing short-term rates, and not on the monetary policy implications of the unwind.

Hanson said that raises the risk that a halt to Fed portfolio paring could be mistaken by markets as something it’s not: a fundamental shift in the monetary stance.

What Our Strategists Say |

|---|

| Balance sheet runoff will continue even if the Fed doesn’t continue increasing the federal funds target rate. They think a further $600 billion of runoff is possible before bank reserves start to become scarce. By their estimates, this would occur in mid-2020. Should the Fed end runoff, we think they will reinvest mortgage-backed security paydowns into Treasuries as the Fed seems keen to slowly go back to a Treasury-only portfolio. --Ira Jersey, Bloomberg Intelligence U.S. Interest Rate Strategist |

Morgan Stanley Chief U.S. Economist Ellen Zentner and her team forecast the balance sheet rundown will end in September.

Powell, though, recently suggested otherwise. The future balance sheet “will be substantially smaller than it is now,” he said on Jan. 10, sparking a brief drop in shares.

To avoid misconceptions about its strategy, the Fed in 2014 put out what it called its “policy normalization principles and plans.” Indeed, Powell cited the initial principles on Jan. 4 when he said the Fed was ready to change its strategy if needed to meet its goals.

But he failed to mention an augmentation of the plans agreed in 2017. It stated the Fed would be ready to stop cutting its bond holdings “if a material deterioration in the economic outlook were to warrant a sizable reduction” in short-term rates.

That wording itself was confusing. It suggested the Fed “could be putting one foot on the brake and the other on the accelerator” when it starts cutting rates, said Ethan Harris, head of global economics research at Bank of America Merrill Lynch.

The balance sheet divide between the Fed and markets dates back to quantitative easing’s 2008 start.

Taper Tantrum

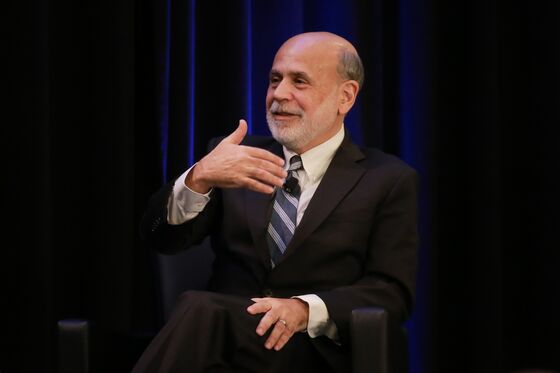

Then-Chairman Ben Bernanke tried to name the Fed’s big bond purchases “credit easing” to focus attention on the impact they’d have on long-term rates. Investors insisted on the term quantitative easing.

Today, Fed officials are still focused on bond yields, arguing their low levels suggest the balance sheet run-off is not as frightening as feared.

Some investors though maintain that a shift to quantitative tightening by global central banks last fall fueled the stock slump.

This isn’t the first time confusion over balance sheet strategy has sparked turmoil. In May 2013, Bernanke triggered the “taper tantrum” when he hinted bond buying might soon stop.

Then-Governor Powell said it was up to Bernanke to clarify the message in a press conference after the FOMC’s June 2013 meeting.

“It’s appropriate to give LeBron the ball at the end of the game,” he said, referring to basketball great LeBron James, according to transcripts.

Powell now has to play the role of closer at next week’s post-meeting press conference.

To contact the reporter on this story: Rich Miller in Washington at rmiller28@bloomberg.net

To contact the editors responsible for this story: Brendan Murray at brmurray@bloomberg.net, Alister Bull, Jeff Kearns

©2019 Bloomberg L.P.