A Fed Rate Cut Looks More Likely. The Question Is When and by How Much

Powell and his colleagues are expected to begin initial discussions on the rate cut decision tree at their upcoming meeting.

(Bloomberg) -- Federal Reserve Chairman Jerome Powell and his colleagues face three decisions when it comes to reducing interest rates: whether to do it, when to do it, and by how much.

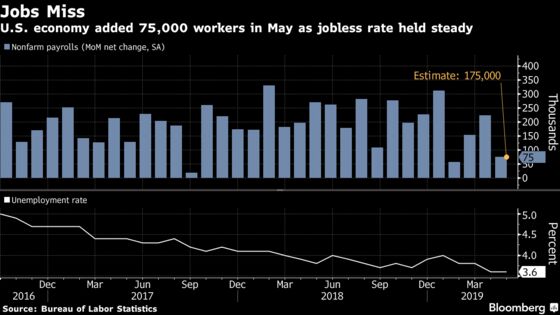

Fed watchers say an unexpectedly weak reading on the U.S. jobs market in May makes it increasingly likely that the central bank will lower rates this year -- in spite of President Donald Trump’s decision late Friday to call off his threatened tariffs on Mexico.

What’s less certain is when the Fed will act and how big any cut will be -- a more traditional 25 basis point move or a bolder, 50 basis point reduction designed to get a bigger bang for the buck.

“We obviously feel more confident that they’re going to be easing,’’ JPMorgan Chase & Co. chief U.S. economist Michael Feroli said after news on Friday that payrolls growth slowed abruptly in May. He expects the central bank to lower rates by a quarter percentage point in September and December, even with the U.S. immigration deal with Mexico that forestalled the threat of U.S. import tariffs on Mexican goods.

Trump criticized the Fed during a CNBC interview Monday, renewing his complaint over rate increases last year and calling it “very, very destructive.”

The feeble jobs numbers came on the heels of soft data on retail sales, factory output and home purchases and occur against a background of Trump’s escalating trade war with China.

Powell and his colleagues are expected to begin initial discussions on the rate cut decision tree at their upcoming meeting, though they’re seen as unlikely to reach a conclusion at the June 18-19 gathering.

Instead, economists say, policy makers will probably revamp their post-meeting statement to indicate their openness to easing policy, perhaps as soon as the July 30-31 gathering.

Patient No Longer

Gone will be the promise of policy patience that’s characterized Federal Open Market Committee statements since January.

In its place is likely to be something more along the lines of what Powell said last week -- namely, that the Fed is “closely monitoring’’ the economy and is ready to “act as appropriate to sustain the expansion.’’

U.S. stocks were on track to advance for a fifth straight session on Monday as investors responded to Trump lifting the threat of Mexican tariffs. Bets on Fed rate cuts were dialed back a bit but remain firmly on the side of a cut in July.

Sooner Than Later

Fed watchers say the latest economic data boost the odds that central bank will move sooner rather than later to lower rates.

Julia Coronado, founder of MacroPolicy Perspectives LLC in New York, said she now expects quarter-point cuts in July and September, sooner than the September-December reductions she previously anticipated.

“If this came in a tranquil environment I don’t think they’d be contemplating rate cuts on the back of’’ the weak jobs report, she said. “But we’re not in a tranquil environment” even though Trump dropped his threatened tariffs on imports from Mexico.

Other trade threats, including unresolved tensions with China and the potential for the U.S. to impose tariffs on auto imports from Japan and the European Union, still loom.

Barclays Plc economists Michael Gapen and Jonathan Millar also moved up their call for rate cuts to July and September. But they expect the first move to be a half percentage point, and the second cut a quarter point.

“The reason they’d come in with 50 basis points is that the emphasis would be on surprising the markets,’’ senior U.S. economist Millar said. “With limited ammunition they want to come in big and make those bullets count.’’

The central bank’s current target range for the fed funds rate is 2.25% to 2.5%. That’s about the half the roughly 500 basis points it has lowered rates by in the past when the economy entered a recession.

Arguing against a big reduction: It could spook investors into thinking that the Fed was panicking, and that the economy is in a lot worse shape than it actually is.

Jan Hatzius, chief economist at Goldman Sachs Group Inc, argued the Fed would in fact leave rates on hold this year. In a note Monday titled “No Time to Panic,” he wrote that this was a close call but data outside of the May payroll report still look decent.

Muted Inflation

The Fed can afford to be aggressive because inflationary pressures are muted. Indeed, Fed Vice Chairman Richard Clarida suggested in May that the low level of inflation might be a reason to ease policy.

“If the incoming data were to show a persistent shortfall in inflation below our 2% objective or were it to indicate that global economic and financial developments present a material downside risk to our baseline outlook,’’ the FOMC would take that into account in setting policy, he told the Economic Club of New York on May 30.

To be sure, the Fed could face criticism that it’s caving to political pressure and indirectly aiding Trump’s 2020 re-election bid if it cuts rates sharply. But that’s a risk it seems willing to take.

“Our priority today is to put in place policies that will help sustain maximum employment and price stability,’’ Clarida said.

--With assistance from Christopher Condon and Reade Pickert.

To contact the reporters on this story: Rich Miller in Washington at rmiller28@bloomberg.net;Steve Matthews in Atlanta at smatthews@bloomberg.net

To contact the editors responsible for this story: Margaret Collins at mcollins45@bloomberg.net, Alister Bull, Ros Krasny

©2019 Bloomberg L.P.