Fed’s Clarida Leaves Door Open to Yield Caps in New Strategy

Fed’s Clarida Leaves Door Open to Yield Caps Under New Framework

(Bloomberg) -- Federal Reserve Vice Chair Richard Clarida left open the possibility of employing Treasury yield caps at some point in the future, though he indicated it’s not likely now and reiterated the central bank’s rejection of negative interest rates.

“Yield caps and targets were not warranted in the current environment but should remain an option that the committee could reassess in the future if circumstances changed markedly,” Clarida said Monday in an online event hosted by the Peterson Institute for International Economics.

Clarida also said policy makers might offer “refinements” to their Summary of Economic Projections -- a quarterly document that outlines their economic outlook and projections for rates -- in light of the framework changes announced last week by Fed Chair Jerome Powell.

“Now that we have ratified our new statement, the committee can assess possible refinements to our SEP with the aim of reaching a decision on any potential changes by the end of this year,” he said.

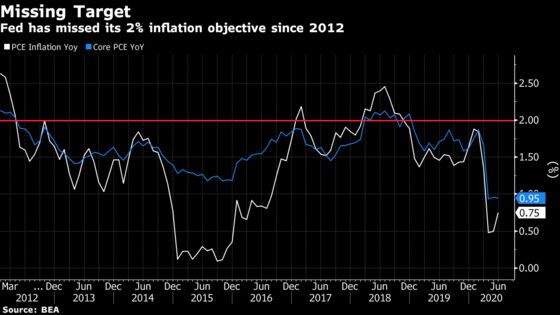

Clarida’s remarks follow Powell’s announcement that the U.S. central bank will sometimes allow inflation to run above its 2% objective to make up for prior undershoots, and allow unemployment to run lower than officials had previously tolerated. The shift is aimed at boosting inflation after years of falling short of the Fed’s target, an outcome that hurts the central bank’s ability to fight recessions.

Quarterly Forecasts

Fed policy makers next meet Sept. 15-16, when they’ll have a chance to spell out how the new long-term strategy will shape their near-term policies aimed at pulling the U.S. economy out of its sharpest downturn since the Great Depression.

Central bankers will also release their latest quarterly projections, which includes a dot-plot graphic describing individual officials’ expectations for future interest rates. In June, this signaled no increase in near-zero interest rates through 2022. The September forecasts will be pushed out to 2023.

While not entirely ruling out yield caps, also known as yield-curve control, Clarida repeated the Federal Open Market Committee’s conclusion that bond buying and communication on the future path of rates were the best tools to use once the federal funds rate had reached zero.

“We believe that forward guidance and large-scale asset purchases have been and continue to be effective sources of support to the economy when the federal funds rate is at” zero, he said.

In a question-and-answer segment that followed, Clarida said the committee would likely return in September to a discussion of how it may alter its guidance on future monetary policy, but stopped short of revealing his preferences or predicting any outcomes.

Guidance, Bond Buying

“Now that we have concluded the review, I imagine we’ll be returning to a discussion of potentially refining guidance and our balance-sheet communication,” he said. “But I really wouldn’t want to prejudge where we are going to end up on that.”

He did say, however, that threshold-based guidance -- indicating when changes in inflation or unemployment, or both, might justify a rate rise -- has been used before by the Fed and may be used again.

In his speech, Clarida offered more detail on the thinking behind the most important changes to the Fed’s statement of longer-run goals.

In the new statement, the Fed said its interest-rate decisions would be informed by its assessment of “shortfalls of employment from its maximum level.” The previous version had referred to “deviations from its maximum level.” The change de-emphasizes previous concerns that low unemployment can cause excess inflation.

Clarida essentially conceded this meant the Fed had given up anticipating future rises in inflation based solely on drops in employment.

Not a Sufficient Trigger

“This change conveys our judgment that a low unemployment rate by itself, in the absence of evidence that price inflation is running or is likely to run persistently above mandate-consistent levels or pressing financial stability concerns, will not, under our new framework, be a sufficient trigger for policy action,” he said.

Nonetheless, Clarida said that doesn’t mean the Fed is out of the business of forecasting.

“Because the effect of monetary policy on the economy operates with a lag, our strategy remains forward looking,” he said. “As a result, our policy actions depend on the economic outlook as well as the risks to the outlook.”

He also emphasized that switching to pursue 2% inflation on average does not introduce a mechanical formula for setting policy.

“To be clear, ‘inflation that averages 2% over time’ represents an ex-ante aspiration, not a description of a mechanical reaction function -- nor is it a commitment to conduct monetary policy tethered to any particular formula or rule,” he said.

©2020 Bloomberg L.P.