Fed Puts Inflation Expectations at Heart of Major Policy Review

Fed Puts Inflation Expectations at Heart of Major Policy Review

(Bloomberg) -- For four decades the specter of high inflation haunted the Federal Reserve. Now it has an equally ominous flip side.

“We need to make sure inflation doesn’t keep slipping down toward zero, because then the central bank really does have less and less ability to react to downturns,’’ Fed Chairman Jerome Powell said during a Q&A at Stanford University on March 8.

Fed officials have long called their 2 percent inflation target “symmetric,” but now they want you to know they really mean it. They’re so concerned that policy makers are contemplating creative, and politically risky, strategies for raising long-run inflation rates.

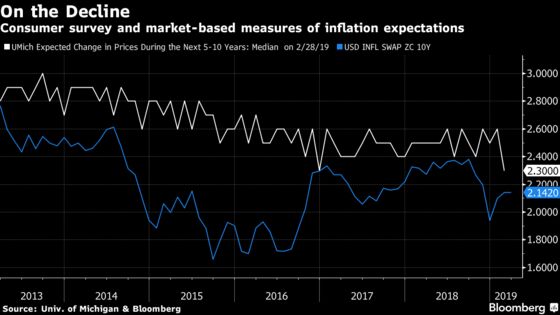

It’s worth noting, however, that those strategies rely heavily on the curious concept of inflation expectations and the power economists assign to it as a determinant of future prices. The Fed’s leadership are true believers, but economists don’t fully understand how the phenomenon works. And among people who make real-world price-setting decisions, it’s sometimes viewed as downright silly.

“Inflation hasn’t fluctuated a lot in the last 15 years, but whether that’s really because of anchored expectations is a big question mark,” Jeffrey Fuhrer, an economist and senior policy adviser at the Boston Fed, said in an interview last month.

’Most Important Driver’

Put simply, many economists believe inflation outcomes are heavily influenced by what ordinary people expect inflation will be. Testifying before Congress on Feb. 26, Powell called inflation expectations “the most important driver of actual inflation.”

In theory, this works through two channels: consumption and price setting. If millions of people expect inflation this year will rise substantially, eating away at the purchasing power of their incomes, consumers and businesses will bring forward spending and investment decisions. At the same time, workers will ask for higher wages and firms will raise prices. The higher demand, plus higher wages and prices, will help generate the inflation that’s anticipated.

The concept explains why central bankers have made supreme efforts since the 1970s and ‘80s to establish their credibility in controlling inflation. Once the public trusts in that commitment, expectations for inflation won’t respond significantly to shocks, like a big jump in energy prices or a sharp drop in unemployment, thereby helping to anchor actual inflation at a low level.

Inflation in the U.S. appears to validate the theory. Since 1993, the Fed’s favorite measure of core prices has averaged just 1.8 percent.

“Certainly after the persistent decline in inflation, after the early 1980s, expectations came down and have stayed down since,” said Olivier Coibion, a professor of economics at The University of Texas at Austin.

The Fed has arguably been too successful. Fed Vice Chairman Richard Clarida said recently he considered expectations to be “at the lower end of a range that I consider to be consistent with our price-stability goal of 2 percent.’’ Before and since Clarida said that, measures of inflation expectations have been moving down.

That’s pushed the Fed to think about adopting a potential “make-up” strategy that would push inflation above target after periods of under-shooting, with the aim of raising expectations back up a bit. But faith in inflation expectations is not universal. Economists have had trouble demonstrating exactly how it works at the micro level.

For starters, for expectations to work the public should really know something about inflation. Research, however, shows that in countries like the U.S., where inflation has long been low and stable, people pay little attention. Most have almost no clue where inflation lies or where inflation may be going. According to Goldman Sachs, only 20 percent of Americans even know the Fed has a 2 percent inflation target.

Where knowledge is high, some research shows household consumption does respond to changes in inflation expectations. But in other experiments wage demands and price-setting decisions showed almost no reaction to changes in expectations.

‘No. Never’

Henry Copeland runs Pressflex, a small firm in Durham, North Carolina, providing web-based software services. Copeland said competition and technology mean prices are constantly falling. Asked if he thinks about where overall inflation is likely to be in the coming year when he sets prices, he laughed out loud. “No. Never,’’ he said.

Copeland’s view echoes wider surveys showing most business owners look to a narrow set of factors related to their company and their sector when setting prices, and not to aggregate inflation.

“It’s almost like we have two different models of the world and how it works,” said Edward Knotek, an economist at the Cleveland Fed.

Still, Knotek is sticking with expectations. “If you drill really deep to the individual level, you’re probably not going to think in terms of broad aggregates,” he said. “But there are broader forces that are moving supply and demand, and that’s part of what we’re capturing in inflation expectations.”

If the Fed ends up taking a crack at its make-up strategy, it’ll be hoping that’s true.

To contact the reporter on this story: Christopher Condon in Washington at ccondon4@bloomberg.net

To contact the editors responsible for this story: Brendan Murray at brmurray@bloomberg.net, Alister Bull

©2019 Bloomberg L.P.