The Fed's IOER Experiment May Already Be Reaching Its Limits

As Fed’s IOER and overnight reverse repo rates compress, it’s likely to drive massive flows in and out of money-market instruments

(Bloomberg) -- The Federal Reserve’s latest strategy to control its key interest rate may already be reaching its limits.

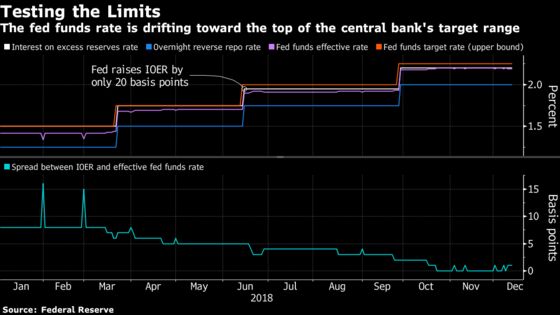

Officials are widely predicted to lift their main target range Wednesday, with a slight twist. The Fed is expected to increase one of the rates it uses to help guide the top of the policy band by a bit less, echoing a similar action taken in June. It’s part of an effort to keep in check the rising fed effective rate. The benchmark has been drifting toward the upper end of the main range for much of 2018 as a combination of surging Treasury-bill supply and the central bank’s balance-sheet unwind have driven U.S. money-market rates higher.

Yet the Fed’s willingness to keep tweaking the so-called interest on excess reserves rate could start to have major implications for everything from banks’ ability to meet their liquidity coverage ratios, to the signaling role of markets, to the future of the central bank’s policy-setting mechanism. Additional moves beyond the one expected this week would bring IOER below the midpoint of the Fed’s target range, toward the critical overnight reverse-repo rate that now guides its floor, putting America’s monetary-policy framework to the test.

“The Fed has to figure out what their constraints are and there’s not a lot of information about that, unfortunately,” said Gennadiy Goldberg, a senior U.S. rates strategist at TD Securities. “We’re having this debate on our desk right now.”

It’s not a given that further adjustments to the interest on excess reserves rate will be necessary in 2019. Yet the evidence so far suggests that the downward pressure on the effective fed funds rate from IOER tweaks may only be temporary.

In June, as fed funds got to within five basis points of the central bank’s upper bound, officials took the unprecedented step of raising IOER by only 20 basis points, while hiking their target rate by 25. While initially successful at pushing the effective rate closer to the midpoint of Fed’s target band, it has since continued to creep higher. At 2.20 percent, it’s once again approaching the top of the current 2 - 2.25 percent target range.

So far, the Fed has shown few reservations about making further tweaks to the rate it pays on excess reserves. In September, Chairman Jerome Powell said the rising fed effective rate is “a problem we can address with our tools, and we’ll use them if we have to.”

Yet market participants are starting to see downsides to the central bank’s current strategy.

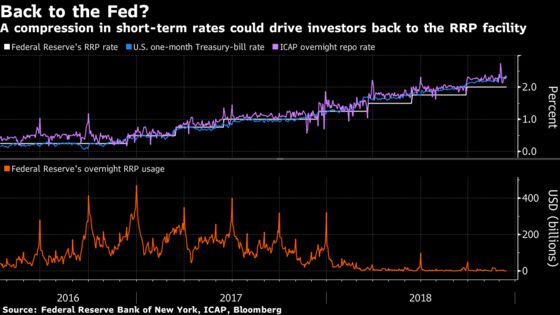

As the Fed’s IOER and overnight reverse repo rates compress, it’s likely to drive massive flows into and out of various money-market instruments and the RRP facility, depending on which offer higher yields on a given day, according to Michael Cloherty at RBC Capital Markets in New York.

When there are swings in the usage of the reverse repo facility, it creates a dollar-for-dollar change in reserve levels, which could ultimately stress the ability of banks to source overnight liquidity and meet their coverage ratios, especially as the Fed continues to shrink its balance sheet, said Cloherty, RBC’s head of U.S. interest-rate strategy.

Funding markets would likely remain stable should the Fed keep the gap between the IOER and RRP rates at 15 basis points or more, where it will likely stand after Wednesday’s expected policy tweak. Any tighter than that, however, and volatility is likely to increase, he said. At its extreme, it could spur intraday movements of “many hundreds of basis points, with extreme whippiness.”

Signaling Role

Uncertainty surrounding the likelihood, size and timing of potential IOER tweaks is also forcing interest-rate traders to position for a wider array of outcomes in the run-up to policy meetings. That’s distorting the critical signaling role markets provide in relation to Fed rate-hike expectations.

“One question we have received with increasing frequency is about the discrepancies around the probabilities assigned to a rate hike at the December Fed meeting,” BMO Capital Markets strategists Ben Jeffery and Jon Hill wrote in a note to clients this month. “Whether one assumes that the FOMC will execute another technical adjustment to IOER influences market implied probabilities.”

While tweaks have so far been well telegraphed and timed to align with policy hikes, 2019 holds the potential for more IOER ambiguity. With traders dramatically paring expectations for interest-rate increases next year, the possibility of straight IOER cuts absent any policy tightening has to increasingly be considered, and priced in. What’s more, officials have already discussed the prospect of off-meeting moves as well.

“From an expectations point-of-view, I’m a simple guy, I take the effective” instead of IOER, said Todd Colvin, senior vice president at futures and options broker Ambrosino Brothers in Chicago. “But when the Fed fudges with IOER it does put a little bit of a twist on it.”

Toolkit Questions

The more officials adjust the excess reserves rate, the louder questions about the Fed’s policy-implementation framework are likely to become.

The Fed will need to start considering changes to the RRP rate to coincide with any additional tweaks to IOER following this week’s anticipated move, Wrightson ICAP economist Lou Crandall wrote in a note Monday.

Ward McCarthy, chief financial economist for Jefferies LLC, expects the Fed to continue adjusting IOER until it reaches the lower bound. It’s part of an effort to incentivize commercial banks to increase overnight lending in the fed funds market, he said in an interview last week, a lack of which is likely at least partly to blame for the upward pressure on the fed effective rate.

Policy makers have also ramped up discussions over potentially replacing fed funds altogether as the central bank’s policy benchmark of choice. Those deliberations may accelerate should officials find the efficacy of further IOER tweaks limited, or the unintended consequences too great.

“It feels like they’re tearing up the playbook and they need to come up with a new one,” said Mark Cabana, head of U.S. interest rates strategy at Bank of America Corp. “They need to make some really important decisions and they need to explain why they’re doing it.”

--With assistance from Liz Capo McCormick.

To contact the reporter on this story: Alexandra Harris in New York at aharris48@bloomberg.net

To contact the editors responsible for this story: Benjamin Purvis at bpurvis@bloomberg.net, Boris Korby, Mark Tannenbaum

©2018 Bloomberg L.P.