Fed Risks Stoking Financial Bubble in Drive to Lift Inflation

The Fed risks stoking similar asset bubbles that Powell has linked to the last two recessions with its eagerness to fan inflation.

(Bloomberg) --

The Federal Reserve risks stoking the same sort of asset bubbles that Chairman Jerome Powell has linked to the last two recessions with its new-found eagerness to fan inflation.

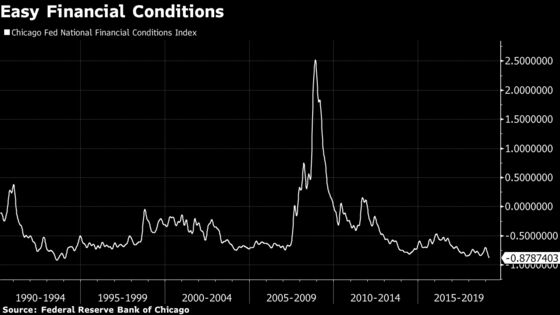

The Fed’s surprise pivot away from any interest rate increases this year has boosted prices of stocks, high yield bonds and other risky assets in spite of nagging investor concerns about slowing global economic growth. Financial conditions, at least as measured by the Chicago Fed, are at their easiest since 1994. And they could well get looser.

“If by late spring it feels like growth is picking up and the Fed is on hold, the markets are going to say Goldilocks is back and it’s risk on,’’ said former Fed official Nathan Sheets, who is now chief economist for PGIM Fixed Income.

That would put policy makers in a pickle. In unveiling the Fed’s U-turn last month, Powell highlighted the central bank’s determination to promote price pressures by declaring that low inflation was “one of the major challenges of our time.’’ And he left open the possibility that the Fed’s next rate move might be a cut after four increases last year.

But a drive to boost inflation through low interest rates could end up threatening financial stability by encouraging supercharged risk-taking, according to Allianz SE chief economic adviser Mohamed El-Erian.

And it’s just such “destabilizing excesses” that Powell has pinpointed as leading to the last two economic downturns. First it was the dot-com stock market boom of the late 1990s that crash landed and led to the 2001 recession. Then it was the housing boom and bust of the 2000s that preceded the biggest economic contraction since the Great Depression.

Easy Policy

The quandary for the Fed is that easy monetary policy seems more effective in spurring asset values than it does in boosting prices of goods and services.

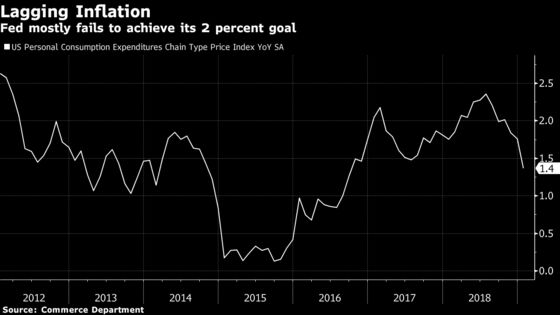

The S&P 500 Index rose by an average 8.5 percent from 2014 through 2018, while the personal consumption expenditures price index increased 1.3 percent, well below the Fed’s 2 inflation target. In January, the most recent month for which data is available, it stood at just 1.4 percent.

El-Erian, who is also a Bloomberg Opinion columnist, said that inflation is being held down by structural forces outside the Fed’s control. They include globalization, the diminished bargaining power of workers and the disinflationary impulses coming from such companies as online retailer Amazon.com Inc.

Powell has brushed off concerns that the central bank’s shift to an easier stance could spur a stock-market bubble such as occurred in the late 1990s dot-com boom.

“We’re in a very different world today,’’ he told reporters on March 20, arguing that the Fed is much more attuned to such risks than it was back then. “We don’t see financial stability vulnerabilities as high,’’ he added.

Powell also subscribes to the traditional Fed view that financial risks are best addressed via enhanced supervision and regulation rather than through changes in interest rates.

“Ultimately I am in a camp of thinking that monetary policy is not at all the ideal tool to address these questions,’’ he told the Economic Club of New York last November, though he did allow that there seemed to be a connection between low interest rates and credit growth and asset prices.

The problem for the Fed is that the U.S. has a limited set of supervisory and regulatory tools available to address financial stability risks, as Vice Chairman for Supervision Randal Quarles acknowledged in a speech last week.

The trade-off between financial stability and inflation might become more acute if the Fed changes its framework for achieving its price target when it completes a wide-ranging monetary strategy review next year.

Plan B

While Powell has ruled out increasing the 2 percent goal, he’s raised the possibility that the central bank could adopt a “make-up’’ strategy -- letting inflation run above target during good times like now, to offset the periods of slower price rises. The aim would be to convince consumers and companies that the Fed is committed to reaching its objective after years of mostly undershooting.

But to achieve that the Fed might have to keep interest rates lower for longer -- a strategy that would likely find favor in financial markets.

Former Fed Governor Jeremy Stein voiced doubts that inflation expectations are as important as some current policy makers believe.

“I don’t think the guy in the taco truck downstairs is going to set a higher price for tacos because the Fed says it’s aiming for 50 basis points higher inflation,’’ said Stein, who is now a Harvard University professor.

He also saw risks in the Fed adopting a strategy in which it explicitly aims for inflation above target for a while.

“Say we’re at 4 percent unemployment and inflation is stubbornly at 1.7 percent. That’s a pretty good place to be,’’ he said. “Do you want to say I’m going to commit now to keeping rates really, really low to fix this failure of 1.7 percent inflation, even in an environment when it might risk creating a bubble?’’

To contact the reporter on this story: Rich Miller in Washington at rmiller28@bloomberg.net

To contact the editors responsible for this story: Brendan Murray at brmurray@bloomberg.net, Alister Bull, Sarah McGregor

©2019 Bloomberg L.P.