Fed’s New Plan to Lift Inflation Faces Skepticism

Federal Reserve’s new plan to run the economy hot looks easier said than done, say economists

(Bloomberg) -- The Federal Reserve’s new plan to run the economy hot looks easier said than done as the central bank confronts multiple forces holding down inflation.

“The Fed needs to articulate very clearly how they plan to achieve the new objective,” Aneta Markowska, chief economist at Jefferies, wrote in a report to clients. “Otherwise, these are just words on paper that don’t really mean anything.”

Chair Jerome Powell Thursday outlined a new approach to setting U.S. monetary policy. The Fed, he said, will sometimes allow inflation to run above the 2% target to make up for prior undershoots, and allow unemployment to run lower than officials had previously tolerated.

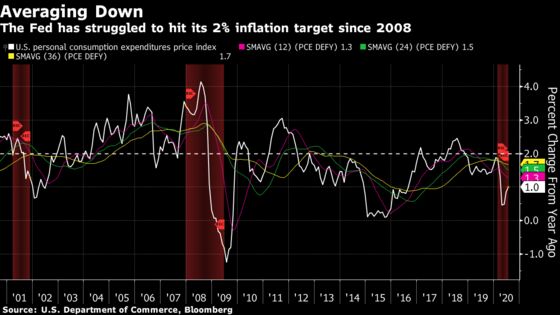

The move confirmed to investors that the Fed is likely keep interest rates near zero for years to come as it seeks to decisively achieve its inflation goal, adopted in 2012. Inflation has averaged only 1.4% since then amid headwinds affecting the U.S. and other major economies, including weak productivity growth, globalization, aging populations and technological change.

Fed policy makers meet again Sept. 15-16 when they’ll have a chance to spell out how the new strategy will shape their policies aimed at pulling the U.S. economy out of its worst downturn since the Great Depression.

Economists at Deutsche Bank AG said officials may clarify their guidance on the path of rates by linking future hikes to reaching certain thresholds for inflation and employment. Minutes of their July meeting showed they’d debated this approach.

Powell’s announcement, though not entirely unexpected, marked the completion of a historic shift for the world’s most powerful central bank. Instead of worrying that very low unemployment would provoke inflation, they now have moved their focus almost fully onto too-low inflation.

To justify that, he made a point of explaining why persistently low inflation is a problem for central bankers, particularly when combined with low economic growth. It results in very low interest rates, even during economic expansions. That means policy makers have little room to cut borrowing costs when a downturn strikes.

“The result can be worse economic outcomes in terms of both employment and price stability, with the costs of such outcomes likely falling hardest on those least able to bear them,” Powell said.

On the other side of the argument, there’s a camp of investors convinced that the Fed’s ultra-easy monetary policy and massive government spending risk re-igniting the runaway inflation of the 1970s.

Still, many observers viewed the Fed’s ability to lift inflation with skepticism, especially considering that much of the world has just tumbled into a new recession -- caused by the coronavrus pandemic -- that’s stifled demand and sent U.S. unemployment north of 10%. Both of those factors conspire to put more downward pressure on inflation.

The Fed may also be hindered in delivering if Congress doesn’t provide additional significant fiscal support. Lawmakers have approved $3 trillion of aid for workers, struggling businesses and the overall economy. But they have failed to reach an agreement on a new package even as provisions of the previous round expired.

What Bloomberg Economics Says...

“This approach de-emphasizes previous concerns that low unemployment can lead to excess inflation. It means the first increase in interest rates may not come into view for many years.”

-- Yelena Shulyatyeva and Eliza Winger

Click here for the full report

“It is doubtful that they can achieve overshoots of inflation anytime soon, and it is mostly out of their hands, in my view, whether or not they will get it even in the medium term,” Adam Posen, president of the Peterson Institute for International Economics, told reporters following Powell’s speech.

Ryan Sweet, head of monetary policy research at Moody’s Analytics, sounded equally doubtful, and not only because of the pandemic.

“The Fed can say they want inflation to overshoot, but that doesn’t mean it will occur,” he said “Demographics and technology will be pushing against inflation.”

Other economists noted that Powell was silent on precisely what will make inflation move above the 2% goal. Unemployment hit 3.5%, a half-century low, in 2019, and still inflation, measured by the Fed’s favorite gauge, never topped 1.6% that year.

“What is not obvious is exactly how the Fed intends to achieve a persistently higher inflation rate” other than promising to use the same tools the Fed employed in the last downturn, Roberto Perli, a former Fed economist and now partner at Cornerstone Macro wrote in a note to clients.

“Those tools took us out of the Great Recession but did not generate inflation,” Perli wrote. “It is possible that the Fed intends to use those tools in stronger doses, but even so there is reason to believe that the power of those tools may be lower today that it was years ago.”

In its framework review, Fed officials rejected, at least for now, alternative tools that other central banks have used, including negative interest rates and capping the yields of certain government bonds.

James Bullard, president of the St. Louis Fed, offered a defense of the new strategy and its potential for success in an interview Thursday on Bloomberg Radio with Michael McKee. He said the approach could help raise inflation expectations among investors, a factor economists believe heavily influences inflation outcomes.

“There was a perception both in markets, and perhaps in the policy making community as well, that 2% inflation was some kind of a ceiling,” he said. “Inflation expectations should be moved up a little bit now in markets in response to this.”

Indeed, market-based measures of inflation expectations ticked up again following Powell’s speech. The so-called break-even rate derived from five-year Treasuries, which had already been rising in anticipation of the Fed’s shift, nudged up to 1.70% from 1.66% Thursday.

Powell sounded a bit more cautious in projecting the results.

“It’s a very promising set of changes to deal with what is the reality of a quite difficult macroeconomic context,” he said in a question-and-answer session following his speech. “Time will tell, and our actions will ultimately tell.”

©2020 Bloomberg L.P.